What happens to a global economy after 10+ years of global central bank efforts to support a recovery attempt after a massive credit/debt collapse originates from a prior credit/debt housing bubble? What happens to global economies when they become addicted to easy money policies and central bank activities that support greater and greater risk-taking? What is the end result of these actions after more than 10+ years of excess and central bank support for the markets?

Let's play this out a bit to think about how the current market environment may be similar to what happened in the mid/late 1990s and see if we can come to any real conclusions. Remember, we are using our research and technical analysis skills to play a “what if” scenario in this research article. Our current trading systems have not warned us of any major bearish price trends of price collapses that may take place. Our systems are still trading the U.S. markets based on current market trends. This research is completely speculative in the sense that we are trying to identify “what if” scenarios based on events in the recent past.

One thing that our research team has been discussing over the past 8+ months, since shortly after the U.S. elections in November 2020, is the idea that the new President/US Federal Reserve may engage in policies that are initially perceived as supportive of the global markets in a post-COVID world – yet may engage in very dangerous end results. An example of this is the continued stimulus efforts for a world that has somewhat moved beyond the initial COVID shock and has transitioned into a new form of economic activity. Another example would be the Fed continuing to act in a manner to support the equities market while inflation and consumer activity have recently shown extreme pricing/buying activities.

One idea that my research team suggested is this activity may be similar to President Ronald Reagan's Star-Wars project in how Reagan was able to prompt a spending excess between the U.S. and Russia, which eventually broke the Russian economy. The process between that event and what is happening right now are strangely similar.

The Strange Outcome Of Global Central Bank Policies: The U.S. Is The Clear Winner

The U.S. and many foreign central banks have pushed the envelope of easy money policies over the past 8+ years by continuing to run programs to support a stronger economic outcome. The focus has been on creating an inflationary target to start a more traditional shift away from the ongoing easy money policies. Inadvertently, these global central banks may have created and supported one of the biggest asset shifts/bubbles in the past 50+ years.

The COVID-19 virus event may have actually pushed the U.S. Federal Reserve and foreign global central banks into an inadvertent process of creating a massive inflation trap at a time when the global economy and corporate world was banking on much more mild inflationary trends. The reflation trade that came after June 2020 is likely to have pushed assets, commodities, credit and debt cycles beyond any conceivable scope of reason, while putting unimaginable pressure on foreign central banks in Asia, South America, Africa and most of the emerging markets. The incredible rally in commodities, asset values (homes, stocks, U.S. equities and others) prompted capital to shift towards the strongest and most capable outcomes on the planet. This created a liquidity trap in many foreign markets where traders moved assets into U.S. equities, cryptos, U.S. ETFs and other assets, while shunning less dynamic and secure global assets.

(Source: https://data.worldbank.org/indicator/CM.MKT.LCAP.CD)

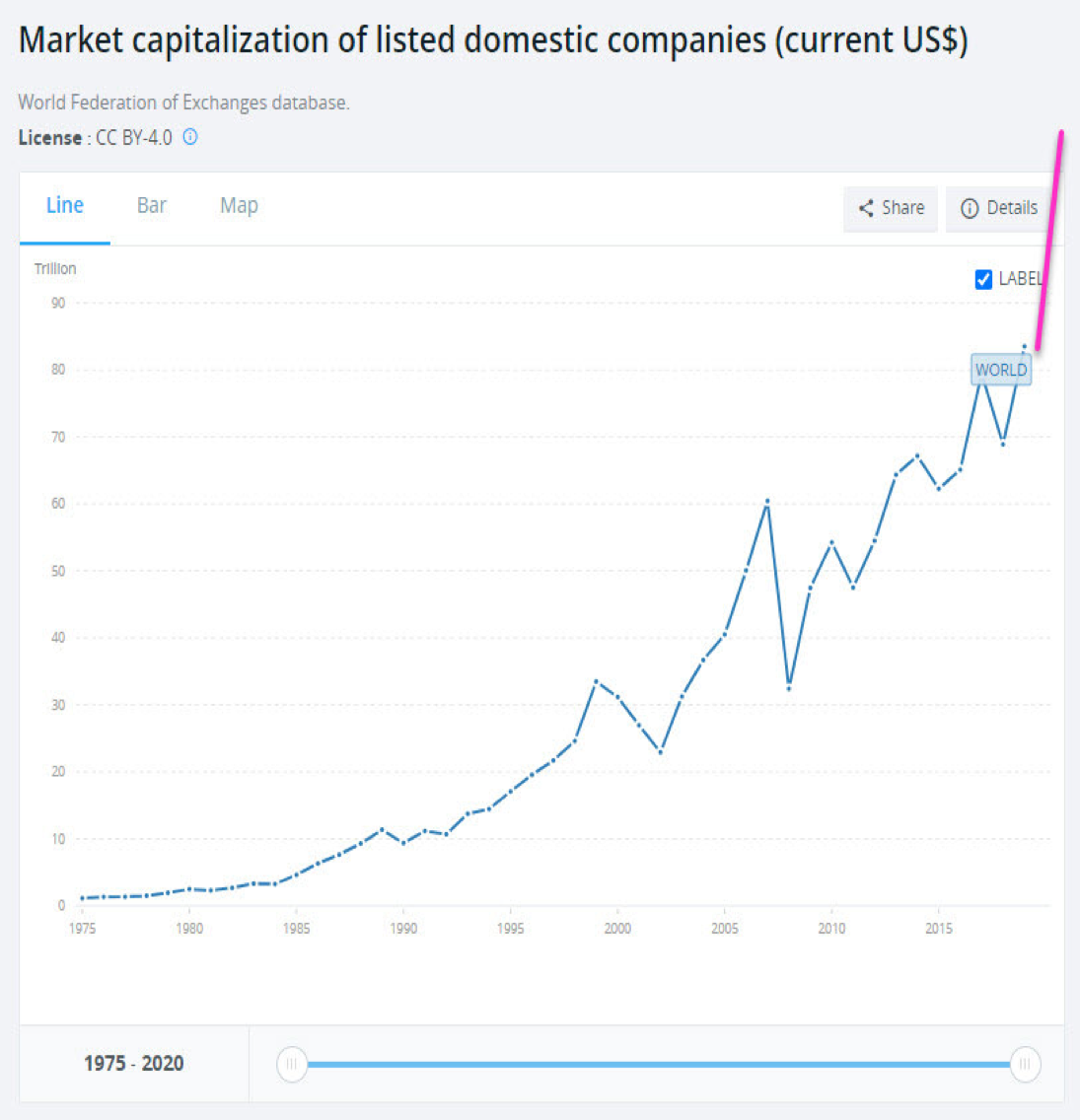

What has transpired over the past 10+ years is that the U.S. equities markets have risen to levels above the 2007~08 peak levels. U.S. equities have also continued to skyrocket higher as foreign investors seek to move assets into U.S. dollar-based equities and ETFs, and away from stagnant, under-performing local equities and assets. Currently, the U.S. stock market total capitalization makes up nearly $48 trillion of the total global market capitalization. The next closest foreign market exchange is China, which makes up nearly $12 trillion in total capitalization.

(Source: https://www.advratings.com/companies/the-largest-stock-exchanges)

When one takes into consideration the massive expansion of state, corporate, consumer and global credit/debt that has taken place over the past 10+ years in China (and the risks associated with servicing that debt as well as increased commodities/asset costs which have taken place over the past 24+ months) one starts to consider if China may suddenly turn into Russia of the late 1990s.

At that time, the inflation rate in Russia reached more than 120% and took place after a number of key economic events set up an almost perfect storm. The aftermath of this event continued to create moderate global market crisis events.

- 1973 and 1979 Energy/Oil Crisis

- 1982 U.S. Interest Rate Peak/Recession

- 1983 Israel Bank/Stock Crisis

- 1987 Black Monday

- 1991 India Economic Crisis

- 1994 Mexican Peso Crisis

- 1998 Russian Financial Crisis

Although the names and dates of these events are much different than what is set up today, imagine the 1973/79 oil/energy crisis was the peak in oil prices in 2018. Imagine the 1982 peak in U.S. interest rates was the peak in interest reached in 2018. Imagine the Israel Bank/Stock Crisis and the 1987 Black Monday was the 2020 COVID crisis. Imaging the 1991 India Economic Crisis, and 1994 Mexican Peso Crisis were the post-COVID economic and current crisis events that have taken place over the past 14+months throughout the world. Now, imagine that China is the new 1998 Russian Financial Crisis taking place. One of the biggest and strongest economies in the world is now at risk of entering a severe inflationary period where excess credit/debt of the past few decades may be washed away – just like what happened in Russia.

(Source: https://www.timetoast.com/timelines/financial-crisis-1900s-2017)

Lastly, remember what came about after these events took place and how isolated the world was from the Russian economic collapse in the late 1990s. The world is not so isolated any longer. If China initiates a credit/debt crisis event, there is a very strong likelihood that the global markets will react to this event moderately violently.

The Hang Seng Index May Foretell A Collapse In The Making

The typical process of the unwinding of this excess credit/debt/liability usually takes place in a common process. First, individuals, corporations and state-run agencies load up on cheap debt while inflation and costs are relatively consistent. Then, as the economy heats up, inflation, commodity prices and equipment/material costs begin to skyrocket – eating into operational profits for these entities. Meanwhile, the need to service the debt/credit persists. As fractures in the system become evident (usually starting with isolated debt defaults by some large entities), investors start pricing greater risks into the credit/debt markets – further complicating the issues for these entities that are burdened with excess debt and diminishing profit margins.

Looking at the Russian Inflation Rate chart, above, any type of major inflationary increase will usually push these entities over the edge in terms of sustainability. Once the cost of refinancing the debt and ongoing profit margins have been squeezed beyond limits, the crisis escalates to a point of implosion.

Given the rise in real estate, commodities, oil/energy costs and other factors, we believe this event may be unfolding right before us in current market trends. China may be the focus of what Russia was in the late 1990s, with extensive credit/debt issues, massive imports of raw materials, commodities, and food, and extensive global foreign debt/credit issues related to the Belt Road project. If a global event were to unfold, which we are only speculating may happen at this point, China and Asia would become the focal point for this process.