Thursday April 26: Five things the markets are talking about

Global equities traded mixed overnight, as the market digested the latest flood of company earnings ahead of the ECB monetary policy announcement (07:45 am EDT).

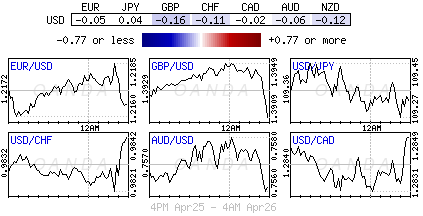

The ‘big’ dollar is steady, trading atop of its three-month highs. US Treasury prices have found a small foothold, while oil prices gained on the possibility that President Donald Trump will withdraw from the Iran nuclear deal, casting a cloud over Middle East geopolitics.

At today’s ECB meeting, investors will be watching for any clues that Euro policy makers are preparing a shift in stimulus plans for their June meeting. Stateside, earnings season continues.

On Friday, the Bank of Japan (BoJ) announces its latest policy decision and releases updated economic projections, while in the US the market will be focusing on Q1 GDP data.

Elsewhere, in Asia, the leaders of North and South Korea meet on Friday.

1. Stocks mixed results

In Japan, the Nikkei share average rallied overnight, supported by tech shares, with index heavyweight Tokyo Electron jumping after it forecast strong profits for this fiscal year. The Nikkei ended +0.5%, while the broader TOPIX added +0.3%.

Down-under, Aussie shares ended slightly lower, as a decline in financial stocks, weighed by a fall in AUD (A$0.7567) and mortgage concerns, offset gains in healthcare. The S&P/ASX 200 index fell -0.2%. In South Korea, the KOSPI climbed +1.3%, with tech shares buoyed by news of a record quarterly profit from Samsung (OTC:SSNLF).

In China and Hong Kong stocks plummeted overnight, as tech shares came under pressure amid the US Huawei probe. The CSI 300 fell -1.9%, while the Shanghai Composite Index slipped -1.4%. In Hong Kong, the Hang Seng index dropped -0.7%, while the Hong Kong China Enterprises Index lost -0.6%.

In Europe, regional bourses trade mostly higher. The DAX trades little changed, with Deutsche Bank (DE:DBKGn) recovering from earlier losses after missing estimates. The market awaits a slew of corporate earnings.

US stocks are set to open in the ‘red’ (-0.1%).

Indices: STOXX 600 +0.2% at 380.8, FTSE 100 flat at 7378, DAX -0.1% at 12406, CAC 40 +0.3% at 5428, IBEX 35 +0.3% at 9891, FTSE MIB +0.3% at 23884, SMI +0.4% at 8776, S&P 500 Futures -0.1%

2. Oil prices rise on Iran sanctions worries, gold prices unchanged

Oil prices are rallying ahead of the US open, supported by expectations that the US will re-impose sanctions against Iran, a decline in output in Venezuela and ongoing strong global demand.

Brent crude oil futures are at +$74.27 per barrel, up +27c, or +0.4%, from Wednesday’s close. US West Texas Intermediate (WTI) crude futures are up +14c, or +0.2%, at +$68.19 per barrel.

Dealers expect that the US will in May re-impose sanctions against Iran, who is a major oil producer and member of the OPEC.

Also aiding prices is French President Emmanuel Macron stating that he expected the US President Donald Trump to pull out of a deal with Iran reached in 2015, in which Iran suspended its nuclear program in return for the west to lift their crippling sanctions.

Note: Trump is expected to decide by May 12 whether to restore US sanctions on Iran.

Also supporting prices is global demand and the declining output in Venezuela, OPEC’s biggest producer in S. America.

Gold prices stuck to a narrow range overnight, trading atop yesterday’s five-week low print, pressured by a stronger US dollar and a rise in Treasury yields. Spot gold is up +0.1% at +$1,324.61 per ounce, a day after it fell to +$1,318.51, its lowest since March 21. US gold futures have rallied +0.3% to +$1,326.2 an ounce.

3. Riksbank and ECB monetary policy decisions

Swedish government bond yields are stable after the Riksbank left its repo rate unchanged earlier this morning at -0.50%, in line with market expectations.

The 2-year bond yield trades at -0.49%, while the 10-year bond yield trades at +0.77%, same as before the rate decision.

In their statement, the Riksbank indicated that a rate increase is not expected until toward the end of the year, while government bond redemptions and coupon payments will be reinvested in the bond portfolio until further notice.

At today’s ECB press conference announcement (08:30 am EDT), President Draghi is expected to keep a positive tone despite the recent setback of some economic indicators. The combination of growth and inflation comments might signal rising awareness in favour of policy “normalization”. The consensus sees the probability of a ‘dovish’ surprise as “rather low,” while a “neutral” meeting should not obstruct a continued rise in bond yields.

The yield on US 10s decreased -2 bps to +3.01%, the first retreat in more than a week and the biggest tumble in more than two weeks. In Germany, the 10-year Bund yield declined -2 bps to +0.62%, the largest decrease in more than a week, while in the UK, the 10-year Gilt yield decreased -1 bps to +1.525%.

4. Market focus on ECB and EUR

The market consensus believe that unless ECB President Draghi puts a lot of emphasis on downside risks to the eurozone economic outlook this morning, justifying “a further dovish re-pricing of ECB policy expectations,” the EUR (€1.2170) has a chance to benefit. Despite the recent slowdown in EU growth and inflation it’s going to be rather difficult to see a dovish Draghi in his press conference. The EUR/USD at the moment is finding it difficult to hold onto gains in the overnight session.

EUR/SEK (€10.4614) has moved higher after the Riksbank pushed slightly back its first potential rate hike from the beginning of H2 until the latter part of 2018.

5. German consumer sentiment set to weaken

Data this morning from the German market research group GfK showed that geopolitical issues and growing protectionism are souring German consumers’ mood.

GfK’s forward-looking consumer confidence index is set to drop to 10.8 points in May from 10.9 points in April, it said. The decrease is in line with a market forecast.

“The escalation of the Syrian crisis and the protectionist trade policies of the US are worrying consumers and could now also affect Germany’s previously excellent economic prospects,” GfK said.

Digging deeper, GfK noted that consumers’ economic optimism suffered a setback in April, falling to 37.4 points from 45.9 points in March, hit by geopolitical concerns and US. protectionist trade policies, negative exacerbated by major fluctuations on stock markets.

Income expectations “cannot escape the downward trend in economic outlook in April,” GfK said, as the sub-index fell to 53.5 points in April from 54.9 points in March.