As last week came to an end, we saw a further temporary reprieve in risk-off, with the ongoing USD long liquidation finding a new leg as the US and China lay the ground and prepare for mid-level trade talks on Aug 21-22 that may somehow contribute to disentangle the current trade war between the two countries. A planned US President Trump-Chinese Leader Xi meeting is not scheduled until a multilateral summit in November though.

The current market dynamics remain very much dependent on the binary outcomes of whether the relaxation in risk aversion we’ve seen can be sustainable or will it be re-ignited, in which case it should lead to dominant safe-haven bids, set to benefit the likes of the US Dollar, the Japanese Yen, and the Swiss Franc; these three would be the first refugee camp that investors will resort to, should the risk-off tone make a comeback. As the chart below illustrates, the risk environment is far from the benign conditions experienced back in 2017, where a stage 2 risk trend was in play.

Risk-weighted index: Death cross (50 & 100 SMA)

The Aussie and the Kiwi remain the most exposed to a return of risk-off flows as the favorite proxy plays to concerns over a prolonged Chinese-US trade war and/or spillover contagion effects of the Turkish crisis into the wider spectrum of the emerging markets. Technically, both pairs have embarked upon a short-term corrective move within the context of solid bearish trends, which was solidified by the breakout of the DXY above a major resistance. From a fundamental standpoint, the Kiwi appears to be especially fragile to further sell pressure as the RBNZ stance has turned more cautious on rate rises. On the flips side, fundamentally speaking the Australian Dollar appears increasingly supported by the latest data that further substantiates the strong labor market in Australia as the unemployment rate heads towards 5%.

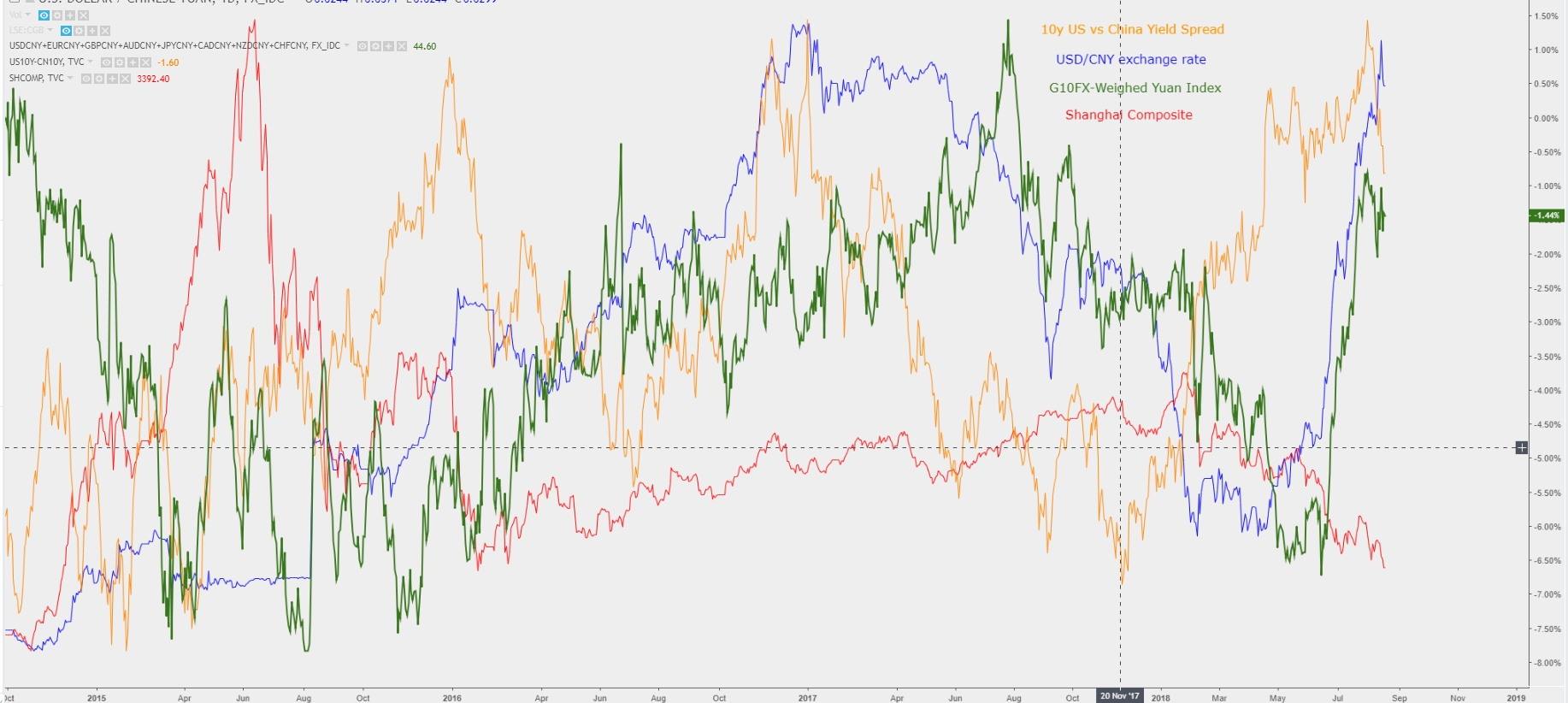

In the week ahead, keep monitoring the Chinese Yuan, as its performance over coming weeks can easily be one of the driving forces to drive risk flows. For now, since the mid-level trade talks this week were announced, there has been a reprieve in the current bullish trend, despite the hefty levels it trades at (near 6.90) are a reminder that a worsening of the current bleep in risk environment may have various forces acting as catalysts, the Renminbi being one of the familiar culprits to follow. That said, the People’s Bank of China has made it more difficult to short the Yuan in recent weeks, after imposing a reserve requirement of 20 percent on some trading of foreign-exchange forward contracts, which adds to the news of the spike in the forward curve in USD/CNH. 1-year forwards, which essentially makes it even more costly to bet on short Yuans for the capital that is unable to gain access into the onshore Yuan market. Besides, the Shanghai Composite is yet to a realignment with the improved risk mood, teetering on the brink of its lowest levels since Dec 2014.

Performance of the CH market underwhelming amid a weak Yuan

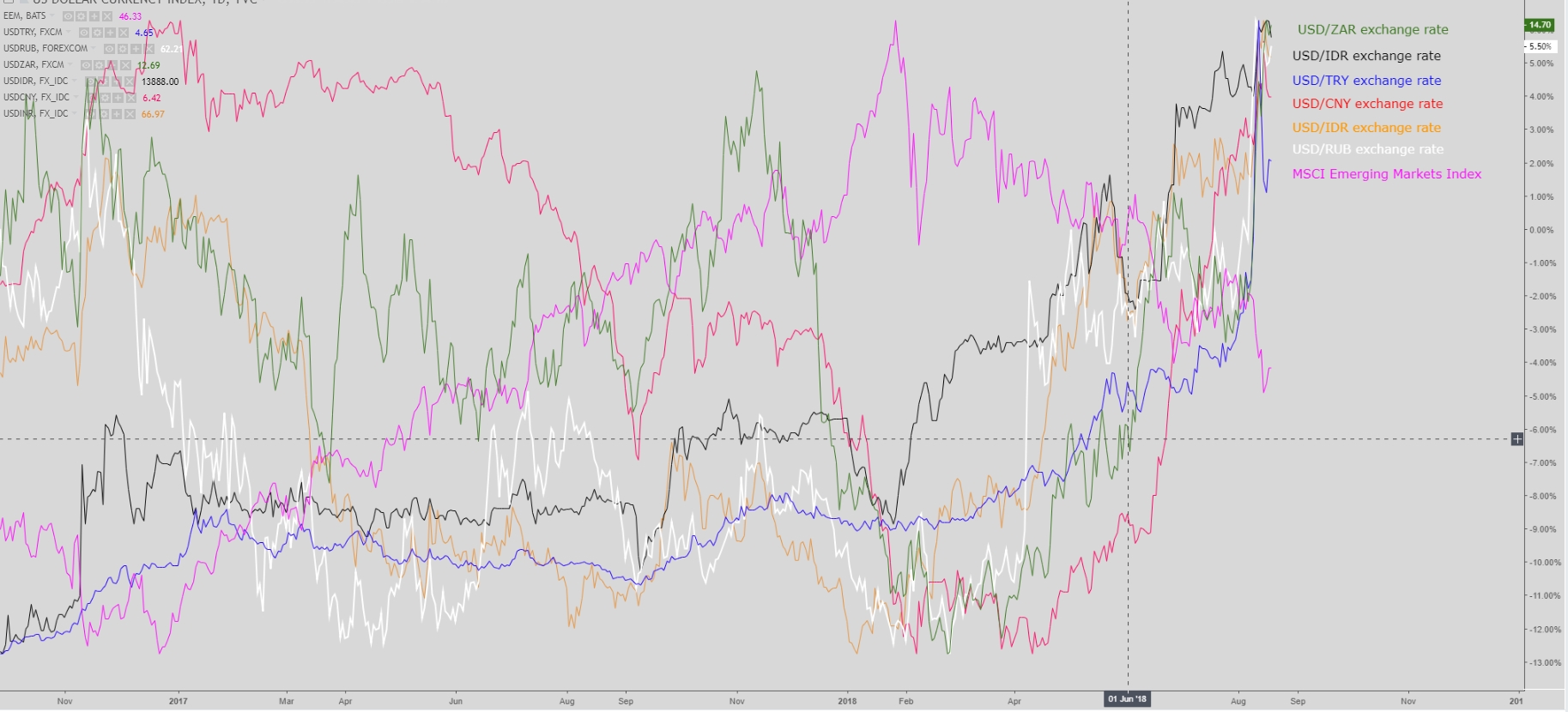

Further evidence that the market continues to walk on a tightrope is Friday’s performance by the Turkish Lira, which after days of strengthening to pare some of its capitulation-led losses from 7 days ago, it is back trading around the 6.00 mark, which is an exchange rate that is set to constitute a major pain for the economy given its major exposure on foreign-denominated debt. For now, the defiant standoff by Turkish President Erdogan to receive any type of financial assistance from the IMF or the refusal by the Turkish Central Bank of resorting to orthodox tactics such as raising rates to stem the unstoppable rise in inflation is paving the way for Turkey to remain a major beacon of uncertainty with potential contagion effects into the Euro.

Emerging markets a source of concern that won’t go away short term

And to the Euro we’ve come. While the brakes were pressed for the deepening trade impasse between China and the US to receive the benefit of the doubts, the single currency has nonetheless suffered the consequences of Turkey making headlines in recent weeks, which for the currency has had a double-whammy effect. Firstly, the mismanagement of the Turkish crisis so far, with the immediate implications that this may have towards a few European banks, has had market forces ruminating that the ECB may turn more cautious on growth and hence in the inflation outlook at a time when they attempt a tricky transition from an era of expansionary QE-led monetary policies into a tentative period (a late 2019 story) of tightening. Secondly, the overwhelming ruling of risk aversion in August has seen the appeal towards the USD increase, causing the DXY to materialize a significant technical breakout, further fueling the bearish EUR/USD trend. The recovery in prices we are seeing is set to encounter major roadblocks on an approach of 1.15/1.16.

The Sterling, meanwhile, continues to communicate major risks of a downward extension unless Brexit negotiations exhibit meaningful progress towards a scenario other than a ‘no-deal’, which is by and large one of the key driving forces keeping the selling pressure so persistent. Even on a pick up of risk flows which saw the long-awaited USD liquidation late last week, the GBP has barely been able to muster any gains, which more often than not, is a great leading hint of a market with signs of trend continuation written all over. The data from the UK last week (upbeat UK retail sales + neutral CPI/jobs) won’t move the needle for the current ‘wait and see’ mode by the BoE in the slightest, with the bank in a ‘once a year rate hike’ comfort zone.

A currency that is set up to be a major contender to challenge the rises in safe havens is the Canadian Dollar, emboldened by positive domestic data, which reinforces the notion of hawkish outlook by the BoC. The latest evidence came after a blockbuster inflation reading on Friday, printing 3% y/y in July! The currency, however, is still being threatened by the possible prospects of a no deal in the NAFTA trade talks with the US, which is a risk event that until more clarity in a satisfactory resolution is seen – no much progress so far – should limit the potential upside in the CAD that would otherwise enjoy if the risk was to be removed.