Wednesday January 25: Five things the markets are talking about

The new U.S. President is certainly providing opportunity for speculators in these choppy markets. All asset classes continue to witness strong intraday volatility, which is not expected to ease up anytime soon.

In particular, currency moves have been leading the pack this week. This year's geopolitical concerns (Brexit, Trumponomics, Dutch, French and German federal and regional elections), supported mostly by the rise of populism, are expected to dominate capital markets’ asset price moves.

Overnight, global flows to haven assets continued to reverse, with gold again under pressure, sovereign bond yields backing up to their highs of the year, while global indices catch a bid on President Trump’s plans to boost infrastructure projects. Yesterday, POTUS revived two oil pipeline projects and issued directives that aim to ease regulations on infrastructure projects and U.S. manufacturing.

Today, the President is expected to focus on immigration and “Wall” building.

1. Equities – green lights across the board

Global equities are carrying on the stellar work of the Dow's Tuesday move higher.

In Asia, equities were supported by investors improved risk sentiment from both regional economic data and overnight gains in the U.S.

Despite the dollar reversing some of its gains against the yen (¥113.66), the Nikkei closed out their session rising +1.4% after setting a two-month closing low in the previous session. Data overnight saw Japan’s exports rise y/y in December for the first time in 15-months.

However, gains elsewhere were notably more muted. Australia’s S&P/ASX 200 rallied +0.4% on mining support. Hong Kong’s Hang Seng index was up +0.3%, while Korea’s Kospi added +0.1% as that country’s economy grew faster than expected in Q4.

In China, stocks shed their early weakness after the PBoC hiked the rate on its medium-term lending facility by +10 bps (a tightening bias). The Shanghai Composite closed out up +0.2%.

In Europe too, equity indices are trading sharply higher, with bank’s leading the gains across the board on a back up of sovereign yields. Commodity and mining stocks are generally lower, but mixed in the FTSE 100.

U.S. futures are set to open in the black (+0.2%).

Indices: Stoxx50 +1.1% at 3,316, FTSE +0.2% at 7,163, DAX +1.1% at 11,726, CAC 40 +1.0% at 4,877, IBEX 35 +1.6% at 9,534, FTSE MIB +0.2% at 19,546, SMI +1.1% at 8,335, S&P 500 Futures +0.2%

2. Oil slips on rising U.S inventories, gold looking for support

Oil prices remain under pressure ahead of the open after builds in U.S. inventories yesterday reinforced expectations that increasing shale output this year would reduce the impact of production cuts by OPEC and other major exporters.

Brent futures are trading down -40c a barrel at +$55.04, while U.S. light crude (WTI) is also down -40c at +$52.78.

Yesterday’s weekly American Petroleum Institute (API) data showed U.S. crude, gasoline and diesel stocks all rose more than expected last week. Expect the market to takes its cue from this morning’s Energy Information Administration (EIA) at 10:30 EST.

Ahead of the open stateside, gold prices have slid -0.5% to +$1,204.07 an ounce after sliding -0.8% yesterday. The metal reached its highest level since November on Tuesday, when the bullion touched +$1,219.59.

3. Sovereign yields trade atop of year highs

In Europe, government bonds have been aggressively sold this morning, after a top ECB official signalled yesterday that policy makers there should soon start to wind down their +€2.3T bond-purchase program.

The yield on 10-year German bunds has backed +5bps to +0.375%. Their counterpart in the U.S., 10-Year Treasuries yields, have also crept higher after their biggest one-day leap in over a month yesterday, to around +2.483%, up from +2.471% at Tuesday’s close.

Elsewhere, the rate on 10-Year Aussie bonds has climbed +4bps to +2.73% after dropping for two consecutive sessions. In China, government bond yields are nearing their highest levels, since 2015 after the PBoC unexpectedly raised interest rates on a type of special loans to certain financial institutions.

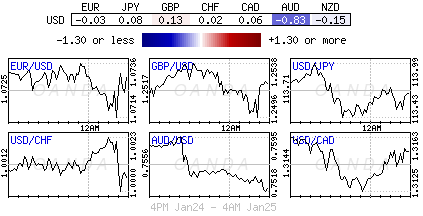

4. Dollar looking for a directional aid

Ahead of the U.S session, the FX market is trading in a relatively tight range. It seems that dealers and investors seem somewhat reluctant to push the ‘mighty’ dollar any higher just yet – the market fears the rhetoric to stem a “stronger dollar” from Trump and administration officials.

Currently, GBP/USD trades atop of its six-week high just shy of the psychological £1.2600 handle one day after the U.K’s Supreme Court instructed PM Theresa May that she cannot go it alone to begin the country’s withdrawal from the EU – she needs to now win the approval of parliament. Europe’s single unit is hovering around the €1.0750 area, while USD/JPY trades just above ¥113.50.

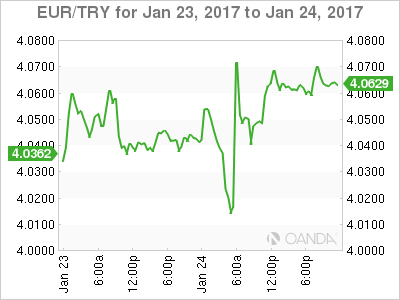

Elsewhere, TRY is maintaining its soft tone (-1% outright to $3.8245) following the Turkish central bank (CBRT) decision this morning to open a +$300m forex swap auction at a +10% interest rate. Expect the market to watch ongoing lira liquidity operations.

5. German Business confidence disappoints

Data this morning showed that the German Ifo headline business sentiment index fell this month to 109.8 – the market was expecting a 111.3 print.

Note: with Germany heading into a potentially turbulent year ahead of federal election in Q3, expect ongoing uncertainty to continue to dampen economic prospects.

This morning print has failed to have any impact on the EUR, given that the recent domestic data points to a solid performance by the German economy.