"We jumped the gun": Morgan Stanley reverts back to call for December Fed rate cut

Introduction & Market Context

Haemonetics Corporation (NYSE:HAE) presented its second quarter fiscal 2026 results on November 6, 2025, revealing a strong performance despite revenue headwinds from portfolio transitions. The market responded enthusiastically, with HAE shares surging 22.06% in regular trading following a 12.38% gain in pre-market activity.

The medical technology company, which specializes in blood and plasma collection devices and related products, demonstrated its ability to drive profitability improvements and cash generation even as it navigates strategic portfolio changes. The company’s stock reached $61.91, well above its 52-week low of $47.32, though still below its 52-week high of $94.99.

Quarterly Performance Highlights

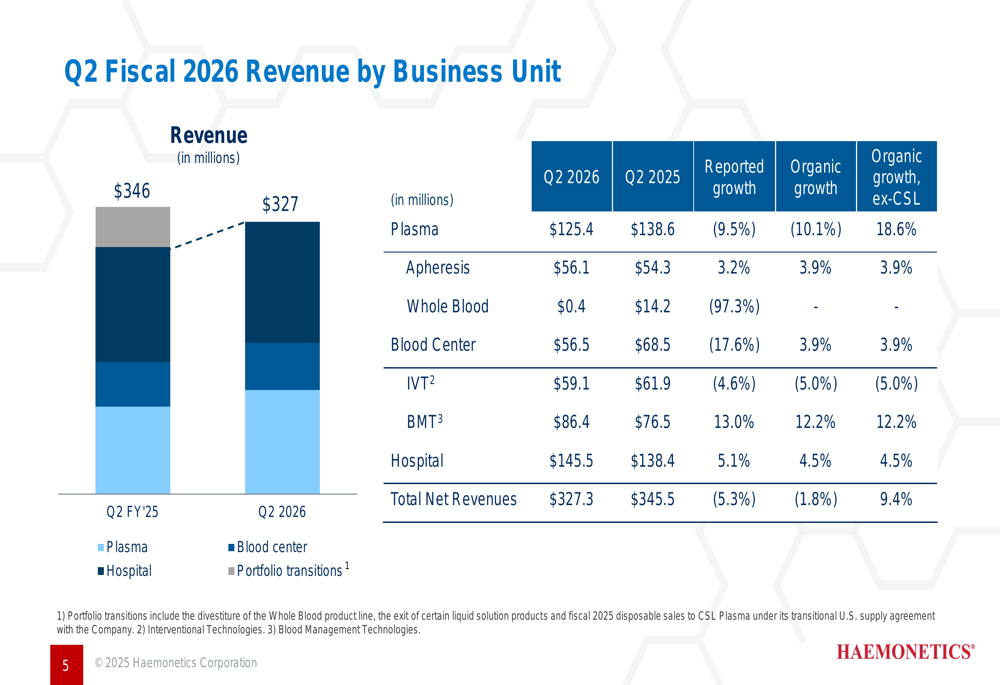

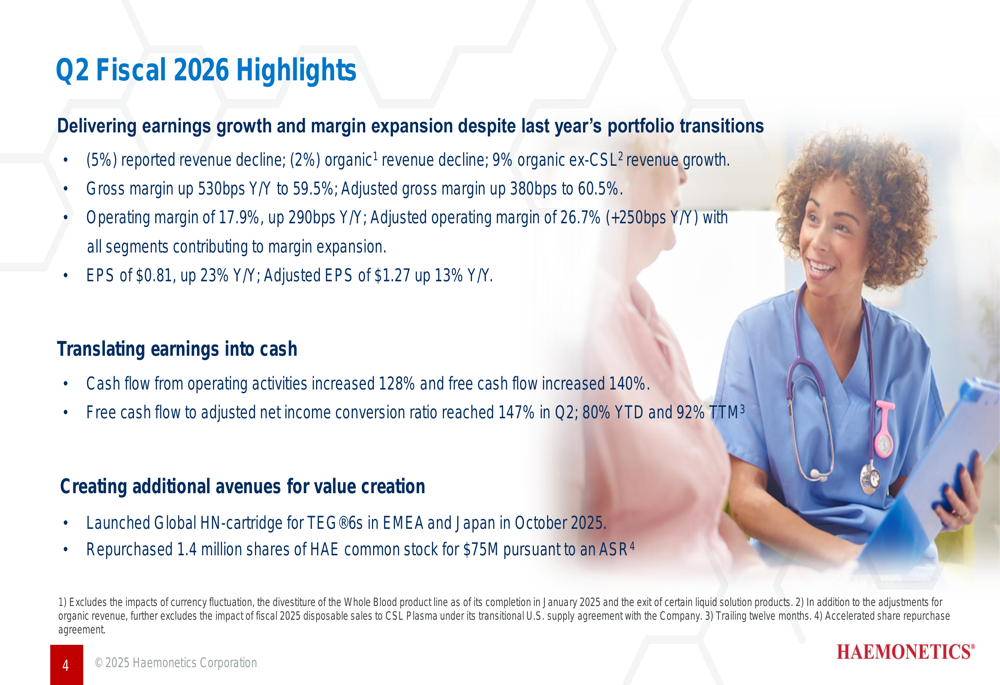

Haemonetics reported a 5.3% reported revenue decline to $327.3 million for Q2 fiscal 2026, reflecting the impact of portfolio transitions, particularly the divestiture of its Whole Blood business. However, when excluding the CSL impact, the company achieved 9.4% organic revenue growth, demonstrating the strength of its core business.

The company’s performance varied across its three main segments. The Plasma segment reported revenue of $125.4 million, down 9.5% on a reported basis but up 18.6% on an organic basis excluding CSL. The Blood Center segment saw a 17.6% reported revenue decline to $56.5 million, primarily due to the Whole Blood divestiture, but achieved 3.9% organic growth. The Hospital segment delivered 5.1% reported growth to $145.5 million, with strong performance in the Blood Management Technologies (BMT) business, which grew 13.0%.

As shown in the following breakdown of revenue by business unit:

Detailed Financial Analysis

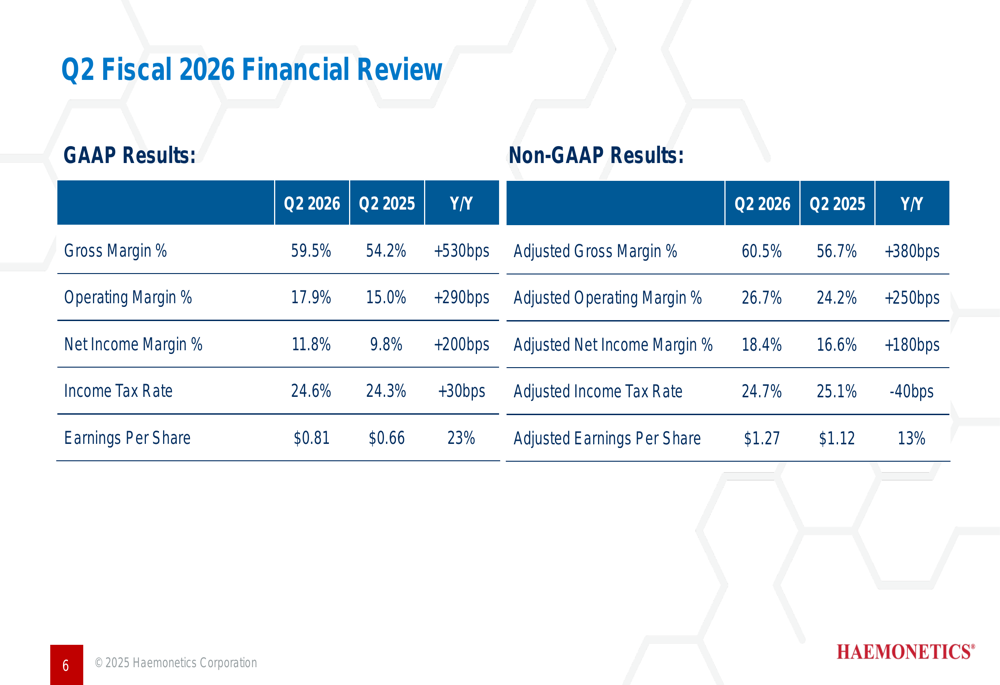

Despite the revenue challenges, Haemonetics delivered impressive margin expansion across all segments. The company’s gross margin increased 530 basis points year-over-year to 59.5%, while adjusted gross margin rose 380 basis points to 60.5%. Operating margin improved 290 basis points to 17.9%, and adjusted operating margin expanded 250 basis points to 26.7%.

This margin improvement translated into strong earnings growth, with GAAP earnings per share increasing 23% to $0.81 and adjusted earnings per share rising 13% to $1.27, exceeding analyst expectations of $1.11.

The company’s financial performance is summarized in the following slide:

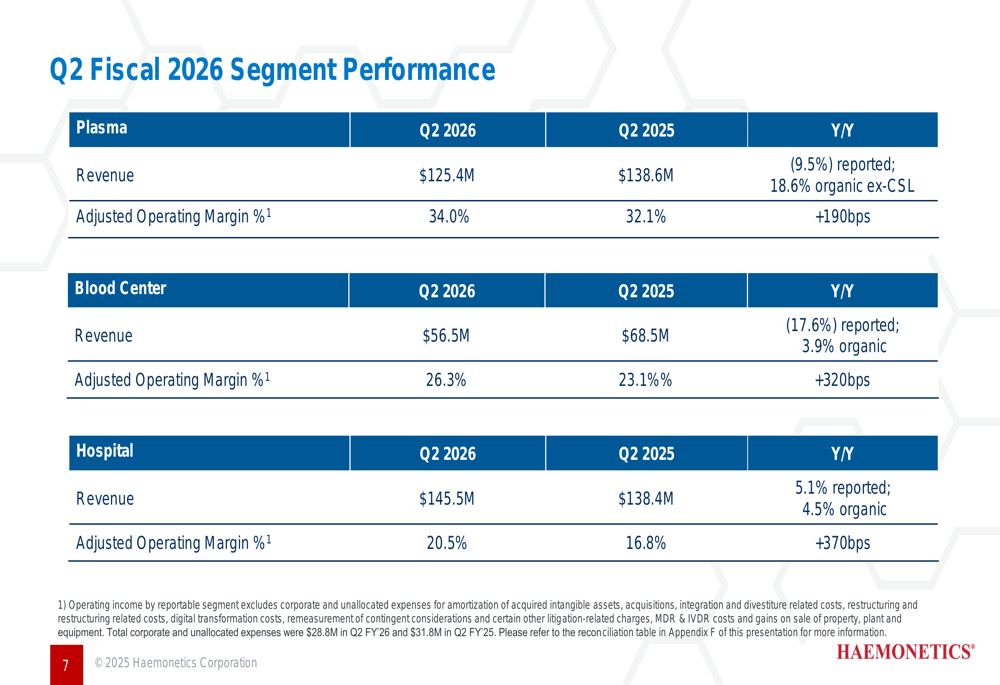

All three business segments contributed to the margin expansion. The Plasma segment achieved a 34.0% adjusted operating margin, up 190 basis points. The Blood Center segment’s adjusted operating margin increased 320 basis points to 26.3%, while the Hospital segment saw a 370 basis point improvement to 20.5%.

The segment performance details are illustrated here:

Cash Flow and Balance Sheet Strength

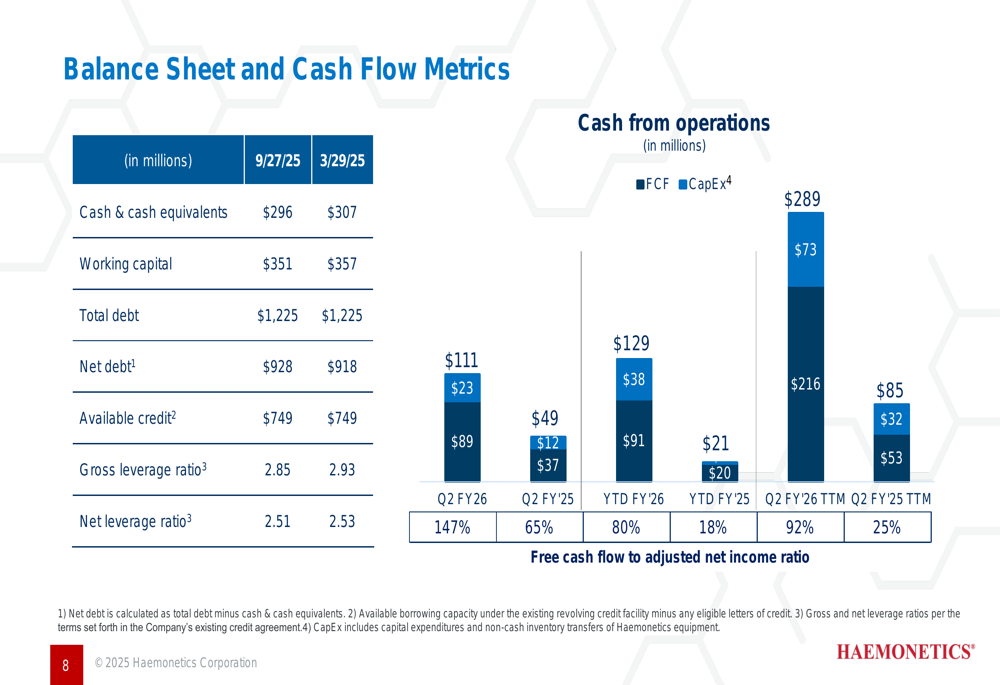

One of the most impressive aspects of Haemonetics’ quarterly performance was its cash generation. Cash flow from operating activities increased 128% year-over-year, while free cash flow surged 140%. The free cash flow to adjusted net income conversion ratio reached 147% in Q2, compared to 65% in the same period last year.

The company maintained a solid balance sheet with $296 million in cash and cash equivalents as of September 27, 2025. Total debt remained stable at $1,225 million, resulting in a net leverage ratio of 2.51, slightly down from 2.53 at the end of fiscal 2025.

The following slide details the company’s balance sheet and cash flow metrics:

Strategic Initiatives

During the quarter, Haemonetics continued to execute on its strategic initiatives. The company launched the Global HN-cartridge for its TEG®6s system in EMEA and Japan in October 2025, expanding its product portfolio in key international markets.

The company also returned value to shareholders through its share repurchase program, buying back 1.4 million shares of common stock for $75 million through an accelerated share repurchase (ASR) program.

As highlighted in the company’s quarterly summary:

Forward-Looking Statements

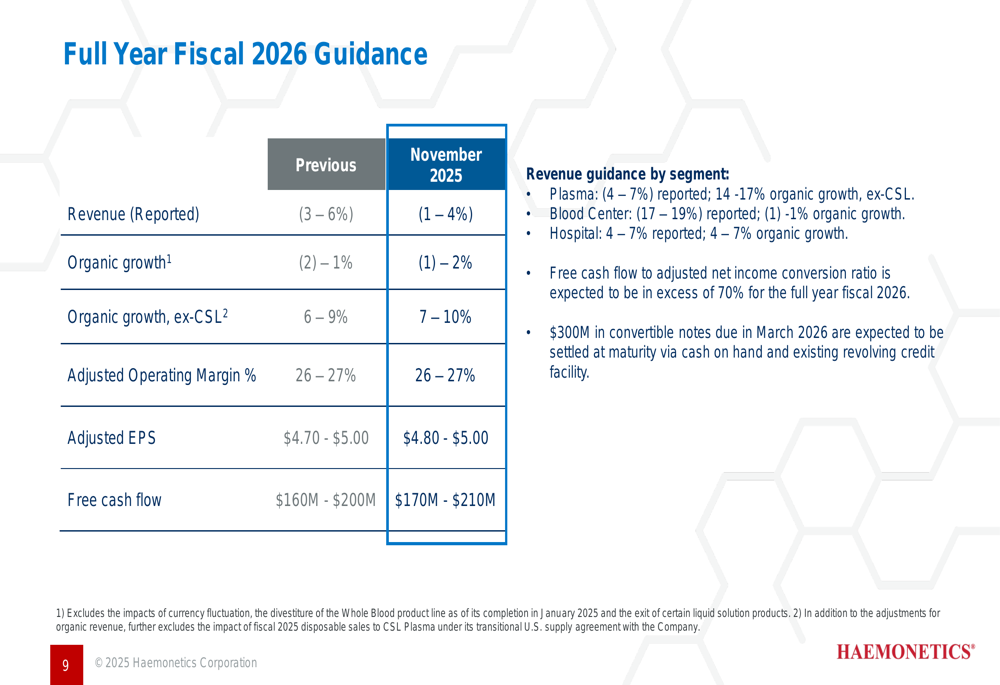

Based on the strong performance in the first half of fiscal 2026, Haemonetics raised its full-year guidance. The company now expects a reported revenue decline of 1-4%, improved from the previous guidance of 3-6% decline. Organic growth is projected at -1% to 2%, while organic growth excluding CSL is expected to be 7-10%, up from the previous guidance of 6-9%.

The adjusted earnings per share guidance was raised to $4.80-$5.00, compared to the previous range of $4.70-$5.00. Free cash flow guidance was also increased to $170-$210 million from $160-$200 million.

The updated guidance is detailed in the following slide:

During the earnings call, CEO Chris Simon expressed optimism about the plasma segment, stating, "Plasma goes from strength to strength. We’re very optimistic about its continued success." CFO James D’Arecca highlighted the importance of core products, saying, "Our growth and profitability are anchored in the success of our three core products, Nexus, TEG, and vascular closure."

Despite the positive outlook, Haemonetics faces challenges including competitive pressures in the vascular closure market, potential integration challenges with the upcoming Vivasure acquisition, and macroeconomic uncertainties that could impact global operations.

Overall, Haemonetics’ Q2 fiscal 2026 results demonstrate the company’s ability to drive profitability improvements and cash generation while navigating strategic portfolio transitions. The market’s positive reaction reflects confidence in the company’s strategy and improved outlook for the remainder of fiscal 2026.

Full presentation:

This article was generated with the support of AI and reviewed by an editor. For more information see our T&C.