(Bloomberg) -- For all the focus on whether the Federal Reserve is about to pause its interest-rate hikes, there’s another critical policy decision sure to draw plenty of attention come Wednesday: What the central bank does with its massive pile of bond holdings.

The banking-sector turmoil, combined with a previous increase in funding pressures, has left financial markets keenly attuned to what the Fed will say about its $8.6 trillion balance sheet.

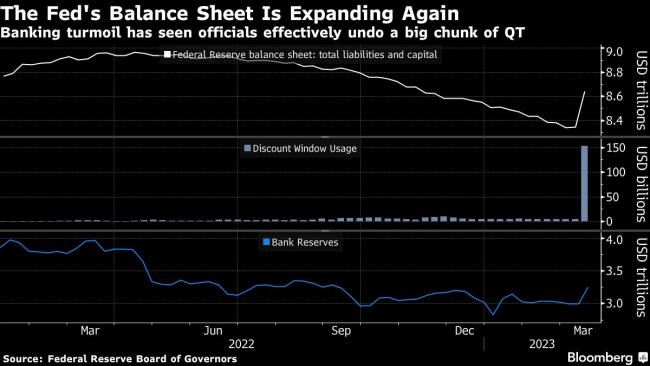

Until this month the stash had been shrinking as part of the Fed’s efforts to return it back to pre-pandemic levels. But now it has started to expand again as the Fed acts to bolster the banking system through a slate of emergency lending programs. Its latest step came Sunday, when it moved with other central banks to boost US dollar liquidity.

Some say financial-stability concern may spur policymakers to dial back the runoff of its bond portfolio, a process known as quantitative tightening that’s designed to drain reserves from the system. Still, others argue that even if the Fed does pause its rate increases, the central bank’s overarching goal of taming inflation means it’s unlikely it will signal any shift this week in efforts to shrink the holdings of Treasuries and mortgage-backed debt. The one exception, they note, would be if stress in the banking sector were to become much more severe.

The Fed’s move to backstop US banks “clearly expands the Fed’s balance sheet,” said Subadra Rajappa, head of US rates strategy at Societe Generale (OTC:SCGLY) SA. If usage of the Fed’s liquidity facilities is “small and contained they probably continue QT, but if the take-up is large then they probably stop as it then starts to raise concerns over reserve scarcity.”

The fate of the Fed’s portfolio is a subject of debate after the collapse of several US lenders led the central bank to create a new emergency backstop, known as the Bank Term Funding Program, which it announced March 12. Banks borrowed $153 billion from the Fed’s discount window — lenders’ traditional liquidity backstop — in the week ended March 15, Fed data show, a record that eclipsed the previous all-time high set during the 2008 financial crisis. They also tapped the new program for $11.9 billion.

The various liquidity programs added about $300 billion to the Fed’s balance sheet last week, reversing about half of the reduction the central bank has achieved since the runoff began last June. But some economists say the two tracks can work in tandem, with the banking efforts targeting financial stability and QT remaining a steady part of the Fed’s plan to remove the support it provided during the pandemic.

“I expect that quantitative tightening will continue,” former New York Fed President William Dudley said in an interview on Bloomberg Surveillance. That program is “very separate and different” from the Fed’s steps to shore up confidence in the banking system, he said.

Even before the trio of lenders failed this month, there were already signs that some institutions needed to access wholesale funding markets to replace deposit outflows, with customers shifting cash into higher-yielding alternatives as the Fed lifted rates. Federal Home Loan Banks’ total advances to members had already more than doubled to $819 billion last year. And until the FHLBs ramped up issuance last week to support member institutions, volumes in the federal funds market — where FHLBs are the largest lender of overnight cash — had reached seven-year highs amid banks’ increased funding needs.

Well before the Fed announced QT, analysts had expected the unwind was going to result in excess liquidity draining faster from the banks than other areas of the financial system, like money-market funds, that have parked more than $2 trillion at the Fed’s reverse repurchase agreement facility. In the minutes of the last central bank gathering, officials even discussed risks of temporary funding pressures.

Still, the Fed’s response to the banking crisis — providing liquidity to lenders — is a wrench in the works for some analysts, who say it risks sending confusing signals.

“The Fed doing its new emergency bank program and QT at the same time is totally contradictory policies,” said Michael Darda, chief economist at Roth MKM. “The Fed is now at cross purposes – working against itself. They are trying to support the banking system on one hand but on the other side they are doing things that will constrain it.”

The counter to the argument that Fed is sending mixed signals is that this new program is more akin to what the Bank of England did last year, when it bought government bonds to stabilize markets — an emergency action as opposed to a broad thrust of monetary policy.

Sunday Developments

Announcements Sunday that UBS Group AG (SIX:UBSG) would acquire Credit Suisse Group AG and that five central banks would take coordinated action to boost liquidity in US dollar swap arrangements increased concern that financial risks may be greater than initially feared. Existing central bank liquidity swap lines with the Fed have been largely untouched amid the most recent market turmoil.

Former Fed Governor Laurence Meyer and his colleagues at research firm Monetary Policy Analytics said in a note Sunday night that they saw a greater chance of the Fed pausing or adjusting its balance-sheet plan after the news.

At the very least, it all stands to make Fed Chair Jerome Powell’s job that much harder Wednesday when he’s likely to face questions about how the central bank’s various policies fit together.

Fed officials haven’t provided a recent timeline for when they expect to wind down QT, but Powell said last month it will be a couple of years until the balance sheet reaches a level where bank reserves are still ample.

Whether that’s still his base case remains to be seen.

“QT is a part of their monetary policy, and so whatever they do with QT is also a signal about what they do about the funds rate and whether they’re going to continue hiking, whether they’re going to hold, how long they’re going to hold and when they start easing,” said Derek Tang, an economist at LH Meyer/Monetary Policy Analytics.

(Adds comments from former New York Fed President William Dudley in 8th paragraph.)

©2023 Bloomberg L.P.