Bitcoin price today: dips to $92k ahead of PCE inflation, potential Fed cut

Introduction & Market Context

Harvard Bioscience (NASDAQ:HBIO) released its third-quarter 2025 earnings presentation on November 6, revealing mixed results that included an earnings per share miss despite operational improvements. The company’s stock reacted negatively in premarket trading, dropping 1.36% to $0.597, reflecting investor concerns despite management’s emphasis on strengthening fundamentals.

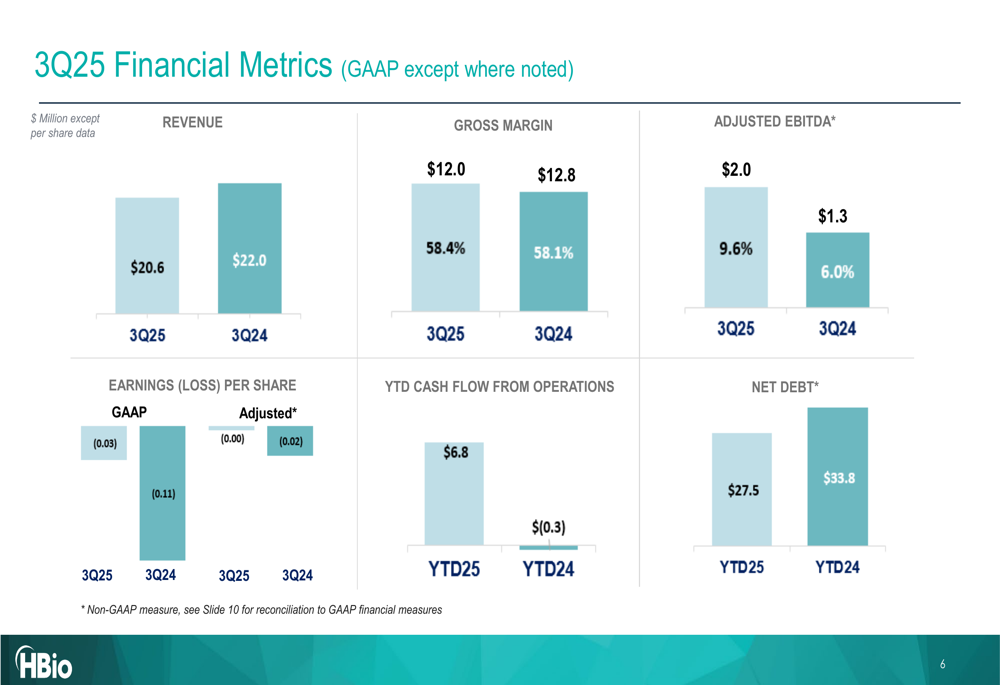

The life sciences tools provider reported revenue of $20.6 million, exceeding analyst expectations of $19 million but still representing a year-over-year decline from $22.0 million in Q3 2024. The company’s EPS of -$0.03 missed the forecasted $0.01, creating a negative surprise of 400% that overshadowed other operational gains.

Quarterly Performance Highlights

Harvard Bioscience highlighted several positive developments in its third-quarter presentation, including improved profitability metrics and strong cash flow generation despite the revenue decline. The company reported operating income of $0.2 million, a significant improvement from the $1.9 million loss in the same period last year.

As shown in the following financial highlights chart, gross margin improved slightly to 58.4% from 58.1% in Q3 2024, while adjusted EBITDA increased to $2.0 million from $1.3 million:

The company also emphasized substantial improvements in cash flow and debt reduction. Year-to-date cash flow from operations reached $6.8 million, compared to -$0.3 million in the same period last year, while net debt decreased to $27.5 million from $33.8 million.

These key financial metrics demonstrate the company’s progress in operational efficiency despite revenue challenges:

Detailed Financial Analysis

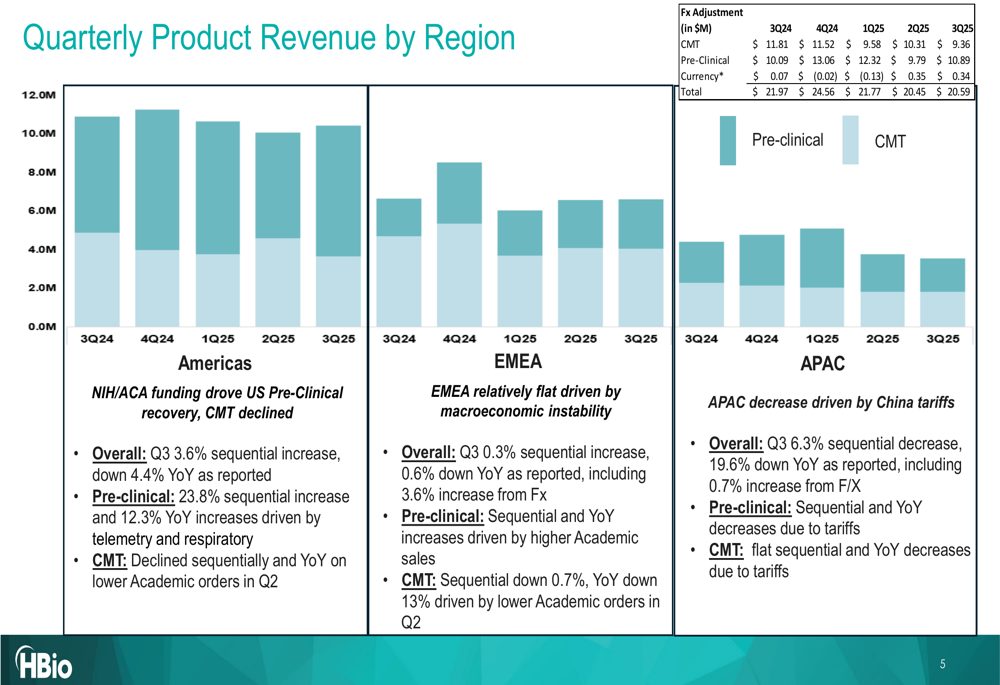

Harvard Bioscience’s regional performance showed significant variations, with recovery in the Americas offset by weakness in Asia-Pacific. The company reported that NIH/ACA funding drove US pre-clinical recovery, while China tariffs negatively impacted APAC performance.

The following regional breakdown illustrates these geographical differences in product revenue:

By segment, pre-clinical products showed strength with a 23.8% sequential increase and 12.3% year-over-year growth, driven by telemetry and respiratory products. In contrast, the Cell & Molecular Technologies (CMT) segment declined both sequentially and year-over-year, attributed to lower academic orders in the previous quarter.

Management noted that the company has achieved the highest backlog in nearly two years, suggesting potential future revenue growth despite current challenges. This backlog growth appears uniform across geographies and products, according to comments from CFO Mark Frost during the earnings call.

Forward-Looking Statements

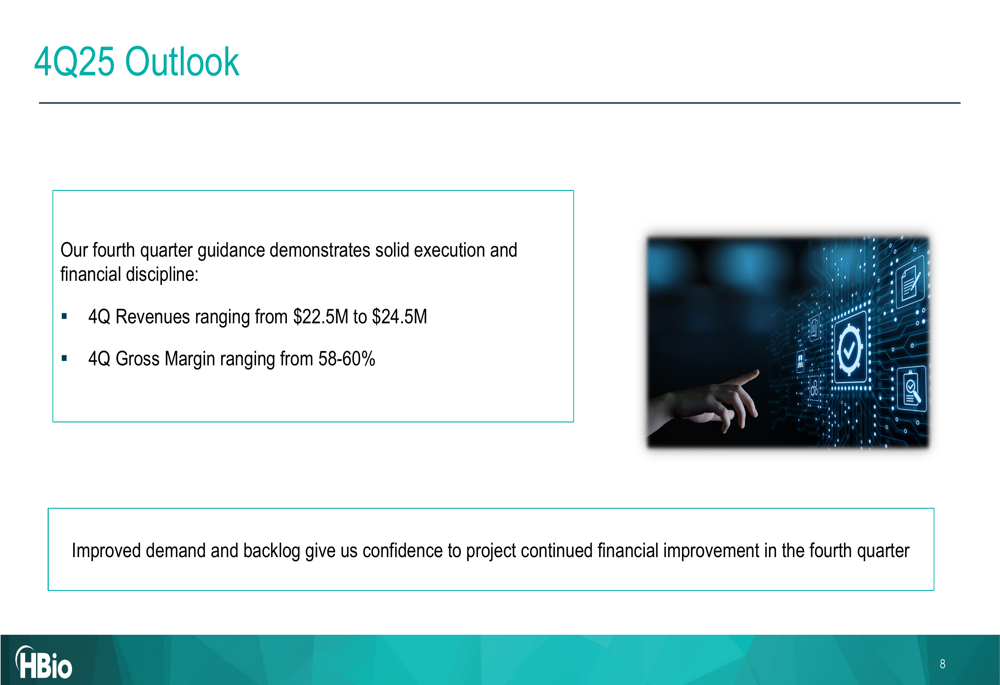

Looking ahead, Harvard Bioscience provided guidance for the fourth quarter of 2025, projecting revenue between $22.5 million and $24.5 million with gross margin ranging from 58% to 60%. This outlook suggests sequential improvement from Q3 results.

The company’s Q4 guidance is presented as follows:

CEO John Duke emphasized that Harvard Bioscience is "a fundamentally stronger company today than it was to start the year: leaner, more focused, and better aligned with long-term growth opportunities." Management highlighted three key priorities for the remainder of 2025: maintaining financial discipline, accelerating product adoption, and strengthening the capital structure.

However, the company faces several challenges, including potential disruptions from a U.S. government shutdown affecting NIH funding, continued revenue challenges in the China/APAC region, and execution risks related to new product launches. Additionally, the company disclosed ongoing discussions with lenders regarding its credit agreement, indicating potential changes to its capital structure.

Harvard Bioscience’s stock remains near its 52-week low of $0.281, despite trading at $0.597 in premarket activity, suggesting continued investor caution about the company’s turnaround efforts despite the operational improvements highlighted in the presentation.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.