Stock market gains continued at a heady pace this quarter, marking the fifth consecutive quarter of gains for Canadian and U.S share prices, and when the ink dried on the tape on June 30th, the result was a dead heat—to the second decimal place—with both the S&P/TSX Composite and the S&P 500 earning a total return of 8.55% during the quarter.

Ongoing strength in the Canadian dollar sapped some of the advance in U.S. stocks however, such that in Canadian dollar terms, the S&P 500 returned a still very respectable 7.1%. In the bond market, the FTSE Canada Overall Short-Term Bond Index generated 0.5% in interest income which was all but fully offset by declining prices for a total return of 0.1% this quarter. Preferred shares, as measured by the Solactive Laddered Canadian Preferred Share Index continued to perform well generating a total return of 5.7%.

With the strength of the stock market recovery since last March (+81% for Canadian stocks and +96% for U.S. stocks), many investors, pundits and media types have turned their attention to worrying about when the next inevitable CRASH is destined to occur. We would like to nip that speculation in the bud, and the best way to do so is to refer back to commentary (excerpted for brevity and shown below in italics) that we wrote five quarters ago, as markets were bottoming.

“…markets have quite correctly priced in a brutal and nasty global recession… that will see unemployment skyrocket to levels not seen since the Great Depression, an unprecedented deluge of corporate and personal bankruptcies and a multi-month sustained period of “life as (un) usual”

“This is neither a cyclical recession, brought about by unduly tight monetary policy or inventory de-stocking nor is it a structural recession brought about by imbalances and financial bubbles. This is an event driven recession, brought about by the social contract between citizens, business and government and the difficult decisions that have been made to put the economy into something akin to a medically induced coma…”

“The question then necessarily turns not to “whether” our economies will survive, but rather how soon and how steep will be the recovery…”

“The severity of a recession is measured by its depth, duration and diffusion. This recession is virtually certain to be deeper than any in modern records. The diffusion of it is likely to be wider spread than virtually any other…but we have some confidence that it is unlikely to be a long recession...”

“A plausible, although far from assured scenario would see social distancing rules relaxed once health authorities are confident the virus spread has been contained. From there, growth in the hardest hit sectors, for instance in bars and restaurants would be astronomical in percentage terms...”

“The multiplier effect that would result from all these furloughed workers returning to work…would be large as lower income workers generally spend nearly 100% of their incomes. A second wave of economic acceleration could take hold as pent-up demand for goods and services…is unleashed. From there, a general improvement in consumer and business confidence could take root as safety and security (both physical and economic) concerns are slowly laid to rest, paving the way for hiring and business investment decisions to be made.”

“…the big picture point is that an otherwise healthy ‘patient’ can be revived from a medically induced coma and in the medium-term return to his or her normal daily life without lasting damage from the extended timeout.”

This trip down memory lane to a time most of us are eager to forget about is important, because it keeps us honest and helps us to avoid the all-too-common practice of backward narration (i.e., “it was obvious that March 24, 2020 was the buying opportunity of a lifetime”, “it was obvious in 1999 that Amazon (NASDAQ:AMZN) was destined to be a dot.com survivor and grow into the world’s biggest retailer”, etc.).

In retrospect, much of what we had foreseen has now come to pass and has been reflected in stock prices today. Where we erred was in our expectation that a tsunami of corporate and personal bankruptcies would occur. Massive and widespread government relief payments to households and businesses de facto socialized the majority of private sector losses that we had expected, and which would otherwise have occurred, and this in part helps to explain the faster and stronger than expected recoveries in stock markets.

Looking ahead, we certainly will not pretend to know what might trigger another event driven recession, but we can think critically about what might prompt a more garden-variety cyclical or structural recession, and we simply don’t see the warning signs for either of these today, and accordingly can’t in good faith get on the ‘pending crash’ bandwagon, knowing as we do that economic cycles typically last 6-8 years, or more.

Cyclical recessions, as noted above, are most commonly caused by sharp interest rate hikes or inventory de-stocking, neither of which strike us as being imminent. The Federal Reserve has signalled loudly and clearly that they are in no hurry to raise interest rates from the current extraordinarily low levels, as has the Bank of Canada.

Both central banks have acknowledged that current inflation is running above their targets, which under more normal circumstances would prompt rate hikes. But despite current multi-year high inflation rates of 3.6% in Canada and 5% in the U.S., central bankers are quite forthright in acknowledging that their playbook for combatting sustained above target inflation is better developed and road tested than their playbook for combatting the alternative—deflation, and we agree.

Both central banks have also thoughtfully and convincingly painted a picture of inflation which is transient, rather than entrenched, as base effects of low prices a year ago influence current inflation rates, as supply chain problems and the lingering spectre of COVID-19 in commodity producing regions spur commodity supply shortages and finally as unusual labour force mix effects come into play in the all-important wage inflation statistics.

A consensus of 17 professional economists predicts a cumulative increase in Canadian overnight interest rates of just 0.25% between now and the end of 2022, with none of those polled expecting more than a 0.5% increase. In the United States, a consensus of 64 professional economists predicts a mere 0.1% increase in overnight rates between now and the end of 2022, which in fact is below the functional increment of 0.25% that the Federal Reserve uses in setting overnight rates. In interest rate derivative markets—where real dollars are at stake as opposed to just professional reputations—current prices imply one quarter point rate hike in Canada over the next two years and less than one quarter point rate hike in the United States.

So, all tolled, experts and investors expect interest rates to remain below 1% for the next 18 months or more, which in the long historical context would remain extraordinarily low and, in our view, benign to markets given that the 25-year average overnight rate in Canada is 2.25%. As for inventory excesses, which oftentimes prompt firms to reduce production and employment levels to trim surplus inventories, these also seem completely at odds with the current circumstances.

The latest Institute for Supply Management survey of U.S. manufacturers showed an inventory to sales ratio of 1.25x – 6% below its long-term average and within a hair’s breadth of its lowest reading in at least 20 years and needless to say, stories of supply chain problems, commodity scarcities, tight shipping capacity and even labour shortages are rampant these days. Warehouses are clearly too empty, not too full.

Structural recessions are brought on by economic imbalances and financial bubbles. Economic imbalances are usually evidenced by overinvestment in one or more areas of the economy, as in the case of the Canadian oil sands 10-15 years ago, U.S. residential housing 15 years ago and technology and telecom equipment globally 20-25 years ago.

We’re hard pressed to pinpoint any one major area of the “real” economy where money is gushing in freely, funding dubious investments and overbuilding capacity today. We cannot entirely rule out the possibility that cheap money is blowing financial bubbles, but our assessment is that these bubbles, if anything, are limited to narrow niches like SPACs, cryptocurrencies and other speculative assets, as we discussed last quarter, such that if they were to pop, they would be unlikely to have far reaching systemic or economic consequences.

Housing affordability in Canada remains an area of yellow alert concern as well, as we also noted last quarter, but considering its importance to household and banking system balance sheets, we expect regulators and government officials will tread thoughtfully and lightly here in attempting to reign in market forces.

So, what we are left with is the conclusion that economic growth and share price gains will continue, absent an exogenous shock that triggers another event driven recession. Certainly, markets will move upwards in a sawtooth pattern, as they usually do, with advances, followed by corrections, followed by further advances.

Moreover, the pace of gains is almost certain to moderate, with stocks having correctly priced in the rapid snapback recovery in corporate profitability already, such that further gains are more likely to be driven by earnings growth than by valuation multiples expanding. Recognizing this, we have made some changes to portfolios over the last quarter, including the purchases of SNC Lavalin (TSX:SNC) in Canadian portfolios and Amazon (NASDAQ:AMZN) in U.S. accounts, both companies where we have high conviction in their ability to meaningfully grow earnings.

SNC Lavalin, in particular, exemplifies all three elements of growth, value and cyclicality. Growth by virtue of its exposure to infrastructure contracts globally and here in North America where there has been structural underinvestment for many years and where governments are now earmarking dollars for renewal, cyclicality by virtue of its clients (projects) being capital intensive and in many cases exposed to natural resource sectors, and value by virtue of it undergoing significant transformation and repositioning under an entirely new leadership team.

For some years Amazon has been the quintessential growth company, just too rich in valuation for our liking. But a sideways trading pattern over the past year coupled with an acceleration of e-commerce trends have brought Amazon’s valuations into attractive levels given the high conviction we have around their growth rates. As we have experienced with Facebook (NASDAQ:FB) and Alphabet (NASDAQ:GOOGL), company fundamentals are far less concerning than valuation, so we are pleased with our entry point.

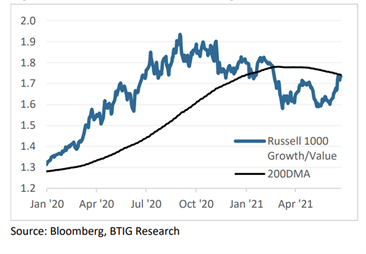

As we often say, we are pragmatic rather than dogmatic investors, and so while we still see ample opportunity for value stocks to outpace growth stocks in the quarters and years ahead, our approach is primarily “bottom-up”, or stated differently, is driven by detailed, company-specific research, and so our portfolios typically will and currently do incorporate both growth and value stocks. The market at large remains engaged in an ongoing daily tug-of-war between these two factions of stocks (as shown in the chart below), but we believe we have chosen well within both groups and thus don’t necessarily need to make bold all-in or all-out bets on either group.

This is neither a time to be greedy, nor a time to be fearful. Markets are approaching a mid-cycle, steady state growth phase that we expect will play out over the next several years.