Thursday March 22: Five things the markets are talking about

Ahead of the US open, Treasuries prices have rallied, the once ‘mighty’ dollar has extended its losses and Euro equities are under pressure as the market assesses the implications of higher borrowing costs in the US and in China, alongside global trade tensions.

Note: The White House administration is set to announce trade tariffs against China later today (12:30 EDT).

Overnight, the People’s Bank of China (PBoC) increased short-term interest rate just hours after the Fed announced its first interest-rate increase for this year. The PBoC raised the rate by +0.05% for the seven-day tenor.

Yesterday, Fed officials, meeting for the first time under new Chairman Jerome Powell, as expected raised the benchmark lending rate +25 bps and forecast a steeper path of hikes in 2019 and 2020, citing an improving economic outlook.

Nevertheless, the market was disappointed as they had expected US officials to live up to some predictions that it would lean towards four rate hikes this year, instead of the three that had been communicated yesterday (dots suggest 2 more hikes this year for total of 3).

1. Stocks mixed results

In Japan, the Nikkei share average rallied overnight despite a stronger yen (¥105.68) with retail investors purchasing recently battered stocks. The Nikkei ended +1.0% higher, while the broader Topix was up +0.7%.

Down-under, Aussie shares fell on Thursday, as early gains from solid jobs data were erased by losses amongst financials. The S&P/ASX 200 index slipped -0.2%. The benchmark had advanced +0.2% on Wednesday. In S. Korea, the KOSPI stock index surged to a seven-week high on a less ‘hawkish’ than anticipated Fed. At the close it was up +0.44%.

In Hong Kong, tech firms drag down regional shares as trade war fears weigh. At close of trade, the Hang Seng index was down -1.1%, while the Hang Seng China Enterprise index fell -0.8%.

In China, stocks were also under pressure on concerns over a potential trade war between the world’s two largest economies. At the close, the Shanghai Composite index was down -0.5%, while the blue-chip Shanghai Shenzhen CSI 300 index was down -1%.

In Europe, regional indices trade lower across the board, tracking US futures lower following the FOMC rate decision yesterday and the BoE rate decision this morning.

US stocks are set to open deep in the ‘red’ (-0.8%).

Indices: STOXX 600 -0.7% at 372.1, FTSE -0.6% at 6993, DAX -1.1% at 12170, CAC 40 -1.0% at 5189, IBEX 35 -0.8% at 9556, FTSE MIB -1.0% at 22600, SMI -0.8% at 8713, S&P 500 Futures -0.8%

2. Oil under pressure as US output to disrupt markets, gold higher

Oil prices are under pressure as the rise in US crude production threatens to undermine efforts led by OPEC to tighten the market.

Brent Crude futures are at +$69.34 per barrel, down -13c, or -0.2% from their last close. US West Texas Intermediate (WTI) crude futures are at +$65.13 a barrel, down -4c from their previous settlement.

Note: Both benchmarks yesterday hit their highest levels since early February, having risen around +10% from its March lows.

Any confidence in the oil market is being tempered by US crude production – last week it climbed to a new record of +10.4m bpd, putting the US ahead of top exporter Saudi Arabia and within reach of Russia’s +11m bpd.

Note: Yesterday’s EIA report showed that US crude inventories had a drawdown of -2.6m barrels in the week ended March 16 to +428.31m barrels.

Ahead of the US open, gold prices trade atop of its two-week high on a weaker dollar after the Feds rate view. Spot gold has rallied +0.1% to +$1,332.77 per ounce. Prices rose to a two-week high of +$1,336.59 yesterday, and also registered their biggest single-day percentage gain since May of last year.

3. Yields fall on ‘dovish’ Fed

This morning, the Bank of England (BoE) is expected to keep interest rates and its asset-purchase program unchanged at 08:00 EDT. Attention will be on the language and the odds for a May hike, now seen as increasingly likely despite softer-than-expected inflation. UK inflation fell to +2.7% in February, but remains well above the BoE’s +2.0% target.

Down-under, the NZD/USD (N$0.7233) jumped by +1.1% after the FOMC statement, but had little reaction to its own central bank’s comments yesterday afternoon. The RBNZ left its official cash rate unchanged at +1.75%, as widely expected.

Note: New RBNZ Governor, Adrian Orr, starts work next Tuesday.

Elsewhere, the yield on US 10-Year’s has decreased -3 bps to +2.85%, the biggest dip in three weeks. In Germany, the 10-year Bund yield has fallen -2 bps to +0.57%, the lowest in almost two-months.

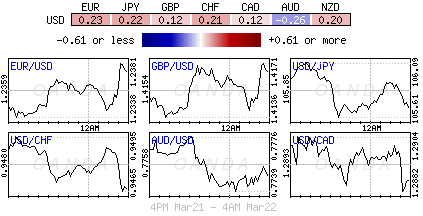

4. Dollar under intense pressure

The once ‘mighty’ USD continues with its softer tone after yesterday’s Fed decision. The Fed had executed a ‘hawkish’ hike, but fixed income dealers have given it a dovish spin as they expected four hikes in 2018, not the dot planned three.

The markets focus now shifts to sterling (£1.4140). GBP rallied to a seven-week high outright of £1.4181, helped by a broad-based weakening of the dollar as well as above-forecast U.K. retail sales data (see below). Market will be looking closely at the BoE’s statement – a “hawkish” tone [which means a 8-1 or 7-2 vote] may tilt the balance in favour of a rate hike as early as May.

Elsewhere, the EUR/USD (€1.2326) remains contained within its 2018 trading range, but a tad firmer in today’s session.

5. UK retail sales rebounded in February

Data from the ONS this morning showed that UK retail sales rebounded last month, but the underlying picture stayed weak, signalling that the British consumer remains cautious.

Sales grew by +0.8% on month in February, compared with a monthly decline of +0.2% in January. The headline print was double the markets expectations.

Digging deeper, with the exception of non-food stores, all retail sectors saw growth in the month. This, however, came after a -0.3% downward revision to January’s monthly growth.