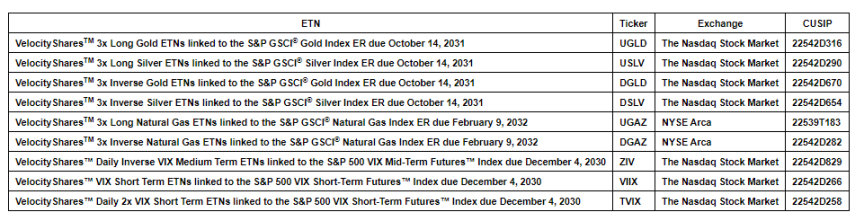

Following the XIV termination debacle in 2018, Credit Suisse (NYSE:CS) is trying to reduce its legal exposure dramatically by delisting a number of its highly volatile VelocityShares ETNs.

In a press release a couple of days ago, Credit Suisse announced that it will delist UGLD (3x Gold), USLV (3x Silver), DGLD (-3x Gold), DSLV (-3x Silver), UGAZ (3x Natural Gas), DGAZ (-3x Natural Gas), ZIV (Short Medium Term VIX futures), VIIX (1x VIX) and TVIX (2x VIX).

Many of these highly leveraged ETNs are just accidents waiting to happen given how volatile commodities have become during the COVID pandemic. A -30% loss in the underlying would bring one of these 3x leveraged ETNs close to termination. The 3x Silver and Natural Gas ETNs can easily lose -80% of their value within a week and have done so in the past. In some years, due to high volatility, both bull and bear 3x leverage ETNs have lost month. As a general rule, I don’t think “mom and pop” retail investors should have much exposure to 3x leverage ETNs as often they don’t understand the concept of volatility drag which is very detrimental to long-term performance. Many retail investors have lost fortunes with 3x leveraged ETNs. Credit Suisse getting out of the 3x leverage game for volatile commodities makes a lot of sense to me.

Credit Suisse is also getting completely out of volatility game. Why is that?

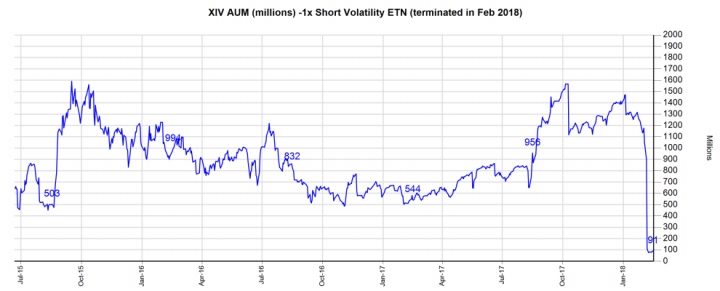

XIV (-1x VIX) ETN was one of the original financial products that made volatility trading popular among retail investors. XIV was developed at the end of 2010 by Velocity Shares and is issued by Credit Suisse (CS). After a difficult start in the first couple of years, XIV gathered a lot of interest by retail investors in 2013 after the Fed launched QE Infinity and signaled that it has added a 3rd mandate of “Financial Stability” to its Congressional mandates of “Maximum Employment” and “Price Stability”. “Financial Stability” meant that the Fed was actively targeting and suppressing volatility in stock markets which is measured by the VIX. The easiest way to take advantage of that Fed intervention for investors was to short the VIX via XIV. XIV became a popular product as the economy improved after 2013. XIV posted a few years of 100%+ returns and its AUM went as high as $1.5 billion on several occasions and was often the most traded exchange-traded product out there.

Towards the end of 2017, the short volatility trade became overcrowded ahead of the corporate tax cuts passed by Trump as many investors wanted to take advantage of the implied leverage in the VIX trade and boost their returns. The combined AUM of short volatility ETPs like XIV became larger than the overall needs of the S&P 500 hedging market they served and the short volatility trade became susceptible to a speculator attack.

In early 2018 during a flash SPX selloff, short volatility products were attacked by hedge fund speculators who took advantage of vulnerabilities in their daily rebalancing algorithms. XIV lost -90% of its value in one night and was terminated on February 6th, 2018 by Credit Suisse in an event referred to as “Volmageddon” in financial circles. Many investors lost massive amounts of money and they sued Credit Suisse in the aftermath. I consulted the plaintiffs in a couple of these lawsuits. After a couple of years, Credit Suisse was able to survive multiple XIV termination lawsuits without having to pay restitution to investors. But the legal fees stung badly and their management doesn’t want a repeat of the XIV episode with one of their other ETNs. Credit Suisse runs these ETNs to make money for itself, not for its lawyers.

After Volmageddon, while XIV got terminated, its twin brother SVXY survived but got deleveraged. Leverage in SVXY went from -1x to -0.5x. After the deleveraging, SVXY numerically became a carbon copy of ZIV. I ran a study at that time and found that over the long term the risk/reward for SVXY and ZIV is nearly identical even though they use slightly different underlyings.

Overall exposure to the VIX Futures market is basically the same except that SVXY provides better tax treatment. Since then ZIV has been struggling to attract investor flows. It has only $76 million in AUM and I am sure CS just doesn’t find operating it profitable. The other VIX ETN in the Credit Suisse portfolio was VIIX (1x VIX) which is a tiny ETN with 49 million that hasn’t been able to gain market share on VXX. After nearly a decade of existence having sub $100 million in AUM is a pretty sad state of affairs for both ZIV and VIIX. The products just don’t have a clientele and are barely profitable. Their operating costs used to be subsidized by XIV and TVIX but now that CS is shutting down TVIX, ZIV and VIIX can’t survive on their own. So I am not surprised at all that Credit Suisse is shutting down ZIV and VIIX.

The question here is why is Credit Suisse shutting down TVIX (2x VIX)?

TVIX is up 200%+ in 2020 and has about $1 billion in AUM. It is the most widely traded VIX exchange-traded product today. TVIX already had legal issues in 2012 when a huge disconnect between its NAV and its price developed after Credit Suisse temporarily suspended issuance of shares. Some investors lost money and there were lawsuits around that episode as well. Lately hedge funds have started targeting TVIX for a termination attack. They want to take it out like XIV by instigating a massive -50% overnight drop in the VIX. We had one such episode in March when TVIX went from $1000 to $200 in a week with some pretty scary overnight action. I am sure CS doesn’t want another XIV-like termination on its hands and more investor lawsuits in the middle of the COVID pandemic. Credit Suisse wants to cut its legal exposure and its legal costs. TVIX is a successful product but is becoming too hot to handle.

TVIX is going to get delisted on July 2nd (next Thursday). After July 3rd, CS will suspend new issuance of TVIX. After July 12th, TVIX can only be traded over the counter. Following the delisting, TVIX shares will remain outstanding but is likely that Credit Suisse will liquidate it soon after. It is probably best if you get out of TVIX before July 2nd as you don’t want to deal with an over the counter product which might trade at massive premium or discount to its NAV. Once issuance of new shares is suspended, there will be big tracking errors and this is a hassle that most retail investors don’t want to be dealing with. Instead, you can use UVXY (+1.5x VIX) if you want to have long VIX exposure. UVXY has slightly lower leverage than TVIX but it can provide a hedge just as suitable as TVIX in an SPX selloff. In the March SPX selloff, UVXY also went up 10 times like TVIX.

Credit Suisse put volatility trading on the map and opened a new chapter in investing history. It is sad to see it leave the game. But fear not, there are new products in the SEC pipeline that will improve on the functional deficiencies of the Credit Suisse products and will be more resilient to speculator attacks. Interest in volatility trading remains high and its future is bright. For now, if you need volatility exposure, you can use SVXY (-0.5x), VXX (+1x) and UVXY (+1.5x).

I want to conclude with an interesting takeaway here for investors: this move by Credit Suisse is telling you is that market turbulence in general is here to stay in coming years. We are entering a market regime in which Credit Suisse doesn’t think it can run 3x leveraged exposure on commodity or VIX products without an accident. That in and of itself is a great tell about the future. Strap on your seatbelts.