Goldman Sachs (NYSE:GS)'s report on India's Clean Energy sector outlines a significant rise in transmission capex, driven by the transition towards renewable energy sources. The report initiates coverage on Power Grid (NS:PGRD), Hitachi (OTC:HTHIY) (Buy), and Schneider (Sell).

Power Grid Corporation of India - Buy (INR 355; 29% upside)

Power Grid Corporation of India (PGCIL) emerges as a significant beneficiary in India's energy transition, with its extensive transmission infrastructure poised to capture a substantial portion of the estimated US$500 billion grid capex by FY50E. PGCIL's strong financial position, including a large balance sheet and low cost of debt, positions it favorably to fund around 30% of India's planned grid capex by FY32E while maintaining dividend payouts.

Despite its advantageous position, PGCIL's long-term beta is deemed higher than global peers, potentially impacting its cost of equity and fair value. The removal of regulatory overhang through tariff notifications further bolsters PGCIL's outlook, with the grandfathering of legacy assets providing long-term stability. This regulatory clarity enhances investor confidence and underscores PGCIL's strategic position in the evolving energy landscape.

Hitachi Energy India - Buy (INR 8,250; 9% upside)

Hitachi Energy India is positioned as a direct manufacturing beneficiary. With robust indigenized manufacturing capabilities and leadership in high-voltage transmission technology, Hitachi is poised to capitalize on India's estimated US$105 billion grid capex by FY32E. The company manufactures a significant portion of its global equipment portfolio domestically and stands to benefit from expanding opportunities in high-value transmission projects, grid digitization, and supply chain diversification.

The investment thesis is reinforced by expectations of rapid earnings growth, driven by a surge in ordering activity and margin expansion. Hitachi Energy India's favorable risk-reward profile is supported by a fast-expanding TAM and technological leadership. However, risks include potential delays in transmission project awards, increased competitive intensity, and higher royalty payments to the global parent company. The valuation methodology incorporates forward-looking free cash flows and a target price of INR 8,250, reflecting an implied FY26E P/E of 60x. Overall, Hitachi Energy India is positioned to leverage India's evolving energy landscape and emerge as a significant player in the sector's transformation.

Schneider Electric (NS:SEIN) Infrastructure - Sell (INR 470; 41% downside)

Schneider Electric Infra (SEIL) is poised to benefit from India's Revamped Distribution System Scheme (RDSS), expected to drive a US$37 billion distribution system expansion over 5 years, with SEIL having a stake in over 50% of the capex. The company's expertise in energy management positions it to leverage the increasing importance of energy efficiency, particularly with the impending EU Carbon Border Adjustment Mechanism.

However, despite growth prospects, the stock's valuation, trading at around 57x FY26E P/E, appears high considering that expected RoCE remains below 30%. SEIL's products, lacking high-end technology, might not justify current multiples. Earnings are forecasted to grow at a 43% CAGR between FY23-26E, primarily driven by RDSS-led distribution capex, mix improvement, and margin expansion. The target price of INR 470/sh reflects a DCF valuation method, anticipating a 25-year free cash flow with a 5% terminal growth rate.

Upside risks include faster-than-expected distribution capex ramp-up, privatization of power distribution, and higher carbon taxes. Conversely, lower distribution capex and increased competition pose downside risks.

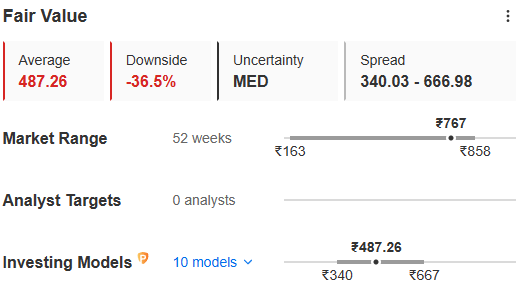

Image Source: InvestingPro+

InvestingPro users already know that the stock is overvalued and by how much. The power fair value feature that precisely calculates the true worth of the stock is INR 478.2 per share, which is very close to Goldman Sachs’ target price. This feature is available for all stocks and can drastically help investors maintain a healthy portfolio by eliminating overvalued stocks and adding undervalued ones, without even having to wait for such reports by institutions.

SALE: Unlock your investment potential with InvestingPro! Advanced stock analysis tool identifies undervalued and overvalued stocks, empowering you to make informed decisions. With a 69% discount, seize the opportunity by clicking here to capitalize on the valuation gap before it closes!"

X (formerly, Twitter) - Aayush Khanna