Monday December 19: Five-things the markets are talking about

The dollar and sovereign yields fell overnight while Asian shares printed a new monthly low as the market cashed in some of their recent bets on Trumponomics and the ‘reflation’ trade.

This will be a light week on many fronts – liquidity and fundamentally.

The Bank of Japan (BoJ) meets this evening to complete the latest round of global central bank meetings. With growth improving and yen weakening, expectations are for no change in Japan’s domestic monetary policy. Governor Kuroda may give a clue to policy going forward in his post comments.

Note: The BoJ is expected to make no change to its twin targets of -0.10% on excess reserves and the zero percent 10-year government bond yield.

Elsewhere this week, final estimates of Q3 GDP will be reported for France and the U.K. In the U.S it’s a light week for key indicators starting Wednesday with existing home sales. Personal income and spending data on Thursday are expected to show moderate gains, while durable goods orders, are expected to fall sharply, however, ex-aircraft, are expected to hold steady. Thursday’s U.S jobless claims are not expected to stray too far from expectations while Friday’s new home sales will complete the final week before the holiday season.

1. Global stocks lower on China worries

Asia equities were lower overnight as China’s markets continued to be rattled by a bond selloff and by fresh signs of a slowdown in the domestic property market.

Japan’s Nikkei Stock Average slipped -0.1%, Hong Kong’s Hang Seng Index closed down -0.9% and Korea’s Kospi was off -0.2%. The Aussie ASX 200 was the outlier, closing up +0.5% even as a threat of a downgrade to the country’s AAA rating hung over markets.

Chinese stocks edged down amid fears that capital was fleeing the country amid a selloff in sovereign debt (China’s 10-Year bond prices were down -1.1%). The Shanghai Composite closed down -0.2%.

Also putting pressure on global bourses were plummeting Chinese metal prices. Why? Authorities are trying to curb potential asset bubble and this has local speculators liquidating.

In Europe, the Stoxx 600 edged lower after reaching the highest point of the year on Friday, while the FTSE 100 is little changed in quiet trading.

U.S futures have rallied +0.2%, taking back all of Friday’s losses.

Indices: Stoxx50 -0.3% at 3,242, FTSE flat at 6,998, DAX flat at 11,366, CAC 40 -0.2% at 4,809, IBEX 35 -0.4% at 9,307, FTSE MIB +0.6% at 19,112, SMI -0.1% at 8,203, S&P 500 Futures +0.2%

2. Crude and commodities get a boost from an underwhelmed dollar

Crude Oil prices are higher overnight as a weaker dollar and the news of a delay of new Libyan oil exports support benchmarks, amidst expectations of tighter crude supply next year.

Brent crude futures traded at +$55.47 per barrel, up +26c, while U.S. light crude (WTI) were up +30c at +$52.20 a barrel.

The future direction of oil prices depends on OPEC’s and non-member compliance to last month’s agreement to a cut in global production. Producers are expected to adhere to a cut of almost +1.8m bpd in oil output from January 1.

However, the higher the price of crude goes, it attracts older drilling rigs to come back on line. Data indicates that drilling for new oil has increased for seven straight weeks.

In the U.S, 12 oil rigs were added last week, bringing the total count to 510, the highest in 12-months.

Elsewhere, gold prices have edged higher, rising above the lowest level touched in 10-1/2 months last week (+$1,122.35), as the ‘mighty’ dollar takes a breather against a basket of currencies. Spot prices are trading atop of +$1.137.85 ahead of the U.S open.

3. Sovereign Yields remain elevated, but quiet

Despite the telegraphed token rate hike by the Fed last week, U.S. 10-Year notes trade at +2.58%, down -1bps overnight, but still close to its 24-month high print of +2.64% last week.

Note: The sovereign benchmark is up +100bps or +1% from the U.S election (Nov 8)

In China, the 10-year sovereign yield rallied another +5bps to +3.40% in the overnight session. That’s a total of +25bps in five business days. Hawkish comments from the Fed last week and waning liquidity in China continue to weigh on prices.

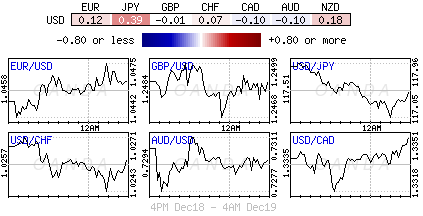

4. Dollar bruised, but not battered

The might ‘buck’ begins the week on the back foot as heightened geopolitical tensions over China’s seizure of a U.S. naval drone has convinced a number of investors to offload some of the dollars Trumponomic premium.

Given the week that’s in it, don’t be surprised to see a further retracement ahead of the New Year.

Overnight, the yen (¥117.41) is one biggest gainers, dropping well below last week’s peak of around ¥118.66. The USD/JPY is certainly one of those currencies that could be most vulnerable since it was the biggest looser (or winner if you are a Japanese exporter, depreciating -10%) since the U.S election.

Elsewhere, Europe’s single unit has also gained, with the EUR/USD up +0.1% at €1.0463. Sterling is little changed, trading relatively flat at £1.2440 ahead of the U.S open.

5. Germany’s Ifo confidence beat’s expectations

This morning, German business sentiment hit its highest level in nearly two-years, beating forecasts, as the Ifo index rallied to a reading of 111.0 in December, up from 110.4 m/m.

However, despite the upbeat print, analysts expect the current positive German growth cycle, which is also coming to an end, will put future headline prints under pressure.

Many are pointing to a number of unknown variables, the impact from U.S. President-elect Trump on trade and economic policies, future Brexit negotiations, and renewed political tensions in Europe to all have a negative impact one way or another.