Stock market today: S&P 500 ekes out gain ahead of key inflation data

- US inflation cools further, declines in monthly terms

- Dollar slides on Fed-pivot trade

- Yen and euro the main gainers against greenback

- Equities extend recovery, earnings season begins

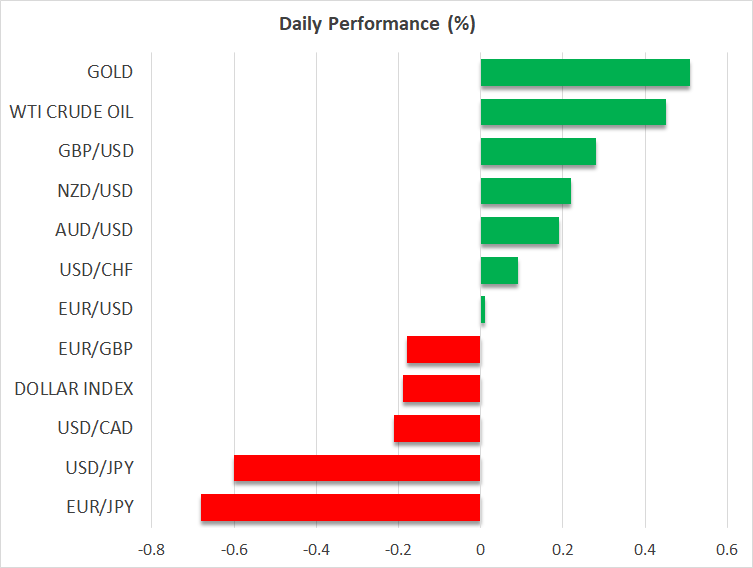

Dollar takes another hit from the US inflation data

The US dollar slid against all the other currencies on Thursday, with the main gainers being the yen and the euro.

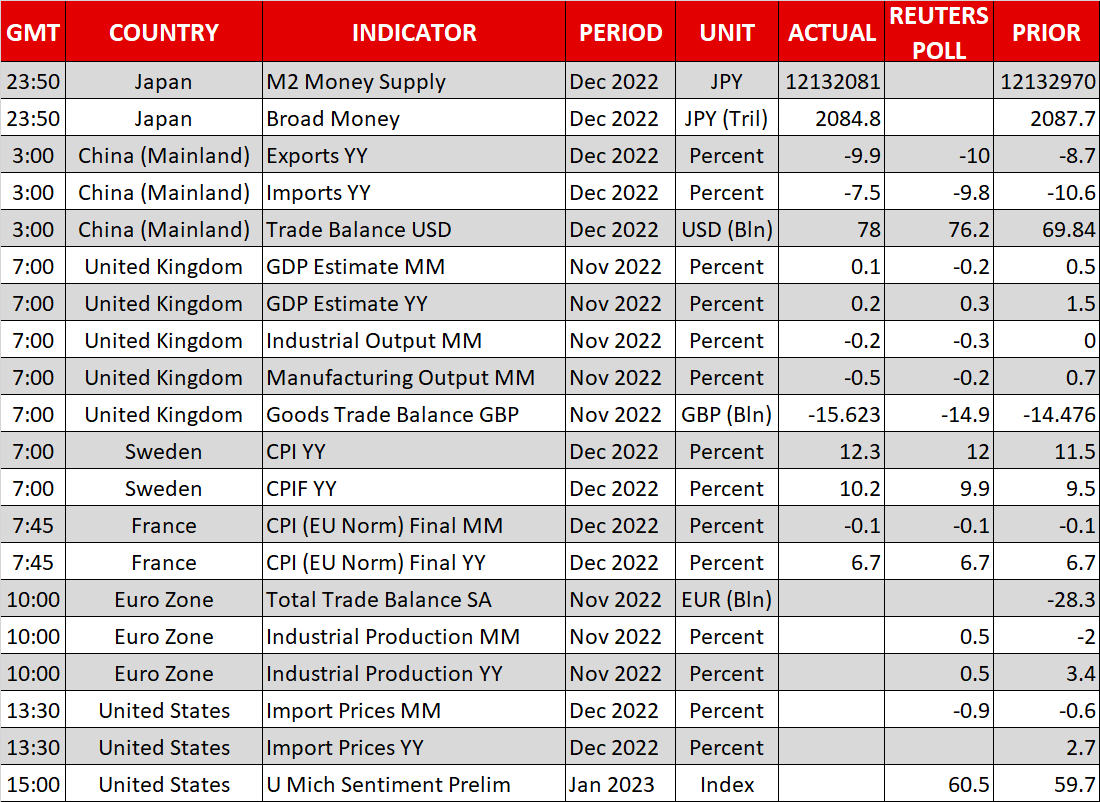

Once again, the US inflation data proved to be the greenback’s biggest nightmare. Both the headline and core CPI rates for December declined to 6.5% y/y and 5.7% y/y from 7.1% and 6.0% respectively, matching the forecasts. However, what came as a surprise and perhaps prompted traders to enter larger dollar short positions may have been the monthly print.

Instead of stagnating as the forecast suggested, consumer prices declined 0.1% m/m, adding credence to the view that inflation may be on a sustained downtrend. With all that in mind, investors may now be more confident that the Fed would eventually need to cut rates at some point this year, despite a couple of policymakers stressing the need for further tightening after the data came out.

According to the Fed funds futures, market participants are now pricing in a 90% chance for the Fed to proceed with a 25bps hike at its upcoming gathering and they are anticipating a terminal rate of around 4.9%. Most importantly though, they are still expecting 50bps worth of rate reductions by the end of the year.

Yen rallies the most as JGB yields break cap, euro takes second place

The yen was the biggest gainer among the major currencies, with dollar/yen falling more than 3% yesterday and today in Asia, confirming a lower low on the daily chart. Following yesterday’s reports that BoJ officials may proceed with additional action to correct distortions in the yield curve, the slowdown in US inflation backed the view that the BoJ may be starting its own tightening crusade at a time when the Fed is headed for the exit.

This is also evident by the narrowing yield differentials between the US and Japan. The 10-year Treasury yield slid to 3.45% from around 3.55%, while Japan’s 10-year yield breached its new cap of 0.50% during the Asian trading today. Ergo, as long as the US-Japan yield differentials continue to narrow, dollar/yen may be poised to continue trending south.

The euro took second place as yesterday’s inflation numbers strengthened the belief that, with underlying price pressures in the Eurozone still accelerating, the ECB may need to continue tightening more aggressively than the Fed henceforth. Euro/dollar emerged above the important barrier of 1.0800, a move that may encourage the bulls to drive the action all the way up to the high of March 31 at 1.1175.

Wall Street cheers CPI data, but focus now turns to earnings

Equities were also affected by the US inflation data, with European and US indices extending their gains. Only Japan’s Nikkei 225 fell sharply today, feeling the heat of the surge in the yen and JGB yields.

However, the prospect of lower interest rates in the US may not be a reason for a long-lasting party if economic data continue to point to deeper wounds. After all, a weak economy is anything but positive for firms and their earnings.

The earnings season begins today with results from several big US banks. Overall S&P 500 earnings are expected to have declined year over year in the fourth quarter, which would be the first negative reading since 2020. Although slightly better-than-expected numbers could result in a relief bounce in the S&P 500, a generally weak picture could leave the door for another slide open.

The S&P 500 could meet strong resistance at the downtrend line drawn from the peak January 4, 2022, or near the key zone of 4,155. A tumble from one of those zones and a subsequent break back below 3,900 could confirm an impulsive wave in the direction of the prevailing downtrend.

The combination of a weaker dollar and lower Treasury yields helped gold climb above $1,880. With recession concerns also a variable in the gold equation, the precious metal may attract additional flows in case investors become more worried about the performance of the global economy, and perhaps slowly head towards the round number of $2,000, near the peak of April 18.