- Investors looking to US NFPs for confirmation of their Fed rate cut bets

- RBA could still signal that higher rates are possible

- But BoC may confirm that interest rates have peaked in Canada

- Japan’s Tokyo CPIs and employment numbers to impact BoJ speculation Will the US jobs report change the dollar’s fate?

The US dollar has been suffering lately on increasing bets that the Fed will cut rates massively next year. The latest strong hit came from Fed Governor Waller earlier this week, who said that if the decline in inflation continues for several more months, they could start lowering the policy rate. This was the first time a Fed official, and particularly a hawkish one, discussed the possibility of a cut and that’s why market participants added to their rate cut bets, with a 25bps cut now being fully priced in for May and the total number of basis points of rate cuts expected for next year increased from 90 to around 115.

As they try to incorporate every new information into their forecasts, next week, investors are likely to turn their attention back to economic data as Fed officials enter the usual pre-meeting blackout period, and thus, there will be no more speeches. On Tuesday, the ISM non-manufacturing PMI for November and the JOLTS job openings for October are coming out, while on Wednesday, the ADP report for November may be scrutinized ahead of the highlight of the week, the official employment report for November.

The report is expected to show that the unemployment rate held steady at 3.9% and that nonfarm payrolls increased by 175k in November from 150k in October. Currently, there is no forecast for average hourly earnings. A 3.9% jobless rate and a slight acceleration in the nonfarm payrolls are unlikely to shake much market expectations with regards to several rate reductions by the Fed next year. For that to happen, these numbers may need to be accompanied by a reacceleration in wages.

This could spark some fear that inflation could pick up steam in the months to come, thereby prompting the Fed to keep interest rates high for a longer period than currently anticipated. On the other hand, a further slowdown in wages could solidify investors’ belief and push the dollar lower. After all, lately, market moves suggest that investors are selling the dollar more aggressively when data or headlines corroborate their view, than buying it when there are indications supporting the opposing ‘higher for longer’ case.

Aussie awaits RBA decision, Australia’s GDP and Chinese data

At its November meeting, the RBA raised interest rates, citing more persistent inflationary pressures. Nonetheless, in the accompanying statement, there was an element of uncertainty about whether another rate hike may be needed. This resulted in a drop in the Aussie, as heading into the meeting there was confidence that another quarter-point hike may be in the works for the turn of the year.

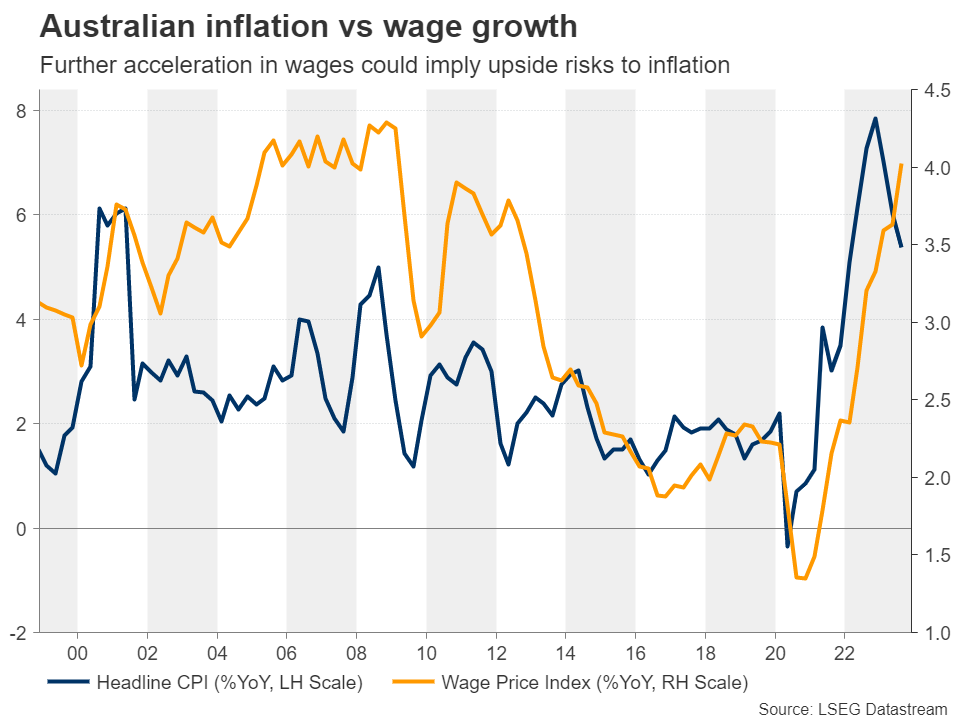

That said, with the new Governor, Michele Bullock sounding hawkish thereafter, and the minutes of that meeting revealing concerns about high inflation, investors kept some rate hike bets on the table. Even after the monthly y/y CPI rate for October dropped by more than expected on Wednesday, investors continue to assign a decent 40% probability for another hike by March.

Perhaps that’s because the closely watched trimmed mean CPI only ticked down to 5.3% y/y from 5.4%, which is still well above the upper bound of the RBA’s 2-3% objective and/or because the monthly CPI data does not show all the components included in the quarterly CPI. In other words, the quarterly reading is a more reliable inflation metric. The q/q CPI rate for Q4 will be available on January 31. What’s more, the Wage Price Index for Q3 rose to 4.0% from 3.6%, which implies upside risks to inflation in the months to come.

With all that in mind, the RBA is more likely to stand pat on Tuesday, but it is unlikely to clearly signal that this hiking cycle is over. Officials are likely to maintain the view that interest rates could further rise if needed, which could allow the aussie to extend its recovery against the US dollar.

That said, the aussie may not be driven only by the RBA decision next week, as on Wednesday, Australia’s GDP for Q3 is scheduled to be released. The forecast is for a slowdown to 0.3% q/q from 0.4%, which could reignite some speculation that the RBA is done raising rates, even if just the previous day policymakers signal readiness to do more. On Thursday, Australia’s and China’s trade numbers will be released, while on Saturday, China publishes its CPI and PPI data. Given the close trade ties between Australia and China, more signs that the world’s second-largest economy is bottoming out could allow the aussie to continue marching north.

Will the BoC signal the end of this tightening crusade?

There is another central bank decision on next week’s agenda: The Bank of Canada on Wednesday. When they last met, policymakers of this Bank held interest rates steady, citing moderating spending and relieving price pressures. However, they remained prepared to raise the policy rate further if needed.

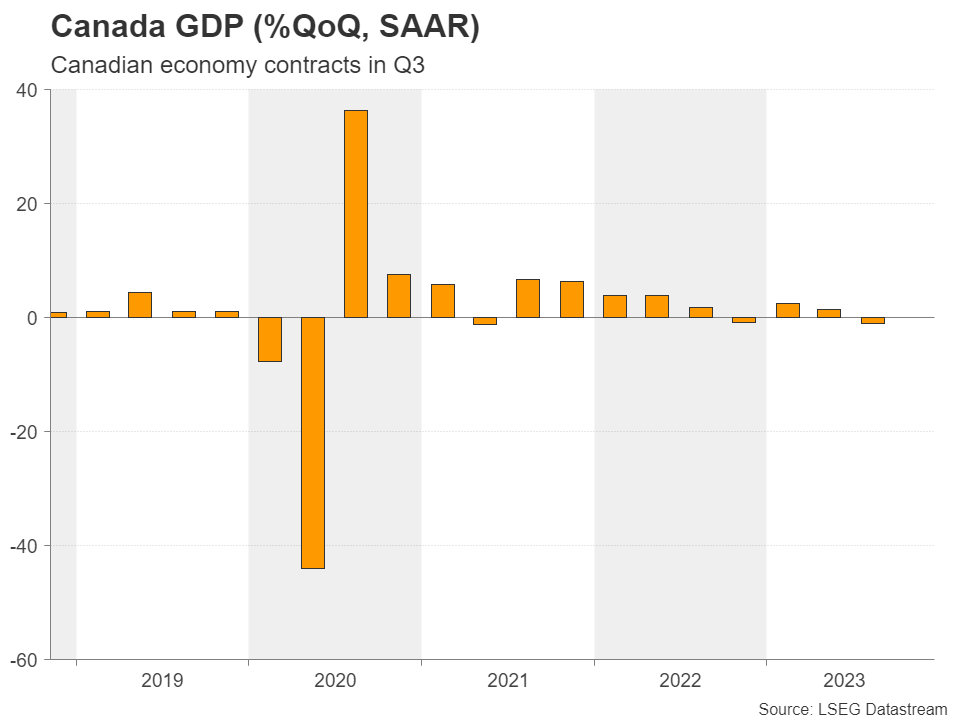

Since then, data have been coming out on the soft side with the unemployment rate rising to 5.7% from 5.5% in October, the employment change revealing that the economy added less jobs than forecast during the month, and inflation cooling more than expected. This combined with Thursday’s GDP data for Q3 pointing to a contracting economy has led investors to price in around 105bps worth of rate cuts by the end of 2024.

Although officials are unlikely to confirm the market’s view of so many bps worth of cuts, they could signal that they are done raising interest rates, which could hurt the loonie. Just last week, BoC Governor Macklem said that interest rates may be at their peak, given that excess demand has vanished, and weak growth is expected to persist for months.

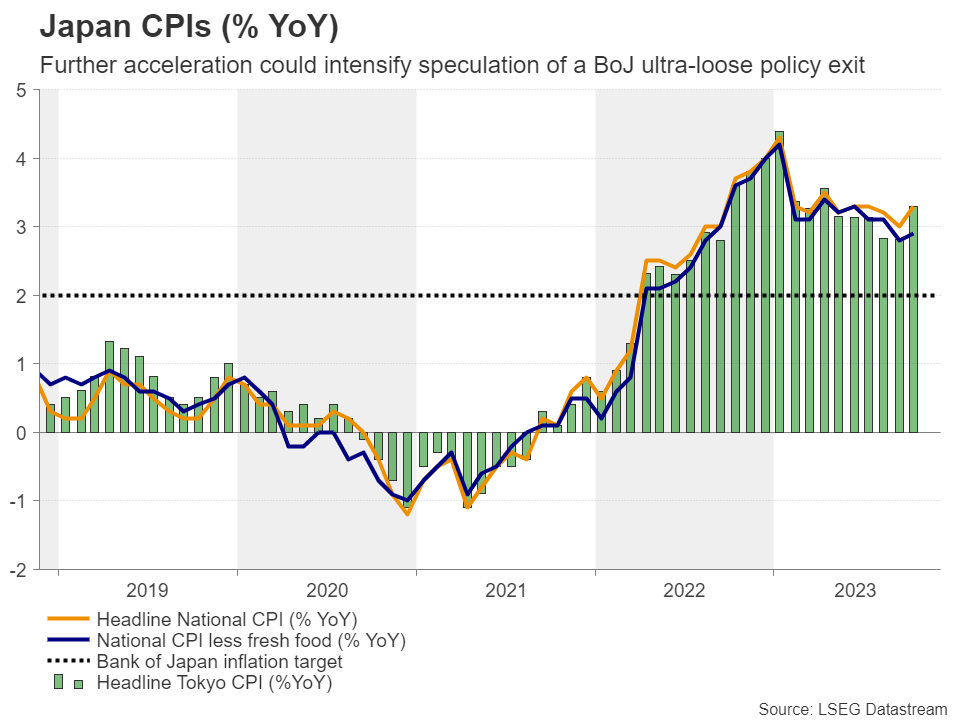

Japanese data could fuel speculation about a BoJ policy exit soon

It will be an interesting week for yen traders as well, as during the Asian session Tuesday, Japan’s Tokyo CPI figures are due to be released, while on Thursday, the final estimate of Q3 GDP and the employment report are coming out. The final estimate of GDP is forecast to confirm that the economy shrank 0.5% in Q3, but if the Tokyo CPIs, which are closely correlated with the National numbers, point to further acceleration in inflation, and the jobs data reveal another pick up in wages, then speculation that the BoJ could exit ultra-loose monetary policy conditions soon is likely to intensify, thereby adding more fuel to the yen’s engines.