The dollar was lower across the board this morning as investors woke up to the possibility that not only might the budget stalemate drag on, but also it could continue into the fight over the debt ceiling – a possible Financial Armageddon. US stocks were lower yesterday (although Asia was mostly higher this morning as China’s non-manufacturing PMI rose sharply), while 10yr bond yields fell 3 bps and the implied interest rates on Fed Funds futures continued to fall on the assumption that the political fighting would prevent the Fed from tapering any time soon. The lower rates are apparently supportive for EM currencies, which mostly gained vs USD, but I think if the stalemate drags on, the prospect of lower growth in the US will outweigh the prospect of lower US rates for these currencies and EM currencies are likely to fall back.

Indeed, it will be almost impossible for the Fed to come to a conclusion on policy because so much of the data that it depends on – particularly the labor market data – will not be published. The Bureau of Labor Statistics won’t even be collecting data while the government is shut down. In fact no government data will be released while the shutdown is going on, only private-sector data. With luck, the shutdown will be over soon – the median length of time is three days, the average six, and the longest ever so far is 21 – and the data flow won’t be disrupted for long.

However, the polarization between the parties is even worse now than it was in the past and some of the Republicans see the two fights (the budget and the debt ceiling) converging. Moreover, some apparently see this as a good chance to press even more demands on the view that the Democrats will not let the country default – big mistake! "I don't even know if they realize the impact of what it means to default," said Representative Peter King of New York, a moderate Republican. On the contrary, at yesterday’s meeting between President Obama and Congressional leaders, the President said he would not negotiate at all until Republicans agreed to fund the government and to increase the debt ceiling. It looks like the stalemate is set to continue, further disrupting markets. Against that background, I think the dollar is likely to decline further and the safe-haven currencies – CHF and JPY – are likely to benefit. The EUR should also benefit from the Swiss National Bank’s intervention in the EUR/CHF, as well as from yesterday’s resolution of the Italian political crisis. It’s a sad day for the US when US politics look bad in comparison with Italy’s.

The economic calendar today starts with the European service sector PMIs for September, including the UK and Italian ones and the final readings from France, Germany and the Eurozone. The Italian PMI is forecast to rise, while in UK the market expects no change. No change is expected in the final PMIs for the EU, France and Germany from the preliminary versions, but it’s not clear whether economists actually prepare forecasts for the final version. Later in the day, Eurozone retail sales for August are expected to rise. ECB’s Coeure speaks in Toulouse. In the US, jobless claims and factory orders for August are scheduled to be released, but they apparently won’t be, because of the government shutdown. The only US data will be the ISM non-manufacturing composite for September, which is forecast to fall to 57.0 from 58.6 – another USD-negative factor. Finally, there are four Fed speakers: San Francisco Fed President Williams, Dallas Fed President Fisher, Fed Governor Powell (speaking at conference on community banking) and Atlanta Fed President Lockhart speaking on “Recent Developments in the US Labor Market.” Overnight the focus will be on the Bank of Japan, which will conclude a two-day Policy Board meeting; BoJ Governor Kuroda will hold a press conference afterwards. It will be interesting to hear what he has to say about monetary policy in the context of the government’s decision to raise the consumption tax.

The Market:

EUR/USDEUR/USD" title="EUR/USD" src="https://d1-invdn-com.akamaized.net/content/pic5d04d014c3279df30236ff2a83ea8fd6.png" height="812" width="1728">

The EUR/USD moved higher yesterday after Italian Prime Minister Enrico Letta won a vote of confidence in parliament. The pair broke above the upper boundary of its short-term consolidative formation at 1.3564 and in early European trading is heading towards the next hurdle at 1.3654 (R1), where a clear break should challenge February’s highs at 1.3706 (R2). Our short term studies confirm the notion, since the MACD oscillator lies in its bullish zone, above its trigger, while the rate is trading above both the 20- and the 200-period moving averages.

• Support is identified at 1.3564 (S1), 1.3461 (S2) and 1.3400 (S3) respectively.

• Resistance levels are the level of 1.3654 (R1), followed by 1.3706 (R2) and 1.3800 (R3). All are found from the daily chart.

USD/JPYUSD/JPY" title="USD/JPY" src="https://d1-invdn-com.akamaized.net/content/picb186f6ec2f707f4503431d349c2da47c.png" height="812" width="1728">

The USD/JPY moved lower on what looks to be ‘safe haven’ flows, breaking below the 97.73 support level (today’s resistance) and completing a failure swing to the downside. However, during the early European morning the price returned to test the aforementioned level once more. I would consider any upward move as a pullback, since the rate remains below both moving averages and the blue downtrend line. Both the RSI and MACD oscillators support the notion since they continue following their downward sloping path.

• Support levels are at 97.00 (S1), followed by 96.38 (S2) and 95.81 (S3).

• Resistance is identified at 97.73 (R1), followed by 98.50 (R2) and 99.16 (R3).

GBP/USDGBP/USD" title="GBP/USD" src="https://d1-invdn-com.akamaized.net/content/pic787ddc3eff47375b90bc604cf0e91345.png" height="812" width="1728">

The GBP/USD rebounded from the 1.6160 (S1) support level and moved slightly upwards with little GBP-specific news to push price the either way. In early European trading the pair lies between that barrier and the ceiling of 1.6276 (R1). If the bulls are strong enough to overcome that level, I expect them to trigger extensions towards January’s highs at 1.6376 (R2). The rate lies above both the moving averages, while the MACD oscillator lies in its positive territory, confirming that the uptrend is still in effect.

• Support levels are identified at 1.6160 (S1), 1.6000 (S2) and 1.5890 (S3).

• Resistance is found at 1.6276 (R1), followed by 1.6376 (R2) and 1.6570 (R3). The latter two are found from the daily and weekly charts.

GoldXAU/USD" title="XAU/USD" src="https://d1-invdn-com.akamaized.net/content/pic79f1c96eccc443df1e9a02c470a37d0a.png" height="812" width="1728">

Gold also surged as some safe-haven demand finally hit the precious metal, pushing it through the 1291 barrier once more. Overnight gold hit the 1316 (R1) ceiling and moved slightly lower. I believe that the recent upward bias is just a correction of Tuesday’s plunge before the price continue its downtrend. The 20-period moving average remains below the 200-period moving average and alongside with MACD’s negative value, they confirm the bearish picture for the yellow metal.

• Support levels are at 1291 (S1), followed by 1273 (S2) and 1242 (S3). The latter one is found from the daily chart.

• Resistance is identified at the 1316 (R1) level, followed by 1343 (R2) and 1368 (R3).

Oil

WTI surged yesterday, breaking above the 102.23 and finding resistance at 104.14 (R1). However, since the price remains in its downward sloping channel I consider the upside move as a pullback before the bears prevail again. The 20-period moving average remains below the 200-period moving average, confirming the validity of the downward path.

• Support levels are at 102.23 (S1), 101.02 (S2) and 99.18 (S3). The latter one is identified on the daily chart.

• Resistance levels are at 104.19 (R1), followed by 106.06 (R2) and 108.13 (R3).

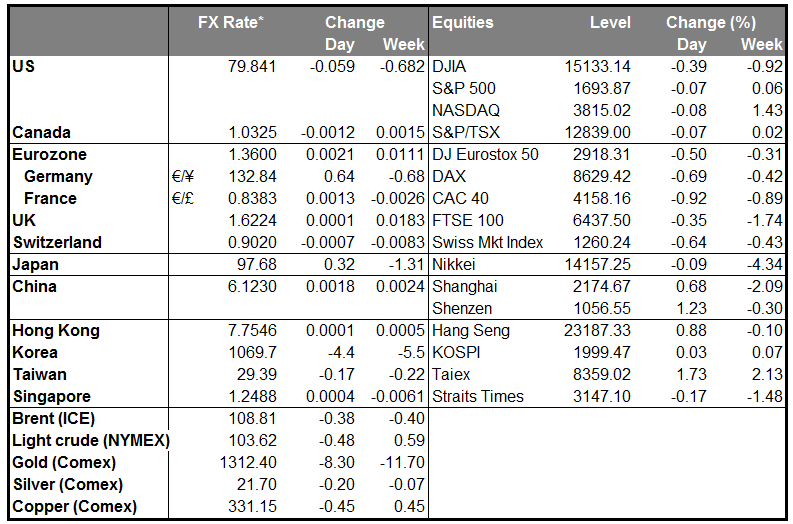

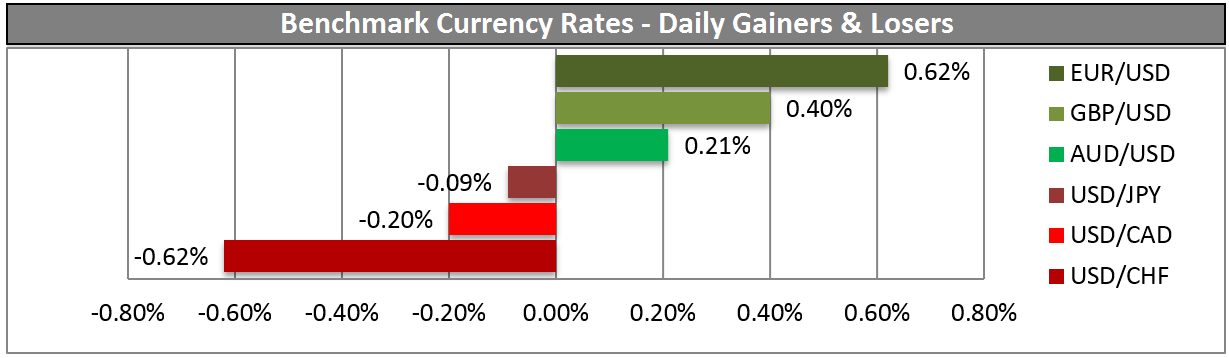

BENCHMARK CURRENCY RATES - DAILY GAINERS AND LOSERS

MARKETS SUMMARY: