- CPI inflation, Fed FOMC minutes, start of Q1 earnings season in focus.

- JPMorgan Chase is a buy with strong earnings beat on deck.

- Delta Air Lines is a sell with weak earnings, guidance expected.

- Looking for more actionable trade ideas? Join InvestingPro for under $9 a month for a limited time only and never miss another bull market by not knowing which stocks to buy!

U.S. stocks ended higher on Friday, as investors digested a U.S. jobs report that showed hiring rose much more than expected in March while wage growth slowed.

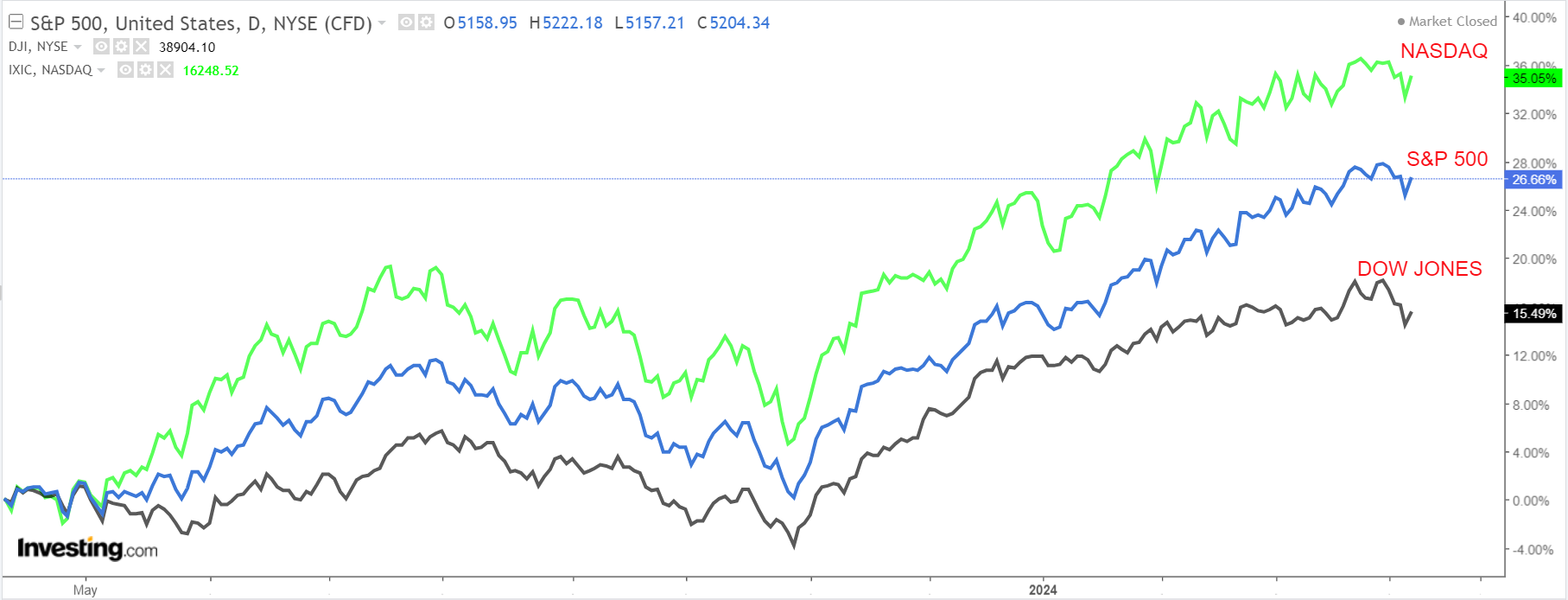

Despite Friday’s bounce, all three indexes still ended the week in negative territory. The benchmark S&P 500 declined 1% during the period, while the tech-heavy Nasdaq Composite dropped 0.8%.

The blue-chip Dow Jones Industrial Average lagged, falling 2.3% to suffer its worst weekly performance in 2024.

Source: Investing.com

The week ahead is expected to be another eventful one as investors continue to look for more cues on the prospects for potential rate cuts.

On the economic calendar, most important will be Wednesday’s U.S. consumer price inflation report for March, which is forecast to show headline annual CPI rising 3.4%, compared to the 3.2% increase recorded in February.

The CPI data will be accompanied by the release of the latest figures on producer prices, which will help fill out the inflation picture.

Source: Investing.com

Meanwhile, the minutes of the Federal Reserve’s March FOMC policy meeting, due on Wednesday, will also be closely watched.

As of Sunday morning, financial markets see just a 53% chance of the Fed cutting rates in June, according to the Investing.com Fed Monitor Tool, down from over 90% a few weeks ago.

Elsewhere, the Q1 earnings season officially kicks off on Friday, with JPMorgan Chase (NYSE:JPM), Wells Fargo (NYSE:WFC), Citigroup (NYSE:C), and BlackRock (NYSE:BLK) all scheduled to release quarterly results.

Regardless of which direction the market goes, below I highlight one stock likely to be in demand and another which could see fresh downside. Remember though, my timeframe is just for the week ahead, Monday, April 8 - Friday, April 12.

Stock To Buy: JPMorgan Chase

I expect another strong performance from JPMorgan Chase (NYSE:JPM) this week, with shares likely to break out to a new record high, as the banking powerhouse’s latest financial results will surprise to the upside in my view thanks to a solid performance across its key business segments.

JPMorgan is scheduled to deliver its first quarter earnings report ahead of the opening bell on Friday at 6:55AM EST, with both analysts and investors growing increasingly bullish about the Jamie Dimon-led megabank.

Market participants expect a possible implied move of around 3% in either direction in JPM shares following the update. The stock dipped 0.7% after its last earnings report in January.

Despite seeing eight out of the 11 analysts surveyed by InvestingPro downwardly revise their profit and revenue forecast ahead of the print, estimates for both are still substantially higher than where they were initially.

Source: InvestingPro

Consensus estimates call for JPMorgan Chase to post Q1 earnings per share of $4.13, rising about 1% from EPS of $4.10 in the year-ago period.

Meanwhile, revenue is forecast to jump 8.9% year-over-year to $41.7 billion, which if confirmed would mark the megabank’s highest quarterly sales total in its history, thanks to solid growth in its retail banking division.

In addition, I anticipate fixed income trading revenue, equity trading revenue, and investment banking revenue to all beat consensus expectations as the Wall Street behemoth benefits from increased trading activity.

As such, I believe JPM CEO Jamie Dimon is poised to offer an upbeat outlook for the months ahead, buoyed by the banking giant’s advantageous position amid the resurgence in global deal-making, merger activity, and IPO underwriting.

JPM stock ended Friday’s session at $197.45, just below the record high close of $200.30 from March 28. At current levels, JPMorgan Chase has a market cap of $568.7 billion, earning the New York-based financial services firm the title of the most valuable bank in the world.

Source: Investing.com

Shares have been on a major uptrend since the start of 2024, gaining 16% so far this year as the company benefits from improving economic conditions, robust demand for banking services, and a supportive regulatory environment.

As ProTips points out, JPMorgan Chase is in great financial health condition, thanks to strong earnings and revenue growth prospects, combined with its attractive valuation and pristine balance sheet. Additionally, it should be noted that the megabank has maintained its dividend payout for 54 consecutive years.

Stock to Sell: Delta Air Lines

I foresee a disappointing week ahead for Delta Air Lines (NYSE:DAL) as the legacy air carrier’s first quarter earnings and forward guidance will likely underwhelm investors due to the challenging operating environment.

Delta is forecast to release its Q1 update before the U.S. market opens on Wednesday at 6:30AM ET amid mounting geopolitical and economic uncertainties.

According to the options market, traders are pricing in a swing of about 6% in either direction for DAL stock following the print. Notably, shares plunged 9% after the company’s Q4 report in January.

Underscoring several near-term challenges Delta is facing amid the current backdrop, three out of the seven analysts surveyed by InvestingPro slashed their EPS estimates in the last 90 days to reflect a drop of approximately 58% from their initial expectations.

Source: InvestingPro

Wall Street sees the Atlanta, Georgia-based airliner earning $0.36 a share in the March quarter, rising 44% from EPS of $0.25 in the year-ago period, while revenue is forecast to increase 9.5% annually to $12.9 billion.

But as is usually the case, it is more about forward-looking guidance than results.

As such, it is my belief that Delta’s management will provide a disappointing outlook for fiscal 2024 and strike a cautious tone amid soft consumer spending and declining operating margins.

In addition, fears surrounding the ongoing conflict in the Middle East and concerns about the impact of soaring oil prices on profitability will also be in focus.

DAL stock ended at $46.06 on Friday. Shares - which have gained 14.5% year-to-date - climbed to a 2024 peak of $49.20 on April 1, a level not seen since July 13, 2023.

Source: Investing.com

At current valuations, Delta has a market cap of about $29 billion, making it the most valuable U.S. airline company, ahead of industry peers such as Southwest Airlines (NYSE:LUV), United Airlines (NASDAQ:UAL), and American Airlines (NASDAQ:AAL).

It should be noted that Delta’s short-term outlook for profitability and cash flow appears risky, as per InvestingPro, which flag rising fuel prices, and increasing aircraft maintenance costs as causes for concern.

Be sure to check out InvestingPro to stay in sync with the market trend and what it means for your trading.

Readers of this article enjoy an extra 10% discount on the yearly and bi-yearly plans with the coupon codes PROTIPS2024 (yearly) and PROTIPS20242 (bi-yearly).

Subscribe here and never miss a bull market again!

Disclosure: At the time of writing, I am long on the S&P 500, and the Nasdaq 100 via the SPDR S&P 500 ETF (SPY), and the Invesco QQQ Trust ETF (QQQ). I am also long on the Technology Select Sector SPDR ETF (NYSE:XLK).

I regularly rebalance my portfolio of individual stocks and ETFs based on ongoing risk assessment of both the macroeconomic environment and companies' financials.

The views discussed in this article are solely the opinion of the author and should not be taken as investment advice.