Rumors flew over the weekend that AT&T (T) had made an offer to buy Spain’s Telefonica (TEF) for $93 billion -- a roughly 50% premium to today’s market cap.

Telefonica was quick to dispel the rumor and AT&T had no comment as Monday afternoon.

My gut reaction is that this rumor is exactly that: a rumor. The sheer size of the deal makes it unlikely that it would ever make it past the assorted national telecom regulators without provoking anti-trust hysteria. AT&T is the largest telecom firm in North America, and Telefonica is a dominant player in Europe and Latin America.

But while I don’t see a deal happening, the prospect does raise a few questions. Given that mobile phones are ubiquitous in the United States, smartphones are not far from the saturation point, fixed-line telecom is in terminal decline and broadband internet and paid TV are well past the saturation point, where does a behemoth like AT&T go for growth?

One obvious answer is emerging markets, which is why Telefonica was allegedly on AT&T radar screen. Telefonica gets roughly half its revenues from Latin America, where fast internet and smartphone subscriptions are both still growth businesses.

The problem is that there aren’t a lot of assets there left to buy. The Latin American market is essentially a two-horse race between Telefonica and America Movil (AMX), the company controlled by Mexican billionaire Carlos Slim.

AT&T actually already owns 9% of America Movil, making it the company’s second-largest shareholder. This would also make it complicated for AT&T to make a serious offer for America Movil’s bitterest rival.

There aren’t a lot of easy targets elsewhere either. The European telecom giants tend to dominate in their countries’ former colonial holdings, with Telefonica being a prime example. France Telecom (FTE) is active in 21 Middle Eastern and African countries, and Britain’s Vodafone (VOD) has most of the rest of the world covered. Vodafone operates in 30 countries, many of which are attractive emerging markets, and has partnerships in place with local providers in over 50 more.

So, an American newcomer like AT&T would be competing on price against some entrenched competition for a capital-intensive business that doesn’t have particularly great margins. Perhaps an aggressive emerging markets growth strategy is not so attractive after all…

I raised a few eyebrows earlier this year when I said that my favorite 'tobacco stock' was semiconductor giant Intel (INTC).

By “tobacco stock” I was referring to companies in slow-growth industries that had high barriers to entry. Because their growth prospects are limited, they tend to use their excess cash flows to buy back their own shares and pay out monster dividends.

This is where AT&T, Verizon (VZ) and Sprint (S) are today. Barriers to entry are not as high in mobile telecom as they are in, say, tobacco or semiconductors. Consider the recent success of discount providers like Metro PCS (PCS), which recently merged with T Mobile. But given the limited spectrum available and the cost of building out a network, the current providers have little to worry about in the way of new entrants.

Sprint is a train wreck right now, which is thankfully being bought out by the Japanese telco Softbank (SFTBY) -- a company so desperate for growth in its moribund Japanese home market that even a dog like Sprint looks attractive).

But how do AT&T and Verizon look?

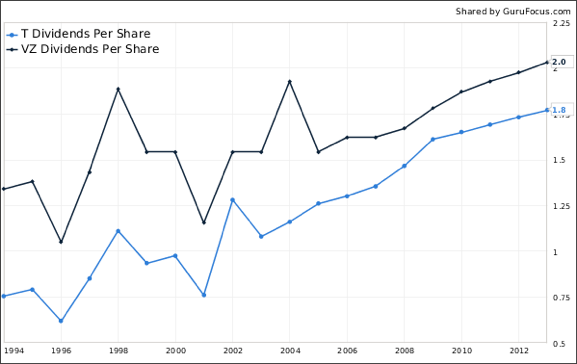

AT&T yields 5% in dividend and is aggressively buying back its shares. Verizon yields 4% and has not made any recent announcements regarding share repurchases.

5% and 4%, respectively, are not bad yields in this environment. This puts the two major telecom companies about on par with triple-net REITs and MLPs.

But if I have to choose between telecom stocks and REITs and MLPs, I’m taking the REITs and MLPs. Both should benefit from an improvement in the economy, as a healthier economy means rising rents and increased energy usage. Both are also better positioned to weather any uptick in inflation.

AT&T and Verizon might also benefit from an improving economy, as more employment means more business phone and data lines and, to some extent, upselling to more expensive personal plans. But both operated in an inherently cutthroat and deflationary business. Quality real estate appreciates in value over time. Telecommunication equipment does not.

Bottom line: in a diversified income portfolio, there might be room for the likes of AT&T or Verizon. But I would give a higher allocation to quality REITs and MLPs.

Sizemore Capital is long TEF. This article first appeared on InvestorPlace.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Telecoms: Great Dividends, But...

Published 06/18/2013, 11:19 AM

Updated 07/09/2023, 06:31 AM

Telecoms: Great Dividends, But...

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.