(Bloomberg) -- The Federal Reserve’s cornerstone method for determining whether US banks can survive an economic crisis has for years had a glaring oversight: Regulators haven’t tested a scenario that resembles the economy of 2023, and the financial conditions that precipitated the downfall of Silicon Valley Bank, in nearly a decade.

Fed officials have touted the annual stress tests as their marquee supervision method to evaluate the health and resilience of the country’s biggest banks.

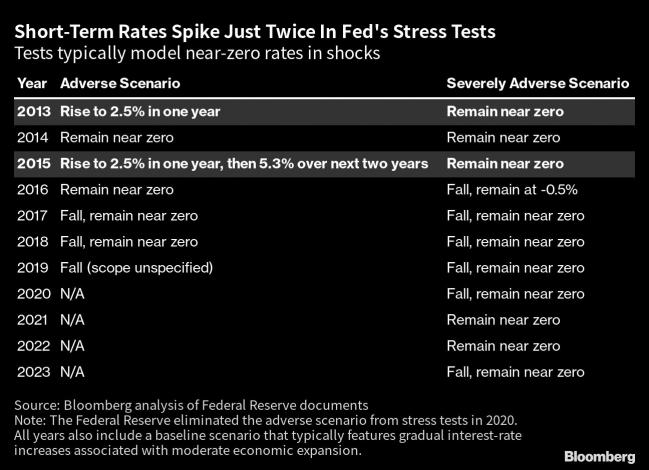

But with two exceptions, in 2013 and 2015, the scenarios have almost exclusively modeled mild to severe recessions with declining inflation and nosediving short-term interest rates. That narrow range fails to capture the realities of the pandemic recovery, when nearly a year of rapid rate hikes eroded the value of bank portfolios like SVB’s.

“A stress test is only as good as the scenarios it tests,” said Aaron Klein, a senior fellow in economic studies at the Brookings Institution. “This was a basic scenario: the Fed raising interest rates suddenly and sharply.”

A more realistic stress-test scenario wouldn’t have solved the institutional problems that toppled SVB, regulation experts said. But the lack of rate-hike modeling does point to a hole in how Fed officials think about financial risk.

“Whether the Fed stress-tested it or not, the Fed knew this interest rate hike was coming,” Klein said, “and it was looking at one of the largest banks it directly supervises having a hundred billion dollars of unhedged mortgage-backed securities that would suffer significant losses.”

The Fed’s baseline scenarios typically include gradual rate increases associated with moderate economic growth, and sometimes feature steepening yield curves. The central bank is adding an additional market shock to its 2023 stress tests that more closely reflects current economic conditions, but won’t penalize banks if they don’t pass. The stress test is also just one of the Fed’s supervisory tools, albeit its most transparent.

Lawmaker Scrutiny

Still, SVB’s collapse has Washington lawmakers scrutinizing whether the Fed’s resiliency measures are an effective hedge against financial instability. The bank on Friday became the biggest US lender to fail in more than a decade after a tumultuous week that saw an unsuccessful attempt to raise capital and a cash exodus from the tech startups that had fueled the lender’s rise.

SVB for years fell below the Fed’s $50 billion threshold for annual stress-testing. As the firm grew, its executives successfully lobbied for a 2018 law that raised the threshold even higher, exempting mid-sized banks from annual testing requirements. SVB, which had between $100 billion and $250 billion in assets, would only have been subject to periodic testing, and wasn’t tested last year.

A stress test may not have been the right tool to identify SVB’s problems, which were inherent to its business model, said Steven Kelly, a senior researcher at the Yale Program on Financial Stability.

Nevertheless, the Fed missed an opportunity in 2022 to add interest-rate risks to the stress test, Kelly said. The central bank raised rates from near zero in March 2022, and announced that year’s stress-test scenarios just a few weeks prior, when the risks were already clear, he said.

Scholars have for years put interest-rate hikes on the back burner when assessing financial risk, Sean Vanatta, an economics lecturer at the University of Glasgow, wrote in an email. Stress tests, which were implemented after the 2007-09 global financial crisis, are almost always premised on a moderate or deep economic downturn that envisions rising unemployment and interest rates falling to zero.

More Intense

The exceptions to that were in 2013 and 2015, when the Fed asked banks to game out how they would manage a mild recession with inflation — as measured by the consumer price index — above 4% and a rapid rise in short-term US Treasury yields to 2.5% in one year. The 2015 scenario also envisioned an additional hike of nearly three percentage points over the next two years; all 31 big banks passed that test.

The pandemic recovery, meanwhile, has fueled economic conditions that were far more intense on both key metrics: CPI inflation topped 9% in June, and was still elevated at 6% last month, while the 3-month Treasury yield rose from 0.4% in March 2022 to nearly 5% earlier this month.

The Fed added a so-called “exploratory market shock” to stress tests for the first time in 2023, on top of their usual severe recession hypothetical. The goal, they wrote in a release, is to expand regulators’ understanding of resilience and assess the potential of multiple scenarios in future stress-test exercises.

SVB’s failure has also highlighted the shortcomings of any one resiliency test. A new Bank Policy Institute report found that the failed lender would have passed a liquidity test with “flying colors” – an unsurprising finding, the report said, because SVB’s failure appears to be one of management and supervision, rather than regulation.

“Banking supervision is, and must always be, more than stress testing,” Vanatta said. “The critical question for SVB and all the other troubled banks is: What did supervisors know, when? What did they advise? And what power did they have to enforce that advice?”

©2023 Bloomberg L.P.