Oracle stock jumps 5% on TikTok deal progress, OpenAI fundraise talks

Believe it or not, Broadcom (NASDAQ:AVGO) is looking to buy Qualcomm (NASDAQ:QCOM) , at least according to people familiar with the matter. But if the rumors are right, the company could pay $70-$80 a share in cash and stock, valuing the company at over a $100 billion, the largest semiconductor deal ever. It’s possible that regulators will not approve the deal on competitive considerations, but just in case they don’t, there’s much going for both the companies-

Rationale for the Deal

There are a number of reasons why the deal makes sense.

First, Qualcomm is one of the largest semiconductor companies, as is Broadcom, so their combination will create a semiconductor giant like Intel (NASDAQ:INTC) or Samsung (KS:005930) with greater resources to tap emerging opportunities.

Second, being the leading supplier of modem chips having also made some progress in 5G, Qualcomm brings Broadcom important technology to round out its portfolio. Not only that – there is very little product overlap despite the fact that both target the market for mobile devices. Smartphone growth rates have been coming down recently because of increased penetration, but other markets like IoT, self-driving cars, artificial intelligence and cloud computing continue to emerge. A combined company with much greater product breadth, a larger client roster and scope for greater integration of technology should do better in this landscape.

Third, Qualcomm has a large number of standard essential patents that it licenses on the basis of fair, reasonable and non-discriminatory (FRAND) terms. It also has several other patents that do not form part of standards but that it bundles with standard essential patents. So on the one hand, Qualcomm shouldn’t have to license all patents at standard essential rates, while on the other, it needs to offer greater clarity on the amount it’s charging for the non-standard technology that forms part of the bundle. It also needs to allow companies to build or second source their own non-standard technology.

The practice has drawn ire from a number of foreign governments and now, Apple (NASDAQ:AAPL) and its suppliers have ganged up against it. What’s worse, Apple is roping in others like Samsung, so Qualcomm’s legal problems are mounting. Apple phones use Qualcomm technology, but Apple and its suppliers have also stopped paying Qualcomm on this pretext while second sourcing from Intel.

This has of course been a big blow to Qualcomm’s revenue and profits. The acquisition has the potential to bring another big semiconductor player on Qualcomm’s side. It can also lead to a resolution of the conflict.

Fourth, Broadcom management has a lot of experience with acquisitions, which have been the most consistent pillar of growth for the company. The biggest of these was the Avago-Broadcom merger, which retained the Broadcom name post closure. Before that, it made more than 50 smaller acquisitions over the course of a decade. Management is also known for cost control, so the combined entity may see greater fiscal discipline, which could be a good way to extract profits.

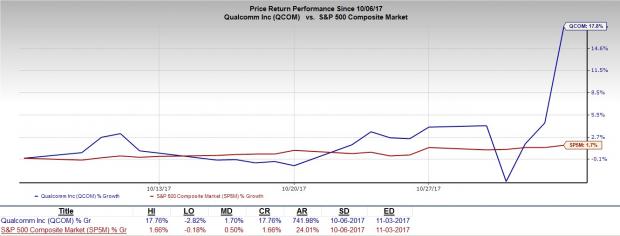

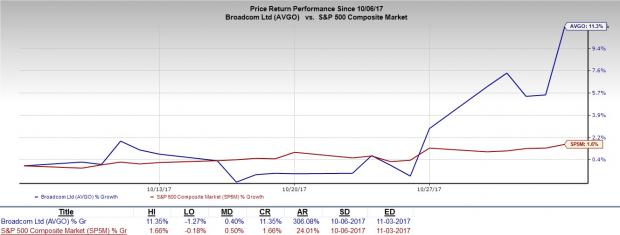

Fifth, the chances of prolonged litigation have pressured Qualcomm’s share prices, so the deal will be a good return on investment for shareholders.

Possible Deal Breakers

Both Qualcomm and Broadcom are in the middle of other acquisitions. Qualcomm is looking to buy NXP, the shareholders of which are asking for a higher price. Broadcom is trying to acquire Brocade (NASDAQ:BRCD) (a much smaller deal). There could be many glitches along the way.

The second concern is regulatory. Qualcomm is quite a dominant player in its own field and Broadcom further expands that field. In a way, since they aren’t competitors, there may not be anti-competitive concerns. But on the other hand, the two together will be a mobile chip making powerhouse, which may be something regulators will consider.

Last Words

These may be some of the biggest acquisitions we have talked about, but consolidation in the space will likely continue in the foreseeable future because chip development and verification isn’t getting any cheaper. Also, companies generally compete on their ability to deliver energy efficient chips that are also more powerful, fast and durable while being cheap. This naturally benefits larger players that can invest heavily in R&D and then manufacture on scale.

On the other hand, some of the biggest propositions have been shot down by regulators, such as Applied Materials’ attempt to buy Tokyo Electron, or more recently, Lam Research’s (NASDAQ:LRCX) attempt to buy KLA-Tencor (NASDAQ:KLAC) .

Broadcom has apparently been trying to acquire Qualcomm for some time, but its previous attempts weren’t attractive to Qualcomm management. Given its current problems, the company may be more willing to go for it.

Broadcom has a Zacks Rank #4 (Sell) while Qualcomm has a Zacks Rank #3 (Hold). For better investments in technology today, you can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Wall Street’s Next Amazon (NASDAQ:AMZN)

Zacks EVP Kevin Matras believes this familiar stock has only just begun its climb to become one of the greatest investments of all time. It’s a once-in-a-generation opportunity to invest in pure genius.

Brocade Communications Systems, Inc. (BRCD): Free Stock Analysis Report

QUALCOMM Incorporated (QCOM): Free Stock Analysis Report

Apple Inc. (AAPL): Free Stock Analysis Report

Broadcom Limited (AVGO): Free Stock Analysis Report

KLA-Tencor Corporation (KLAC): Free Stock Analysis Report

Lam Research Corporation (LRCX): Free Stock Analysis Report

Original post

Zacks Investment Research