Although the calendar suggested a relatively quiet start of the week, that was not the case. Overnight, the RBNZ and the FOMC cut interest rates aggressively, by 75bps and 100bps respectively, while the BoJ doubled the pace of its ETF purchases. As for the rest of the week, we have two more central banks deciding on interest rates, the Norges Bank and the SNB, and it would be interesting to see how these two Banks will respond to the coronavirus outbreak. Australia’s employment report and Canada’s CPIs are also due to be released.

Monday appeared to be a relatively light day in terms of data releases. However, it was not as quiet as the calendar suggested. Overnight, three major central banks decided to ease their policy further, outside scheduled meetings, in an attempt to safeguard the global economy from the negative effects of the fast spreading coronavirus. The chorus started with the RBNZ, which cut its benchmark rate by 75bps to +0.25%. The FOMC was next with an even bolder action. US policymakers decided to reduce the Federal funds rate target by 100bps, to 0-0.25%, while later in the Asian session, the BoJ, although it did not cut rates, pledged to double the pace of its ETF purchases.

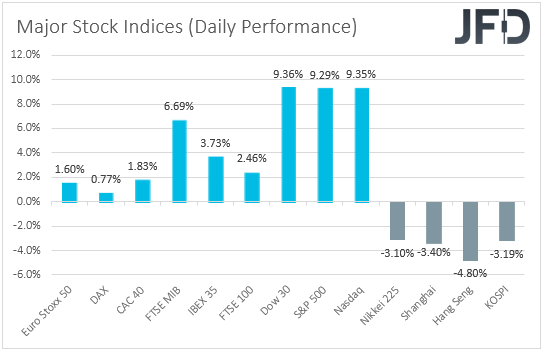

However, the decisions had only limited success in calming panicked investors. Following Friday’s rebound in equity markets, Asian bourses traded in the red today as investors’ anxiety over the effectiveness of such measures deepened even further. Japan’s Nikkei 225 closed 3.10% down, while China’s Shanghai Composite slid 3.40%.

All these developments suggest that investors may now be on the same page as we have been for the last few days. We have been repeatedly noting that rate cuts may not be enough to offset the damage. With fears that the virus is unlikely to be contained soon, we see it hard for consumers and businesses to opt for cheap loans and start spending. Thus, we believe that the worst is not behind us yet, and that the economic wounds could deepen and drag well into Q2. We repeat once again that with elevated uncertainty on how much more serious all this could get, it would be naïve to assume that everything is priced in. Therefore, we would treat any gains in equities as corrective moves, before the next leg south. We believe that there is still room for declines in risk assets as investors my once again seek shelter in safe havens.

Data out of China may have also weighed on the broader market sentiment as the large declines in fixed asset investment, industrial production and retail sales for February underscore the magnitude of the economic damage the virus’s outbreak has already caused to the world’s second largest economy.

As for the rest of today’s data, the only release worth mentioning is the New York Empire State manufacturing index for March, which is forecast to have fallen to 4.40 from 12.90.

On Tuesday, we have the UK employment data for January. The unemployment rate is expected to have remained unchanged at +3.8%, while average weekly earnings including bonuses are forecast to have accelerated to +3.0% yoy from +2.9%. The excluding bonuses rate is anticipated to have remained unchanged at +3.2%. We don’t believe that this set of data will prove so determinant with regards to the BoE’s future course of action as they refer to a period before the fast spreading of the coronavirus around the globe.

On Wednesday, the BoE decided to cut interest rates by 50bps, outside a scheduled gathering, while the UK Chancellor of the Exchequer Rishi Sunak announced that the nation will borrow almost GBP 100bn more in coming years than predicted a few months ago. In our view, the large fiscal loosening lessens the need for the BoE to proceed for more rate cuts, and with other major central banks, like the RBA and the BoC, expected to continue easing, this may allow the pound to strengthen.

From Germany, we get the ZEW survey for March. The current conditions index is expected to have slid further into the negative territory, to -30.0 from -15.7. This would mark the 8th straight month with a negative sign. The economic sentiment index is also expected to tumble into negative waters, to -29.0 from 8.7. With the coronavirus spreading in the EU at a fast pace, a slump in those indices appears more than normal to us. From the Eurozone as a whole, we get the Labor cost index and wages for Q4. The Labor cost index is forecast to have accelerated to +3.0% yoy from +2.6% in Q3, while no forecast is currently available for the wages rate.

In the US, we have retail sales, industrial and manufacturing production data, all for February. Both headline and core sales are expected to have slowed to +0.2% mom from +0.3%, while the industrial and manufacturing production rates are forecast to have returned into positive territory. Namely, the IP rate is expected to have risen to +0.4% mom from -0.3%, while the MP one is forecast to have increased to +0.3% mom from -0.1%. The JOLTs Job Openings for January are also coming out and the forecast points to a small decline.

On Wednesday, under normal circumstances lights would have fallen on the FOMC policy decision. However, as we already noted, the Fed decided to act outside a scheduled meeting, slashing interest rates by 100 bps overnight, to a target range of 0% to 0.25%, and promising to expand its balance sheet by at least USD 700bn in the coming weeks. On March 3rd, the Committee decided to cut the federal funds rate by 50bps, the first emergency move outside a scheduled meeting since the 2008 financial crisis, in an attempt to safeguard the world’s largest economy from the impact of the coronavirus. On top of that, on Thursday, officials decided to offer USD 1.5 trillion in short-term loans, and that they will start purchasing a broader range of US Treasuries, which means a new round of QE. The latest and much bolder cut make us believe that the Fed is done cutting rates, as US officials are not in favor of negative rates. Even Chair Powell noted following the 100bps cut that he does not think negative rates in the US are appropriate, and that the Committee will not proceed with this week’s scheduled meeting.

As for Wednesday’s data, during the early Asian morning, New Zealand’s current account balance for Q4 is coming out and the forecast points to a narrowing deficit. Japan’s trade data are also due to be released with the nation’s deficit expected to have turned into surplus.

During the European day, we get Eurozone’s final CPIs for February and as it is always the case, they are expected to confirm their preliminary estimates, namely that the headline rate slid to +1.2% yoy from +1.4%, while the core rate ticked up to +1.2% yoy from +1.1%.

From the US, we get building permits and housing starts for February, with the forecasts suggesting small declines, while from Canada, we have the CPIs for February. The headline CPI is anticipated to have slowed to +2.1% yoy from +2.4%, while no forecast is available for the core rate, which stood at +1.8% yoy in January. Under normal circumstances, this would have allowed BoC policymakers to stay away from the cut button, but bearing in mind that central banks are now acting to support the wounded global economy that is hit by the effects of the coronavirus outbreak, we cannot rule out another bold action by the BoC, perhaps outside a scheduled meeting as well.

On Thursday, during the Asian morning, it was the turn of the BoJ to decide on monetary policy, but this Bank proceeded with a decision early Monday as well. Japanese officials maintained the short-term policy rate at -0.10% and the target of the 10-year JGB yields at around 0%. With little ammunition in terms of rate cuts, the Bank just proceeded by increasing its annual pace of ETF purchases to JPY 12 trillion from JPY 6 trillion previously.

As for our view, we see it very hard for business sentiment to rebound just because the BoJ pledged to purchase more ETFs. Compared with the cuts we got from other central banks, this is a much softer move and may not have the desired effects. We expect the yen to continue attracting haven flows, as we don’t believe that equities have hit a bottom yet. With the virus still spreading fast and with no vaccine on the horizon, uncertainty over whether it could indeed be contained may weigh further on investors’ morale, prompting them to reduce even further their risk exposure.

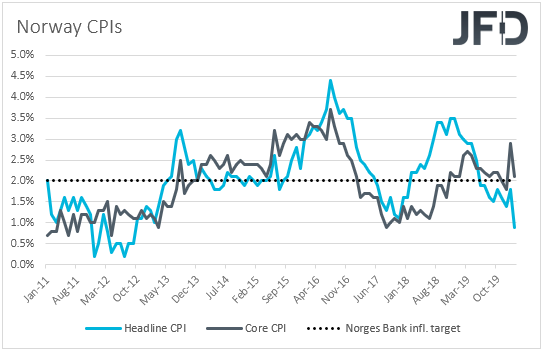

Later in the day, during the European session, the central bank torch will be passed to the Norges Bank and the SNB. When they last met, Norwegian policymakers kept interest rates untouched at +1.50% and noted that the policy rate will remain at the present level in the coming period. However, last week inflation data disappointed largely, with the headline rate tumbling to +0.9% yoy from +1.8%, and the core one sliding to +2.1% yoy from +2.9%.

With central banks worldwide easing their respective policies in order to prevent a global recession due to the effects of the coronavirus, a slump in Norwegian inflation may come as an extra reason for policymakers to follow the footsteps of the RBA, the FOMC, the BoC, the BoE and the RBNZ, especially after the sharp tumble in oil prices last Monday.

Passing the ball to the SNB, this may be the only central bank which is unlikely to ease this week. Having the lowest interest rate globally, at -0.75, the Bank may prefer to fight the virus crisis by intervening in the FX market in order to prevent the franc from keep strengthening, especially with the currency attracting haven flows recently. Another reason we don’t expect the SNB to touch interest rates is because the ECB refrained from doing so. The Bank may just adopt a more dovish language and strengthen its intervention signals.

As for Thursday’s data, during the Asian morning, Japan releases its National CPIs for February. No forecast is available for the headline rate, while the core one is anticipated to have held steady at +0.8%. That said, with both the Tokyo CPI rates for the month sliding, we believe that the National rates will follow suit.

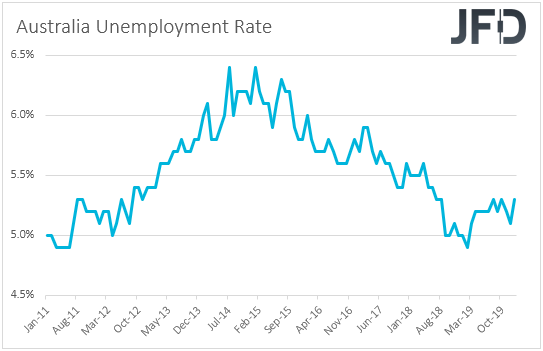

From Australia, we get the employment report for February. The unemployment rate is expected to have stayed unchanged at 5.3%, well above the 4.5% threshold which the RBA believes it will start generating inflationary pressures, while the employment change is forecast to show that the economy has gained less jobs than it did in January. Specifically, it is expected to reveal 10k new jobs, down from the 13.5k print in January.

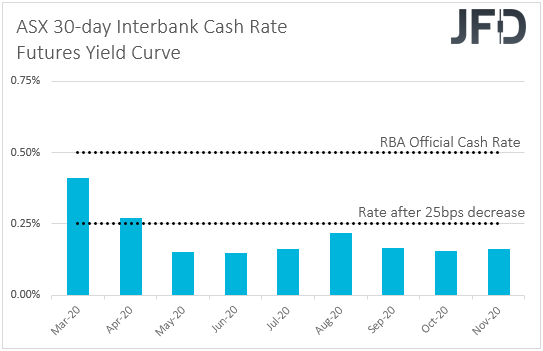

At their latest meeting, RBA officials decided to cut interest rates by 25bps, to a new record low of 0.5%, with Governor Philip Lowe saying in the post-meeting statement that the coronavirus was having a “significant” impact on the domestic economy and that it’s hard to assess how large the effects will be. In the statement, it was also repeated that officials “remain prepared to ease monetary policy further to support the Australian economy”. According to the ASX 30-day interbank cash rate futures yield curve, there is an 92% chance for officials to push the cut button again at the April meeting, and a soft employment report may just seal the deal.

New Zealand’s GDP for Q4 is also due to be released. The forecast is for the qoq rate to have declined to +0.5% from +0.7%, but this will drive the yoy one up to +2.4% from 2.3%. With all other major central banks easing their policy in order to safeguard the global economy from the coronavirus crisis, the RBNZ was no exception, kickstarting the overnight easing chorus with an emergency 75bps rate reduction, noting that the economic outlook has “deteriorated significantly”. Officials also added that the rate will stay at 0.25% at least for 12 months, meaning that there are no more cuts on the horizon. That said, they agreed that should further stimulus be required, a large-scale asset purchase program would be preferable. With all that in mind, we don’t believe that data referring to a period before the virus outbreak would alter that view and thus, they may not prove the market mover they usually are. We prefer to wait for data concerning the first quarter of 2020, as these numbers may prove determinant over to whether the RBNZ will proceed with QE.

As for the rest of the day, the only release worth mentioning is the US Philly Fed manufacturing index, which is expected to have declined to 10.0 from 36.7.

Finally, on Friday, Japanese markets will be closed due to the Vernal Equinox holiday.

From Canada, we get retail sales for January, while in the US, we have the existing home sales for February. Canada’s headline sales are expected to have risen 0.4% mom, after stagnating in December, while the core rate is expected to have declined to +0.2% mom from +0.5%. The US existing home sales are forecast to have rebounded 0.8% mom after sliding 1.3% in January.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Weekly Outlook: RBNZ, Fed, BoJ Ease Policy, Norges Bank And SNB Also Meet

Published 03/16/2020, 05:44 AM

Updated 07/09/2023, 06:31 AM

Weekly Outlook: RBNZ, Fed, BoJ Ease Policy, Norges Bank And SNB Also Meet

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.