Major EU and US indices continued marching north yesterday, perhaps on news suggesting that Europe will begin vaccinations earlier than previously anticipated, and on reports that US negotiators are getting closer in passing a covid-aid bill. However, sentiment softened heading into the Asian session today, on headlines that US lawmakers are struggling to agree on the bill’s details, and following remarks by UK PM Johnson that a no-deal Brexit is still very possible.

Equities Retreat in Asia, GBP Slides on PM Johnson's Remarks

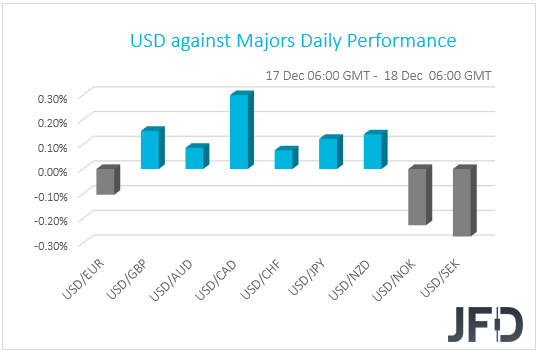

The dollar traded higher against the majority of the other G10 currencies on Thursday and during the Asian session Friday. It underperformed only versus SEK, NOK, and EUR in that order, while it gained the most ground against CAD, GBP and NZD.

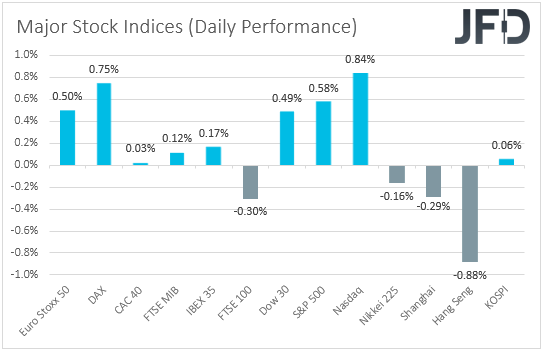

The relative strength of the US dollar, combined with the weakening of the commodity-linked Loonie and Kiwi, suggests that markets turned risk off at some point. Indeed, turning our gaze to the equity world, we see that, although the majority of EU and US indices traded in positive waters, most Asian indices were in the red today. Japan’s Nikkei 225, China’s Shanghai Composite and Hong Kong’s Hang Seng slid 0.16%, 0.29% and 0.88% respectively.

Thursday was marked by increasing risk appetite as some European nations said that they were set to begin vaccinating their citizens with the Pfizer-BioNTech drug in the last week of December, instead of the beginning of the new year as was earlier expected. The vaccine is expected to be approved by the European Medicines Agency during that week.

On top of that, headlines suggested that, in the US, top Republicans and Democrats got closer in agreeing on a new coronavirus-aid bill, with the unexpected rise in initial jobless claims making the case even more imminent. That said, risk appetite softened heading into the Asian session today, perhaps on reports that negotiators in the US were struggling to agree on the details of a USD 900bn coronavirus-aid package. Comments from UK PM Boris Johnson that no trade accord would be reached unless the EU changes its position substantially, may have also hurt sentiment.

Despite the softening of investors’ optimism during the Asian session today, we stick to our guns that the path of least resistance for equities is to the upside. Lawmakers from both major US political parties said that failing to agree on a covid-relief package is not an option, while Republican Senate Majority Leader Mitch McConnell said that talks could spill into the weekend.

In our view, this suggests that a bill is more likely than not to pass before the end of the year. On the Brexit front, Irish Deputy PM Leo Varadkar said that he remains optimistic that the EU and the UK would secure a trade deal in the coming days, keeping hopes on that front on the table. Taking also into account that the vaccinations in Europe are likely to start earlier than previously anticipated, we see the case for equities and other risk-linked assets to rebound soon, while safe havens are likely to come under renewed selling interest.

In the FX world, the British pound was among the main losers, coming under selling interest following the pessimistic remarks by UK PM Boris Johnson. However, as we already noted, we think that there are still hopes for a trade agreement before year end, hopes that may allow the British currency to rebound again. More headlines that the two sides are getting closer into sealing a deal are likely to benefit the pound, even against the Aussie and Kiwi, which we expect to perform well in a risk-on environment. For the pound to drift lower, we may need to get more headlines suggesting that a no-deal Brexit is the most likely outcome.

Yesterday, we also had the SNB and BoE monetary policy decisions, while today, in Asia, we had the BoJ. Kicking off with the SNB, the Bank kept its policy unchanged, reiterating that the Swiss franc remains highly valued and that they remain willing to intervene more strongly in the FX market. The BoE stood pat as well, noting that Q4 GDP is likely to be a little weaker than expected in November and repeating that it stands ready to increase its QE purchases pace should market functioning worsens. The BoJ also announced no changes to its major settings, but extended its funding support program to firms that was introduced earlier this year in response to the coronavirus pandemic. Other than that, there was no other significant change. In terms of market reaction, all three decisions passed largely unnoticed by the financial world.

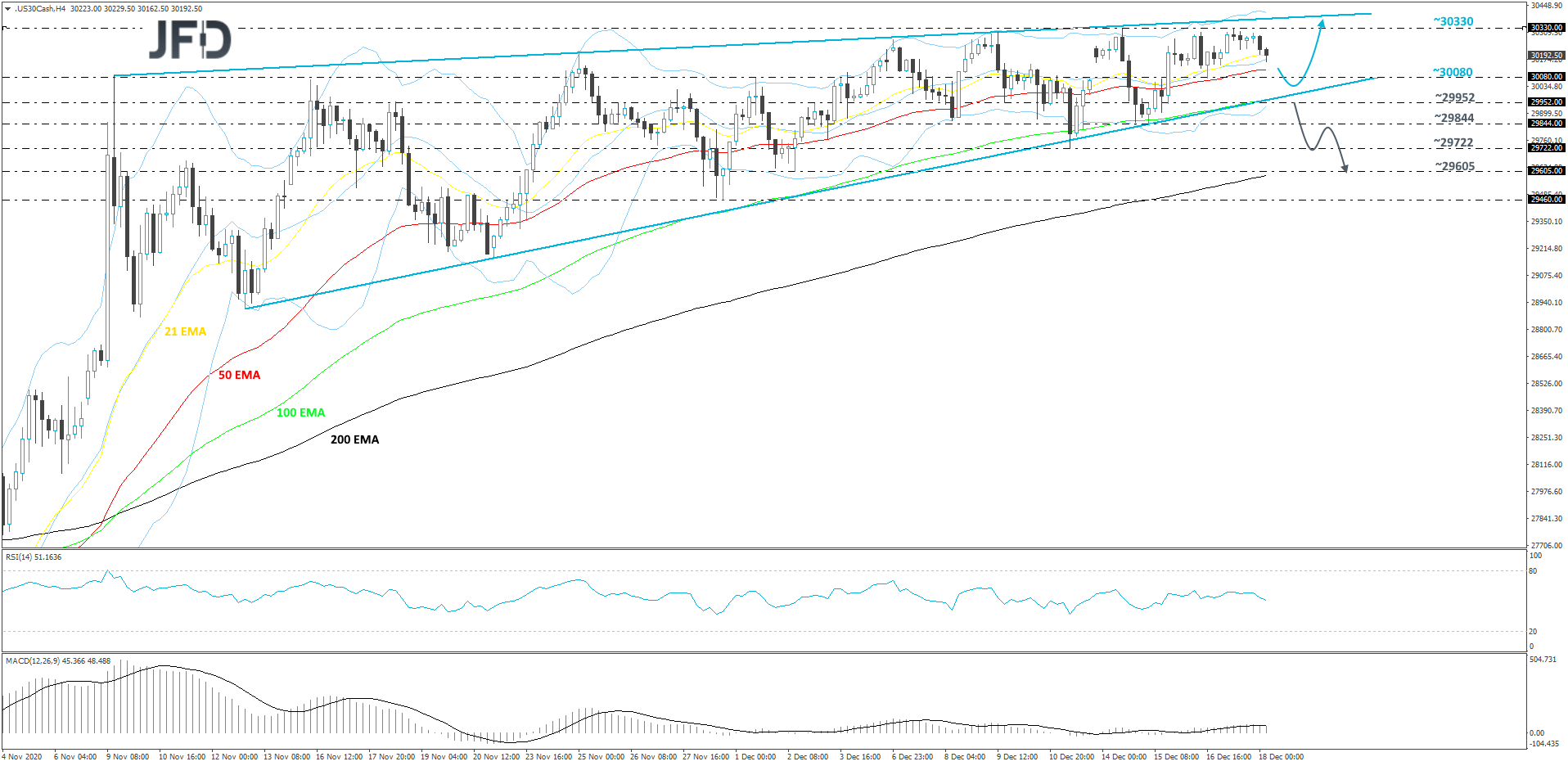

DJIA Technical Outlook

The Dow Jones Industrial Average index continues to trade within a rising wedge pattern, which tends to be a bearish pattern. However, as long as the price trades inside that formation, we cannot talk about any longer-term downside moves. There is a chance to a small correction lower, but if the lower side of the pattern remains intact, we will stay positive with the overall outlook.

A small decline could bring the index a bit lower, where it might test the 30080 territory, or the lower side of the aforementioned rising wedge. If that whole area acts as a good support zone, the buyers may step in again and drive DJIA higher. If so, the price might drift back to the current all-time high on our cash index, at 30330, which if breaks, would place DJIA into the uncharted area. The next target could be the upper side of the aforementioned wedge.

On the downside, if the lower side of the previously-discussed pattern breaks and the index falls through the 29952 hurdle, marked by the low of Dec. 15, that might signal a possible reversal. More sellers could join in if DJIA drops below the 29844 zone, marked by the low of Dec. 15. The price could then get pushed to the 29722 obstacle, a break of which may set the stage for a move to the 29605 level. That level marks the current lowest point of December.

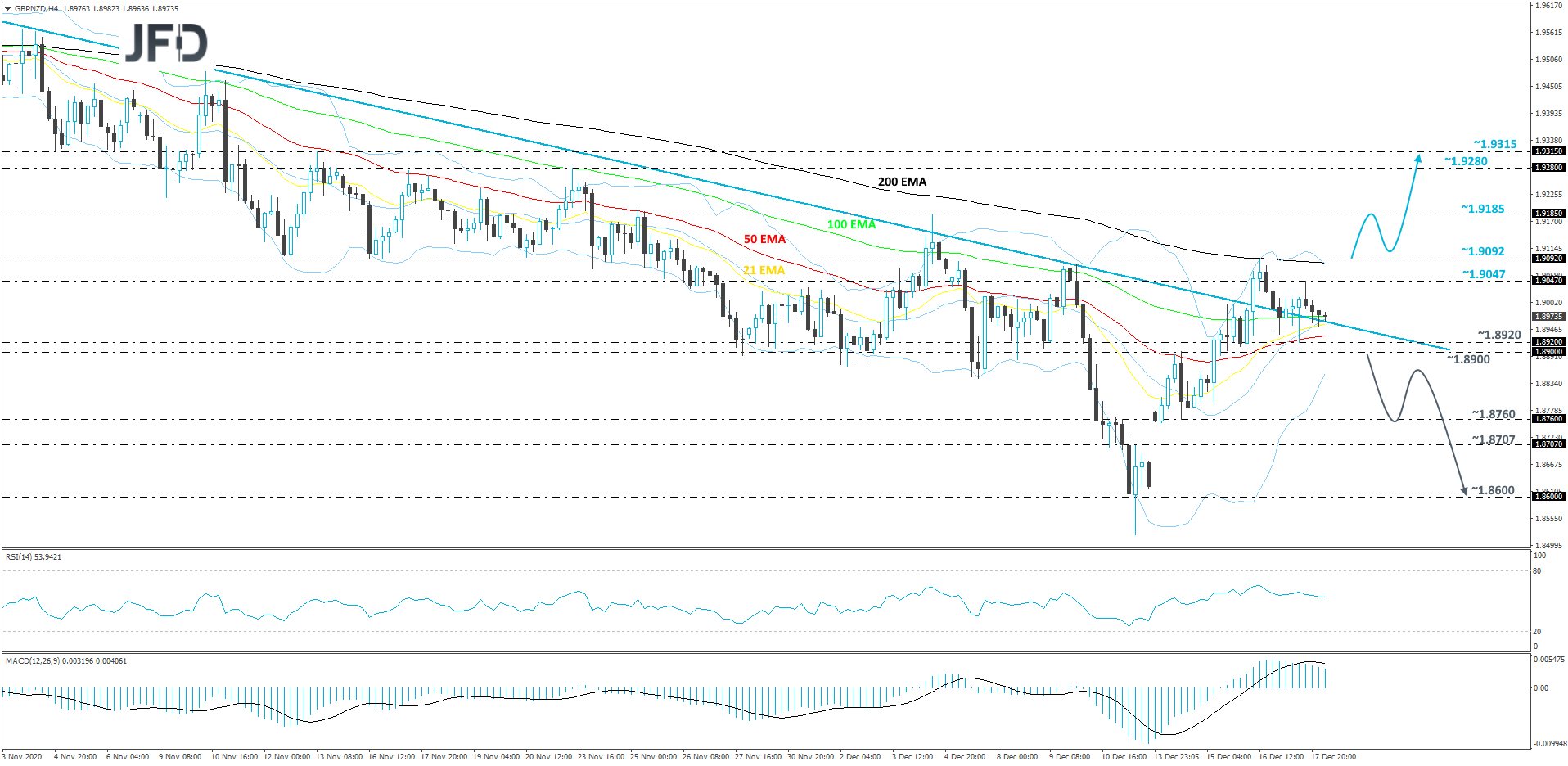

GBP/NZD Technical Outlook

After breaking the short-term downwards-moving trendline for the third time, but this time managing to remain above it, GBP/NZD went ahead and tested the 200 EMA on our 4-hour chart. The pair failed to make its way above it and corrected slightly lower, but continued to balance above the aforementioned downside line. If the rate continues doing that, at some point, we could see a push back up again. That said, in order to get a bit more comfortable with higher areas, we would prefer to wait for a push above 1.9092 barrier, marked by the current highest point of this week. Until then, we will remain somewhat positive with the near-term outlook.

If, eventually, we do see a strong move above that 1.9092 barrier, this will also place the pair above the 200 EMA on the 4-hour, which could be seen as a positive and attract more buying interest. GBP/NZD might then travel to the 1.9185 hurdle, marked by the current highest point of December, where it may temporarily get halted. However, if the buyers are still feeling a bit more comfortable than the sellers, a break of that hurdle could send the rate to the 1.9280 zone, or the 1.9315 level, marked by the highs of Nov. 23 and 13 respectively.

Alternatively, a break back below the aforementioned downside line and a rate-drop below the 1.8900 area, marked by the high of Dec. 14 and an intraday swing low of Dec. 15, may spook new buyers from entering at that moment. GBP/NZD could slide to the 1.8760 hurdle, marked by the low of Dec. 14, which might provide a temporary hold-up. That said, if the bears continue to dominate the field, that may result in a further decline, where GBP/NZD might travel to the 1.8707 obstacle, or to the 1.8600 level, marked by an intraday swing low of Dec. 11.

As For Today's Events

During the early European session, we already got the UK retail sales for November, with both the headline and core sales falling by less than anticipated.

The German Ifo survey for December is also due to be released. The current assessment index is expected to have declined to 89.0 from 90.0, while the business expectations one is forecast to have risen to 92.5 from 91.5. This is likely to take the business climate index slightly lower, to 90.0 from 90.7.

Later in the day, we get more retail sales data, this time from Canada and for the month of October. Both the headline and core rates are expected to have declined to +0.2% mom, from +1.1% and +1.0% respectively.

We also have three speakers on today’s agenda: ECB Supervisory Board Chief Andrea Enria, Chicago Fed President Charles Evans, and Fed Board Governor Lael Brainard.