Most EU and US indices rebounded yesterday. However, we are reluctant to say that the latest retreat is over, as concerns over a second round of lockdown measures around the globe are still on the table. Overnight, the Kiwi rose after the RBNZ held its policy untouched. Perhaps its traders were looking for a more dovish outcome. As for today, the main items on the agenda are the preliminary PMIs for September.

USD KEEPS SHINING, BUT EQUITIES REBOUND SOMEWHAT

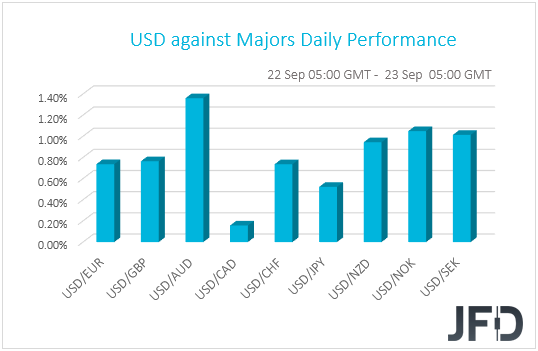

The US dollar continued to trade higher against all the other G10 currencies on Tuesday and during the Asian morning Wednesday. It gained the most versus AUD, NOK, SEK, and NZD in that order, while it recorded the least gains against CAD.

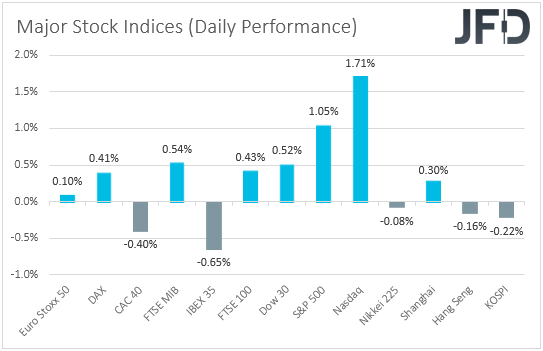

The strengthening of the US dollar suggests that financial markets continued trading in a risk-off manner. However, looking at the equity world, we see that this was not the case. The majority of EU indices closed in positive territory, with risk appetite getting boosted later, during the US session. That said, sentiment softened again during the Asian morning today. After a two-day holiday, Japan’s Nikkei 225 slid -0.08%, and although China’s Shanghai Composite is up 0.30%, Hong Kong’s Hang Seng and South Korea’s KOSPI are both down 0.16% and 0.22% respectively.

EU indices were helped by a jump in oil and tobacco shares, with American Tobacco and Imperial Brands (OTC:IMBBY) gaining more than 3% after RBC upgraded their ratings to “outperform”. Wall Street was boosted by Amazon.com Inc (NASDAQ:AMZN)., which jumped 5.7% after Bernstein upgraded the stock to “outperform”, saying that the firm will continue to be supported even after the pandemic is contained.

As for our view though, we are reluctant to say that the latest correction is over, and that the prevailing uptrends have resumed. Concerns over a second round of lockdown measures around the globe are still there, and this is evident by the fact that the safe-haven US dollar stayed on the front foot. The easing appetite during the Asian session today supports the notion as well, suggesting that yesterday’s rebound may have been just a dead cat bounce before the next leg south. We repeat that the fresh fears of another round of restrictions, which could hamper the economic recovery, suggest that there is still ample room for further declines. There are also several other issues that could keep investors’ anxiety elevated, the likes of US-China tensions, Brexit, the upcoming US elections, and the stalemate in the US Congress with regards to passing a fresh coronavirus-aid bill.

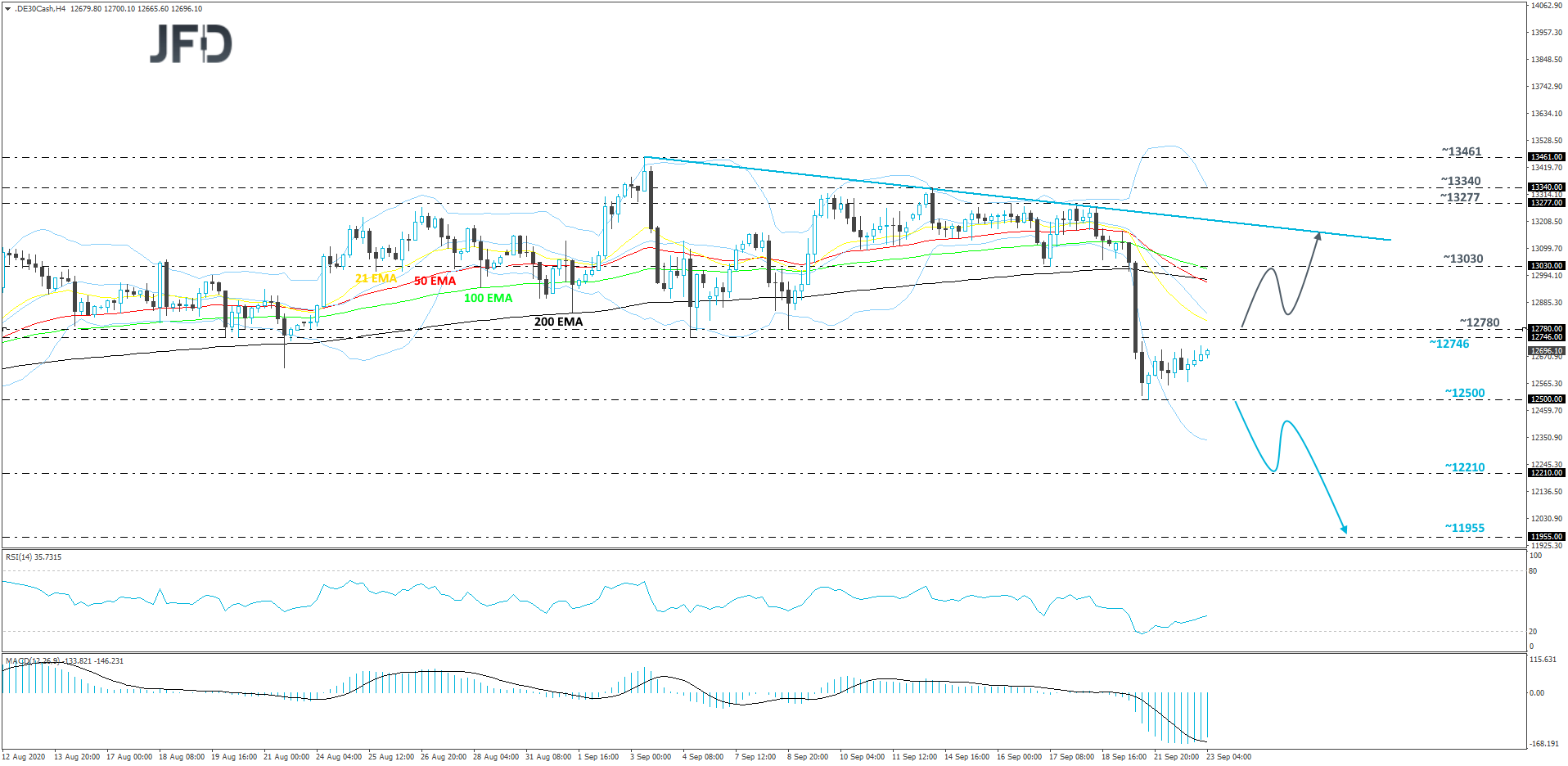

DAX – TECHNICAL OUTLOOK

We saw DAX moving heavily to the downside on Monday and then finding support at the 12500 hurdle, which continues to hold the price from moving lower. That said, the current rebound could be seen as a temporary correction before another possible leg of selling, especially if the index remains below the 12746 area, marked by the low of September 4th. For now, we will take a cautiously bearish approach.

In order to get comfortable with further declines, a break of the aforementioned 12500 hurdle would be needed. Such a move would confirm a forthcoming lower low, potentially sending the German index further south. That’s when the price might hit the 12210 hurdle, marked by the low of July 31st, which may halt the slide for a bit. However, if the bulls are still nowhere in sight, the fall could continue below that hurdle, where the next potential support level might be at 11955, which marks the lows of June 25th and 29th.

On the other hand, if the price is able to climb back above the 12780 barrier, marked by the low of September 8th, that may open the door for a larger correction higher. The German index might travel to the low of September 17th, at 13030, which could stall the uprise temporarily. DAX might retrace back down somewhat, however if the price stays above the 12780 zone, the buyers may take charge again and this time lift the index above the 13030 area. If so, the move higher could continue, but the price might find resistance near the short-term downside line, drawn from the high of September 3rd.

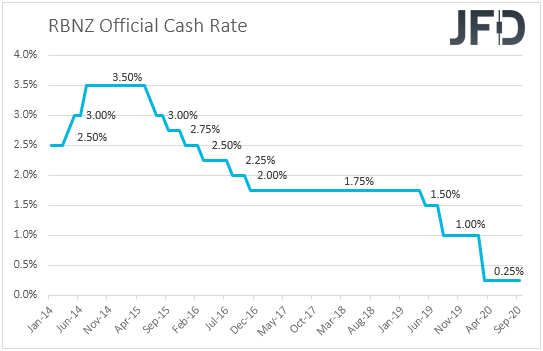

RBNZ STANDS PAT, PREL. PMIS TAKE CENTER STAGE

Back to the currencies, the Kiwi gained nearly 50 pips against its US counterpart overnight, following the RBNZ decision, though the currency was still found lower this morning. The RBNZ kept its Official Cash Rate (OCR) and its Large-Scale Asset Purchase (LSAP) unchanged, repeating that further monetary stimulus may be needed in the foreseeable future, including a Funding for Lending Program, a negative OCR, and purchases of foreign assets.

The rally in the Kiwi suggests that many participants may have been waiting for a more dovish language, perhaps clearer signals as to when fresh stimulus measures may be deployed. In any case, for now, we expect the risk-linked currency to be mainly driven by developments surrounding the broader investor morale. In case concerns over a second round of covid-related restrictions trigger another selloff in equities, the Kiwi is likely to suffer as well, especially against the safe-havens US dollar and Japanese yen.

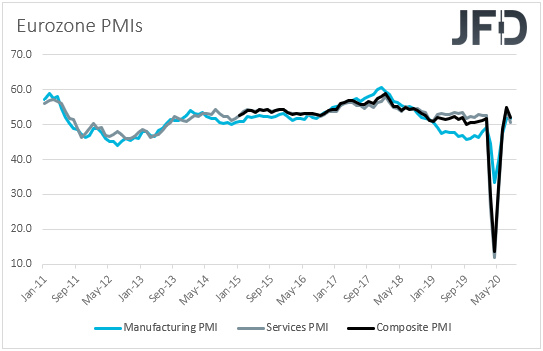

As for today, the main releases on the agenda may be the preliminary PMIs for September. During the EU trading, we get the PMIs from several Euro-area nations and the bloc as a whole. Eurozone’s manufacturing PMI is forecast to have risen somewhat, to 51.9 from 51.7, while the services index is anticipated to have held steady at 50.5. Strangely, this is expected to drag the composite index slightly lower, to 51.7 from 51.9.

At the prior ECB meeting, policymakers kept monetary policy untouched, reiterating that they stand ready to adjust all their instruments, as appropriate, to ensure that inflation moves towards its aim in a sustained manner. That said, although President Lagarde said that the risks of the economic outlook remain to the downside, the Bank’s GDP projections were revised slightly higher. Thus, small movements in the Euro area PMIs are unlikely to raise speculations that further easing is on the cards for the upcoming ECB gathering, which means that the euro is unlikely to move much if the actual prints come close to their forecasts. For speculation over an imminent action by the ECB to resurface, the PMIs may have to miss their forecasts by a large margin.

We get the preliminary PMIs for September from the UK and the US as well. The UK indices are forecast to have declined, and although they are expected to stay above 50, the new measures announced by the UK PM Johnson yesterday may be an omen for contracting prints for the month of October. With regards to the US indices, the manufacturing index is forecast to have ticked up to 53.2 from 53.1, and the services one to have declined to 54.7 from 55.0.

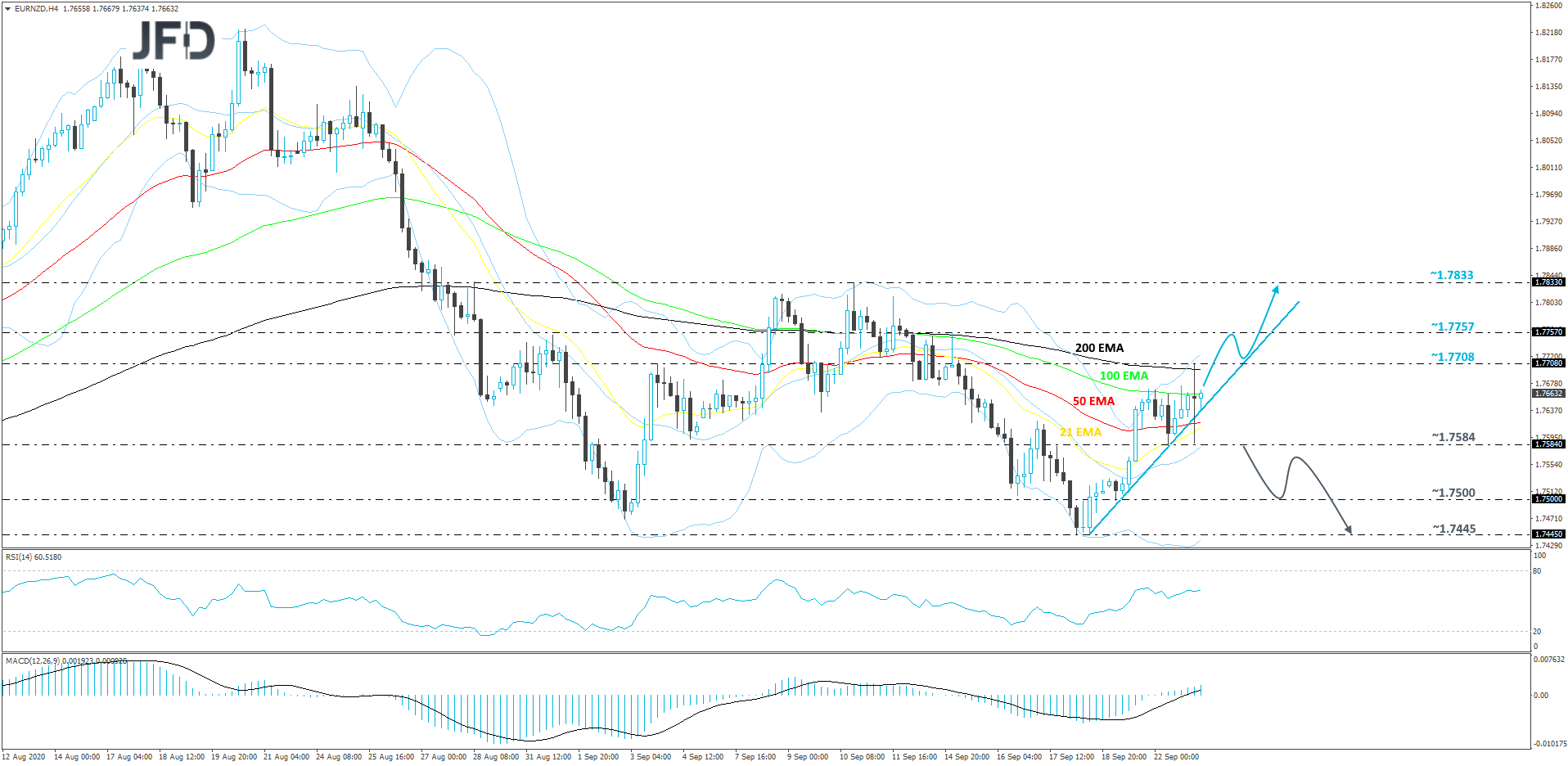

EUR/NZD – TECHNICAL OUTLOOK

After finding good support near the 1.7445 hurdle, EUR/NZD started moving north again and is currently balancing above a short-term tentative upside support line taken from the low of September 18th. Although the rate is still trading below the 200 EMA on our 4-hour chart, the pair seems to be showing willingness to climb higher, as the RSI and the MACD are pointing slightly to the upside. If EUR/NZD continues to move above that upside line, we will remain positive, at least for now.

If the bulls are able to push the rate further north to the 200 EMA, the pair might also test the 1.7708 zone, marked by this morning’s high. A failure by that zone to provide resistance could result in a move higher and a possible test of the 1.7757 area, marked by the high of September 15th, which could slowdown the acceleration. That said, if the buyers are still feeling comfortable, they may drive the rate to the 1.7833 level, which is the current highest point of September.

We will start considering lower areas if the rate suddenly breaks the aforementioned upside line and then slides below the 1.7584 hurdle, marked by yesterday’s low. That may spook the bulls from the field temporarily and allow more sellers to join in. EUR/NZD could then drift to the 1.7500 obstacle, a break of which might clear the way to the current lowest point of September, at 1.7445.

AS FOR THE REST OF TODAY’S EVENTS

The EIA (Energy Information Administration) report on crude oil inventories for last week is coming out. The forecast points to a 2.325mn barrels slide following a 4.389mn decline the week before. However, bearing in mind that the API (American Petroleum Institute) revealed a 0.691mn inventory build yesterday, we would consider the risks surrounding the EIA forecast as tilted to the upside.

We also have four Fed speakers on the agenda. Chair Powell will deliver its second speech before Congress, but we don’t expect any fireworks. Yesterday, the Fed Chief said that the economy had shown “marked improvement” since the pandemic drove it into recession, but the path ahead remains uncertain and that he and his colleagues will do more if needed. He also warned that the economic recovery would suffer if the government and Congress fail to pass a new fiscal stimulus package. We believe that today’s remarks will stay along those lines.

We will also get to hear from Cleveland President Loretta Mester, Chicago President Charles Evans, and Board Governor Randal Quarles. Evans, due to become a voter next year, said yesterday that the Fed “could start raising rates before we start averaging 2%” inflation. This enhances our view derived from the latest FOMC gathering, that not all members are in favor of waiting for inflation to overshoot the target for some time before raising rates. A reiteration of that notion may thereby keep the dollar supported, and perhaps add some pressure to equities.

{{youtube|{"id":"uL8dJd0-gCI","title":"Daily Market Review: Equities Rebound, RBNZ Stands Pat, PMIs in Spotlight"}}}