Market participants increased somewhat their risk exposure yesterday, but not much, as they may have remained unconvinced from Fed Chair Powell’s remarks that it is still too early to start normalizing monetary policy. We also had a BoC decision, with officials tapering their QE purchases further as expected, but noting that the output gap is still expected to close in the second half of next year, disappointing those expecting a more hawkish language. Tonight, the central bank torch will be passed to the BoJ, but we don’t expect any fireworks.

US Dollar Slides, But Equities Fail To Gain Much On Powell's Cautious Remarks

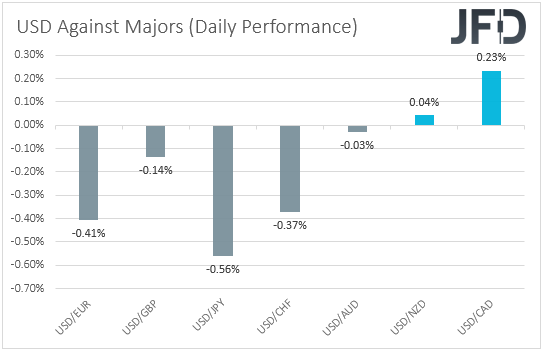

The US dollar pulled back against most of its major peers on Wednesday and during the Asian session Thursday. It gained only versus CAD and NZD in that order, while it lost the most ground against JPY, EUR, and CHF.

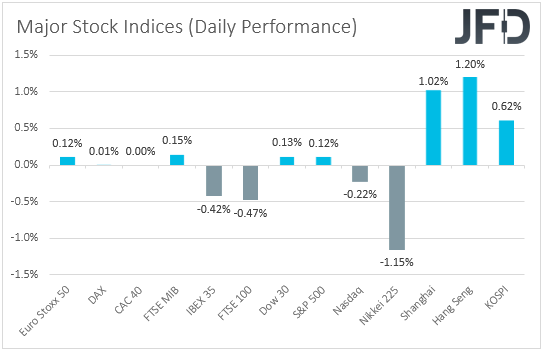

The weakening of the US dollar suggests that market sentiment may have improved at some point yesterday or today in Asia. However, the strengthening of the safe-havens yen and franc points otherwise. Thus, in order to get a clearer picture with regards to the broader market sentiment, we prefer to turn our gaze to the equity world. There, major EU indices traded unchanged or lower, with concerns over high inflation around the globe intensifying after the UK CPIs followed the footprints of the US ones and accelerated by more than anticipated. The only exceptions were the Euro Stoxx 50 and Italy’s FTSE MIB, which gained somewhat.

In the US, the Dow Jones and the S&P 500 traded slightly higher, with the latter hitting a fresh record high. However, NASDAQ ended its trading lower. Market sentiment was somewhat more improved during the Asian session today. Although Japan’s Nikkei 225 fell 0.98%, China’s Shanghai Composite, Hong Kong’s Hang Seng, and South Korea’s KOSPI traded in the green.

Yesterday, when testifying before Congress’s House of Representatives Financial Services Committee, Fed Chief Powell said the US economy is "still a ways off" from levels the Committee wants to see before they start normalizing monetary policy. He also added that he still believes the recent rally in inflation is due to the nation’s post-pandemic reopening that that it will prove to be temporary. That said, with data the day before showing that underlying inflation pressures hit their highest since November 1991, many participants may have found it difficult to rely on his remarks. That’s why equities did not rebound confidently, and although the US dollar pulled back, the yen and the franc remained supported. This was also evident by the fact that market participants did not alter much their bets over when they expect the Fed to hit the hike button. Ahead of Powell’s testimony, they were anticipating such a move to take place in January 2023. In the aftermath, that timing was moved just a month back. In other words, expectations are now for the first Fed hike to happen in February 2023.

As for our view, we are reluctant to rely on Powell as well. Many Fed members have already expressed their desire for raising interest rates as soon as next year, while, most importantly, underlying inflation, which excludes volatile items such as energy and food, has more than doubled the Fed’s objective of 2%. So, how much of this is transitory? We believe that the US dollar could rebound again soon, but we don’t expect equities to fall. We may see some pullbacks, but we stick to our guns that, now, equity investors are likely to stay more focused on second-quarter earnings, with expectations pointing to decent results. Today, Powell will deliver the same testimony before the Senate Banking Committee, but we don’t expect any surprises. He is very likely to stick to the view that it’s too early to start normalizing policy, and that’s why we don’t believe that we will see strong market moves today.

AUD/JPY Technical Outlook

AUD/JPY drifter lower yesterday and today in Asia, falling below the 82.08 level, which provided support on Monday and Tuesday. Overall, the pair remains below the downside resistance line taken from the high of May 10, which combined with the dip below 82.08, suggests that further declines may be looming in the short run.

In our view, the dip below 82.08 may have opened the path toward the lows of July 8 and 9, at around 81.32, where another break would confirm a forthcoming lower low on the daily chart and perhaps allow the slide to extend towards the low of February 12, at 81.07. If the bears are not willing to stop there, then a break lower may see scope for extensions towards the 80.67 zone, which supported the price action on February 9 and 11.

Now, in order to start examining a decent correction to the upside, we would like to see a break above 82.80. Such a move would confirm a forthcoming higher high on the 4-hour chart and may initially pave the way towards the high of July 7, at 83.45, or the inside swing low of July 5, at 83.41. Another break, above 83.41, could extend the recovery towards the aforementioned downside line drawn from the high of May 10, or towards the 84.20 territory, defined as a resistance by the high of July 6.

Bank Of Canada Tapers Further, But Timing Of Output and Gap Closing Stays Unchanged

Apart from Powell’s testimony, yesterday, we also had a BoC monetary policy decision. Canadian policymakers kept their interest rates unchanged and reduced further their QE purchases pace, to CAD 2bn per week from CAD 3bn, as was broadly expected. However, still, the Canadian dollar fell after the decision, to be found as the main loser among the major currencies this morning. In our view, given that the tapering was largely anticipated, Loonie traders focused on other parts in the statement, and specifically on the part saying that officials continue to see the output gap closing in H2 2022. What’s more, at the press conference following the decision, BoC Governor Tiff Macklem said that the outlook is “not really that different” from April. It seems that CAD-traders may have been looking for something more hawkish, perhaps something to suggest that interest rates are likely to be lifted earlier than previously thought. However, saying that the output gap is still expected to close at the same time as was forecast in April, means that the estimated timing for a rate hike has not changed.

In our view, yesterday’s decision changes the narrative around the Loonie. Following a very hawkish RBNZ, we believe that the Canadian currency may now well underperform the Kiwi, even if it performs somewhat better against the Aussie, due to the dovish RBA. We believe that the Loonie could continue underperforming even against the US dollar as, from what we saw yesterday, investors may have remained unconvinced that the Fed will be patient in deciding to start scaling back monetary policy support. Many of them could still be expecting a QE tapering process to start in the next few months. So, long story short, we do believe that NZD/CAD will strengthen in the foreseeable future, but we also see decent chances for USD/CAD to continue drifting north for a while more as well.

USD/CAD Technical Outlook

USD/CAD triggered some buy orders near the 1.2425 level yesterday following the BoC decision, with the rate returning back above the 1.2490 zone. Overall, the price structure continues to suggest a short-term uptrend above the upside support line drawn from the low of June 10, and thus, we would consider the near-term outlook of this exchange rate to still be positive.

We believe that the bulls are likely to stay in the driver’s seat for a while more, and perhaps push the action towards the high of July 8, at 1.2590. If they are willing to overcome that hurdle, then their move will confirm a forthcoming higher high on the daily chart and perhaps open the way towards the 1.2627 hurdle, which prevented the bulls from sailing further north several times between Mar. 25 and Apr. 21. If the buyers manage to win the battle near that zone this time around, then we may experience extensions towards the peak of Mar. 8, at around 1.2700.

On the downside, the move that could signal a short-term bearish reversal may be a dip below yesterday’s low of 1.2425. This may also take the rate below the aforementioned upside line and could initially target the inside swing high of July 5, at around 1.2370. A break below that barrier could see scope for larger bearish extensions, perhaps towards the low of the day after, at 1.2300, or the low of June 23, at 1.2252.

As For Today's Events

During the Asian session, we already got Australia’s employment report for June, as well as China’s GDP for Q2, which was accompanied by the fixed asset investment, industrial production, and retail sales, all for June. Australia’s unemployment rate fell by more than expected, but the net change in employment showed that the economy added less jobs than anticipated. In our view, this is unlikely to tempt the RBA to take off its dovish dress.

As for the Chinese data, although the Chinese economy slowed by more than expected in yoy terms, the qoq rate was higher than its own forecast, while IP, FAI and retail sales, all slowed by less than expected, adding to the view that the world’s second largest economy has performed very well during the period. This may have been the catalyst behind the increased risk appetite during the Asian trading today.

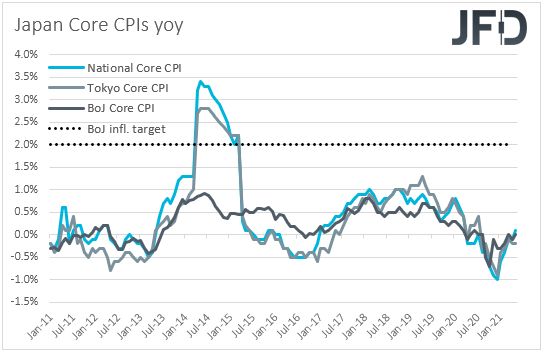

Tonight, during the Asian session Friday, the central bank torch will be passed to the BoJ. Its latest meeting resulted in no fireworks, with officials maintaining their policy unchanged and extending the deadline for pandemic-related programs by six months, as was mainly expected to happen at that gathering, or the one scheduled for this week. With both Japan’s headline and core inflation rates around the zero mark, we don’t expect this Bank to adopt a similar stance to other major central banks and start sending signals with regards to whether and when it could start normalizing its policy. We expect policymakers to keep their foot on the extra-loose pedal and perhaps signal that they are willing to leave it there for long. Although, under normal circumstances, a dovish language may have been proven negative for the Japanese yen, we don’t expect the yen to suffer much after the decision, especially if FX traders start repricing an earlier tightening move by the Fed. Worries over the Delta coronavirus variant could also keep this safe-haven currency supported.

As for the speakers, besides Fed Chair Powell, who will repeat his testimony, we will also get to hear from Chicago Fed President Charles Evans, ECB Executive Board member Frank Elderson and BoE MPC member Michael Saunders.