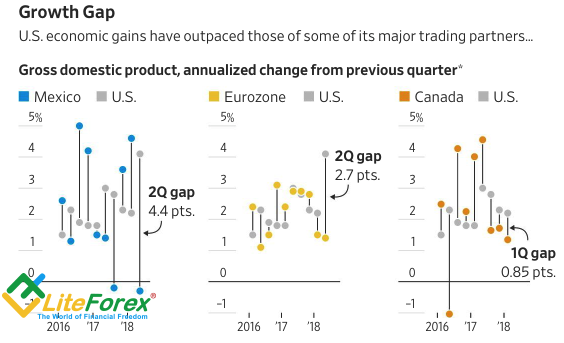

The growth gap between the U.S. and the Euro-area economies in the second quarter is the widest since 2014.

If the eurozone economy continues to gain at the current low pace, the ECB won’t remove its monetary stimulus soon. The Euro-area GDP growth slowed down to 0.3% Q-o-Q in the second quarter, showing the worst results since 2016. Compared to April-June period, European economy expanded by 1.4%, and the growth gap with the U.S. economy (+4.1%) turned out to be the widest since 2014. Different paces of GDP growth, expand the spread between the interest rates, support the capital outflow from the Euro-area to the USA and encourage the EUR/USD bears. The matter is that their past success doesn’t guarantee the same gains in future.

Economic growth gap

Source: Wall Street Journal

According to JP Morgan, most of the positive is already priced in dollar pairs, while a gradual improvement of European economy will drive EUR/USD quotes up the levels of 1.2 and 1.25 in late 2018 and mid-2019. Toronto-Dominion Bank believes that global economy’s recovery will return to the market the idea of monetary normalization by the Fed rival central banks, creating a strong barrier to the USD index further rise. Wells Fargo forecasts that a slowdown in the U.S. GDP growth will make the Fed increase the federal funds rate at a lower pace, which will hit dollar. Morgan Stanley refers to the excessively increased dollar net longs and that Donald Trump is annoyed with the stronger dollar.

EUR/USD bulls were discouraged by an increase in the U.S. personal consumption expenditures rate to 2.2% Y-o-Y in June. The U.S. core PCE is 1.9% up, almost hit the Fed’s target.

Dynamics of U.S. inflation

Source: Bloomberg.

Taking into account the record GDP gains and the U.S. unemployment rate, being near the lowest levels for the past few decade, we can expect the U.S. inflation to further accelerate. The matter is how long the Fed is going to put up with it. The derivative market suggests 68% probability of four federal funds rate hikes in 2018. That is, this factor has almost entirely been included in the quotes of dollar pairs. But will the U.S. economy manage to retain the same growth pace as it featured in the second quarter?

As for euro, there are also some doubts that the eurozone GDP can increase in the second half-year. The ECB expected it would rise during April-June period, explaining the weak start by seasonal factors: bad weather, a flu epidemic, strikes of German workers. Now, the ECB explains the slow economy’s expansion with trade battles, strong euro, removing the monetary stimulus and political crisis in Italy. The last two factors continue working in July-September. In particular, Rome will be adopting the draft budget, which may not be liked by Investors.

In the short-term, the market attention is focused on the Fed’s meeting and the report on the U.S. employment in June. To continue the euro rally, EUR/USD bulls need do storm the resistance at 1.1745. The nearest important support is around 1.1595