Equities and other risk-linked assets fell, while safe havens rallied, as accelerating coronavirus cases in Europe prompted some countries to proceed with renewed lockdown measures, and raised concerns that more nations around the globe could follow suit soon.

During tonight's Asian session, the RBNZ announces its monetary policy decision. Although we don’t expect any action, we will scan the statement for hints as to whether officials are willing to introduce more stimulus in the months to come if deemed necessary.

Dollar Rallies, Equities Slide As Rising COVID Cases Spark Lockdown Concerns

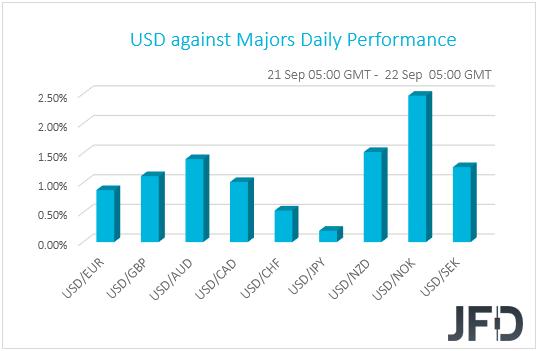

The US dollar traded higher against all the other G10 currencies on Monday and during the Asian morning Tuesday. It gained the most versus NOK, NZD, AUD, and SEK in that order, while it eked out the least gains versus JPY.

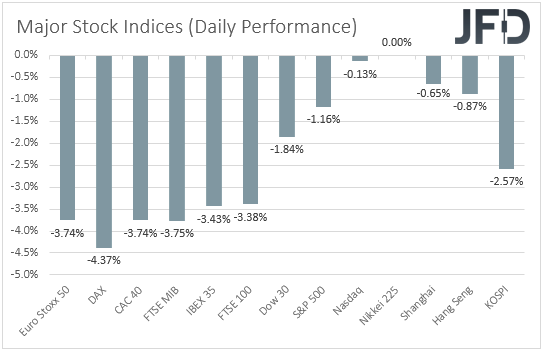

The strengthening of the US dollar and the yen suggests that the financial community traded in a risk-off fashion. Indeed, turning our gaze to the equity world, we see that major EU and US indices were a sea of red, with the negative investor morale rolling into the Asian session today.

Japanese markets were closed due to the Autumn Equinox holiday, while China’s Shanghai Composite, Hong Kong’s Hang Seng, and South Korea’s KOSPI are currently down 0.65%, 0.87%, and 2.57% respectively.

The catalyst behind the deterioration in risk sentiment at the start of the week was the accelerating COVID-19 infections in Europe, which prompted some nations to proceed with renewed lockdown measures. Among those nations are Denmark, Greece, and Spain, with Britain also considering a second round of restrictions as new cases rise by at least 6k per day.

Adding to concerns was the death of the US Supreme Court of Justice and liberal icon Ruth Bader Ginsburg, which decreases the chances of Congress passing a new coronavirus-aid bill to support the US economic recovery. Congress has for weeks remained deadlocked over the size and shape of such a package, with the chances of a breakthrough before the November 3rd election diminishing day by day.

In contrast to last week’s downturn, the slide in the beginning of this week was led by value stocks, such as industrials, energy, and financials, as opposed to technology stocks. That appears logical to us as tech firms may be the least affected in case of a second round of lockdown measures around the globe. This is evident by the fact that Zoom (NASDAQ:ZM) was among the main gainers on the NASDAQ 100, on the prospect that new restrictions may spur more use of the product. Airline, hotel, and cruise companies also fell, with Europe’s travel and leisure index marking its worst two-day drop since April.

Up until last week, we had been holding the view that the slide in equities and risk-linked assets may stay limited and short-lived, due to the extra loose monetary policy around the globe, as well as due to the positive headlines surrounding a potential coronavirus vaccine. However, the acceleration in coronavirus cases and, consequently, the fresh fears over a second lockdown, which could hamper the economic recovery, suggest that there is still ample room for further declines.

Thus, we would now switch our view, and we would see decent chances for the current retreat to continue for a while more. Among currency pairs, those which could pull back the most are those consisting of a risk-linked currency and a safe haven, the likes of AUD/USD, NZD/USD, AUD/JPY, and NZD/JPY.

Will the RBNZ Expand Its Stimulus Efforts?

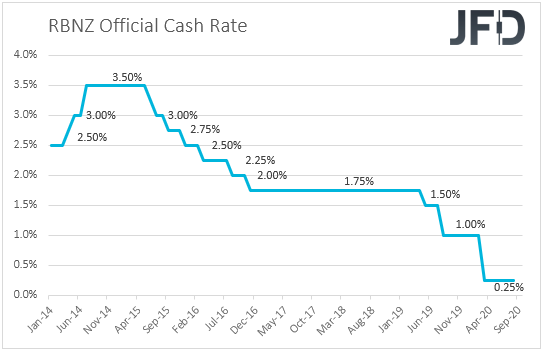

Speaking about the Kiwi, tonight during the Asian morning Wednesday, the RBNZ will announce its monetary policy decision. At its latest gathering, the Bank decided to keep its Official Cash Rate (OCR) unchanged at 0.25%, but expanded its Large-Scale Asset Purchase (LSAP) program, adding that a package of additional monetary instruments must remain in active preparation, including a negative OCR and purchases of foreign assets.

Since then, the only top tier economic data we received was New Zealand’s GDP for Q2, the qoq rate of which slid to -12.2% from -1.4%. That said, although a 12.2% qoq contraction is a severe one, it is still better than the Bank’s own forecast of -14.3% qoq.

Therefore, combined with the fact that the Bank has expanded its stimulus efforts just at the prior gathering, this is likely to keep officials’ fingers off the easing button at this gathering. They may prefer to wait for more data before they reach at safe conclusions as to whether more stimulus is needed or not. That said, we will dig into the statement for clues as to how likely such a move may be in the foreseeable future.

Any hints that officials could push the easing button without hesitation in the months to come may bring the Kiwi under additional selling interest. For the currency to rebound, the Bank may have to signal that although further stimulus remains possible, it is not warranted at the moment, a scenario we see as the least likely, especially with the coronavirus still spreading at a fast pace around the globe.

Technical Outlook AUD/USD

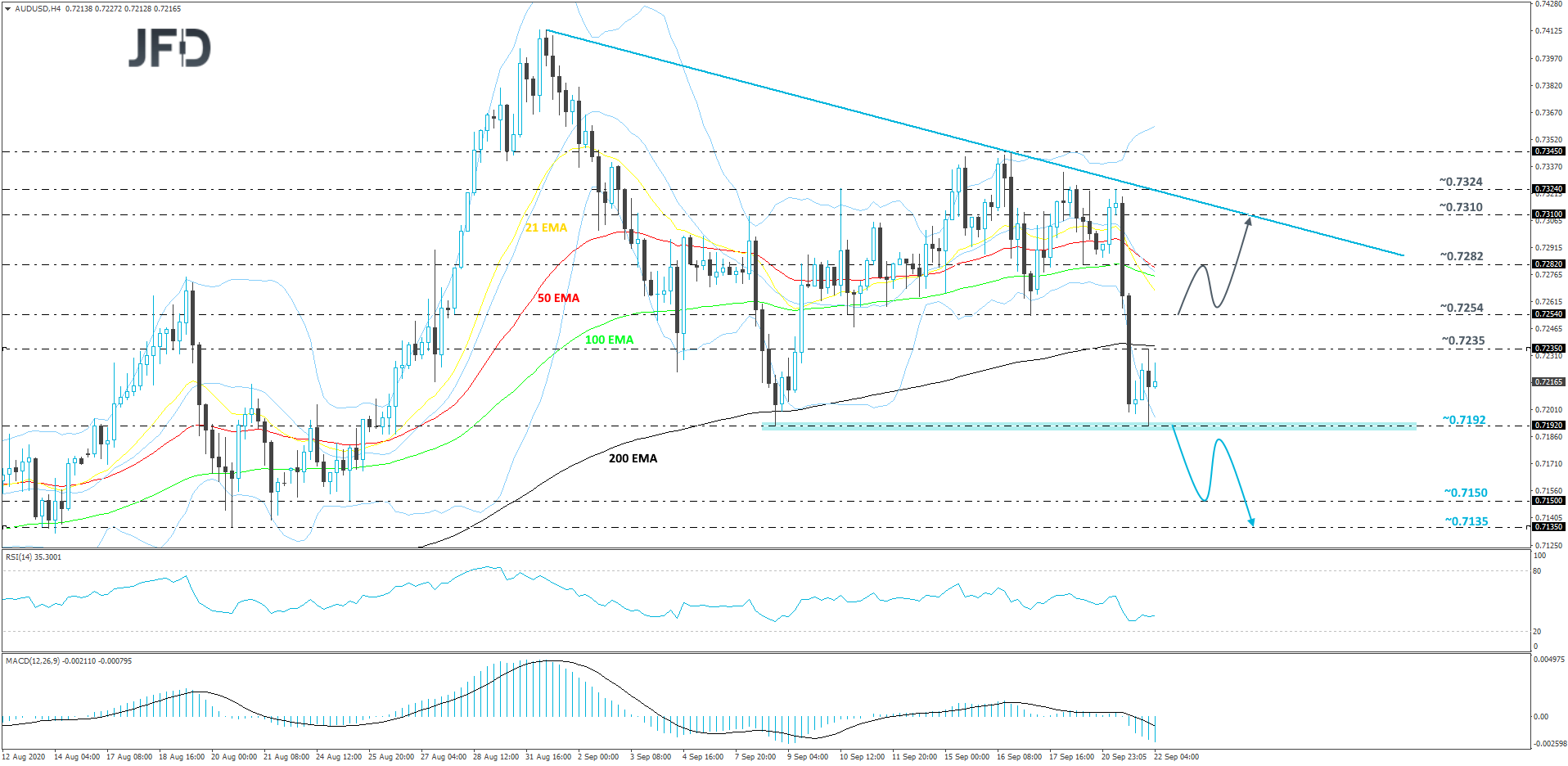

Yesterday, AUD/USD sold off heavily, moving further away from its short-term tentative downside resistance line taken from the high of September 1st. That said, the pair got a good hold-up near its key support zone, at 0.7192, which marks the current lowest point of September. At the same time, the rate is now trading below the 200 EMA on our 4-hour chart, what some could also see a bearish indication. In order to get a bit more comfortable with further declines, a drop below the 0.7192 hurdle would be needed.

If, eventually, the pair does fall below the 0.7192 area, that would confirm a forthcoming lower low, potentially inviting more sellers into the game. AUD/USD could then drift to the 0.7150 obstacle, a break of which might open the way for a test of the 0.7135 level. That level marks the lows of August 13th and 20th.

On the other hand, if the bears are not ready to bring AUD/USD lower yet and the rate climbs back above the 0.7254 barrier, marked by the low of September 17th, that may invite a few more buyers into the game. They might help lift the pair to the 0.7282 obstacle, which if fails to provide resistance and breaks, may open the door for a test of the aforementioned downside line, or the 0.7310 level. That level marks an intraday swing low formed yesterday.

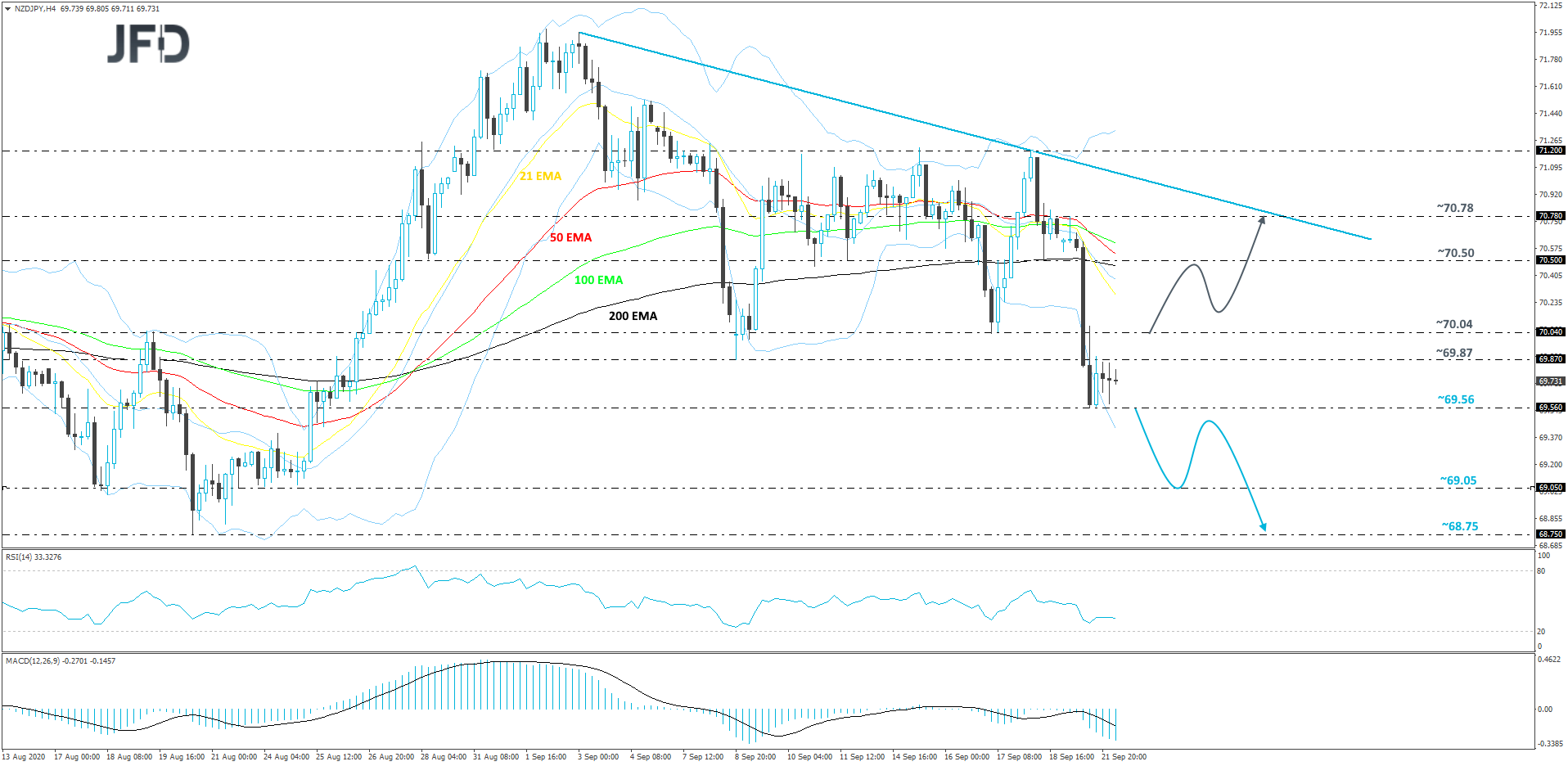

Technical Outlook NZD/JPY

NZD/JPY dropped sharply yesterday, breaking below some of its key support areas and creating a new low for September. The rate got a hold-up near the 69.56 territory, from which it rebounded somewhat. For now, it seems that the pair might continue with its journey a bit further south, as our oscillators are indicating negative price momentum. In addition to that, NZD/JPY continues to trade well below its short-term tentative downside resistance line taken from the high of September 3rd. For now, we will take a bearish approach and aim for slightly lower areas.

A drop below yesterday’s low, at 69.56, would confirm a forthcoming lower low and could increase the pair’s chances of drifting further south. AUD/USD might then travel to the 69.05 zone, marked near the lows of August 24th and 25th, which may stall the rate temporarily. The pair could even rebound somewhat, however, if it fails to move back above the 69.56 area, this might result in another slide. If this time the 69.05 hurdle fails to hold, the next possible support level to consider could be at 68.75, which is the lowest point of August.

Alternatively, if the rate rebounds and jumps over the 70.04 barrier, marked by the low of September 17th, that might temporarily spook the bears from the field and allow the bulls to take control. NZD/JPY may rise to the 70.50 hurdle, marked by an inside swing low of September 18th, which is near the 200 EMA on our 4-hour chart. The rate could stall there for a bit, but if the buying is still strong, a further move north may send the pair to the 70.78 level, marked by yesterday’s high. Around there NZD/JPY might also test the aforementioned downside line taken from the high of September 3rd.

As For Today's Events

Ahead of the RBNZ decision, during the European morning today, we have another central back deciding on monetary policy and this is the Riksbank. At its latest gathering, this Bank decided to extend its framework for its asset purchases from SEK 300bn to SEK 500bn, up to the end of June 2021, while it announced that in September, it will start purchasing corporate bonds. The Board also decided to cut interest rates and extend maturities on lending to banks, despite keeping the repo rate unchanged at 0.0%.

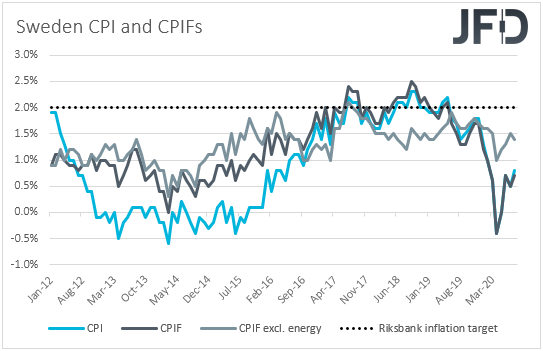

Latest inflation data showed that both the CPI and CPIF rates increased, even though by less than anticipated, but the core CPIF metric, which excludes the volatile items of energy, has slowed to +1.4% yoy from +1.5%. In any case, we believe that after acting at the previous gathering, a tick down in the core CPIF rate is unlikely to urge Riksbank policymakers to proceed with any policy changes at this meeting.

Later in the day, the US existing home sales for August are coming out and the forecast points to a slowdown to +2.4% mom from +24.7%. The API (American Petroleum Institute) weekly report on crude oil inventories is also coming out, but as it is always the case, no forecast is available.

We also have five speakers on today’s agenda: Fed Chair Jerome Powell, BoE Governor Andrew Bailey, ECB Chief Economist Philip Lane, ECB Executive Board member Fabio Panetta, and Chicago Fed President Charles Evans.