We all know something is coming from the Bank of Japan, but what? The market in the shortest term is about whether it has overdone the JPY selling for now. Meanwhile, US markets are closed for the day.

Germany local elections

State elections in Lower Saxony over the weekend saw the SPD/Green party just edge out Merkel’s CDU for a single seat majority in a sign that the national election set for September of this year will be a nail-biter. Previously, the odd thing was that Merkel’s CDU was becoming more popular than ever, but voters for the coalition partner FDP were abandoning a sinking ship as some fear that the party may fail to reach the voting threshold (5%) for representation in parliament in September. But the Lower Saxony results saw a sharp improvement in the FDP’s results. According to sources quoted in this Bloomberg article, there may enough CDU voters willing to switch to FDP to guarantee that the party continues to poll at least 5%.

Bank of Japan

The Bank of Japan announcement is on tap for tonight and the JPY crosses are consolidating a bit in recognition of the import of this event risk. The baseline expectations are for the announcement of a 2% inflation target, possibly together with the government, as the Economics Minister Amari (he of last week’s gaffe that saw JPY consolidating and then un-consolidating when he retracted his statement) will be attending the meeting. The BoJ may also announce yet another round of new asset purchases announcement (another ¥10 trillion log on the monetary fire is perhaps the baseline expectation there, but it is the hints toward what size of foreign assets that will be purchases that will be more interesting down the line).

The bigger questions await the appointment of the new Bank of Japan leadership in a couple of months’ time. Beyond that, it is about the market trying to decide what it has already priced in and positioning. It is interesting to note in recent weeks that the positioning in the US futures market has actually been declining slightly ever week for the last six weeks through last Tuesday. Two ways to skin that cat: room for positioning to expand again with fresh shorts, or a sign that there is waning appetite to short the JPY at these levels.

From this point, I think any further sharp weakening in the JPY will begin to provoke a strong response from Japan’s trading partners. In a world of fiat currencies backed only by faith and in a world of weak global demand, one nation’s gains from a weaker currency are another nation’s losses. That’s what provokes currency wars in the end.

US fiscal standoff

There were signs late last week from Republicans that they will look to extend the debt ceiling three months to avoid a disaster in the making. On the surface, this appears to be good news, but it’s not really if we think about it for a moment: yes, it may relieve the immediate pressure on the Treasury or the need for President Obama to make unprecedented steps (there is a constitutional argument that the president has the right to enforce spending that the Congress voted into place) and thus provoke some kind of constitutional crisis. But it also merely extends the uncertainty and the gridlock, which could eventually wear down market confidence.

Looking ahead

The rest of the week for major FX will be sorting through the results of the BoJ meeting and positioning and technicals, barring any major new political developments in the fiscal negotiations in the US or ad hoc developments in Europe.

Technical observations

A few basic technical observations as we stare down the week ahead

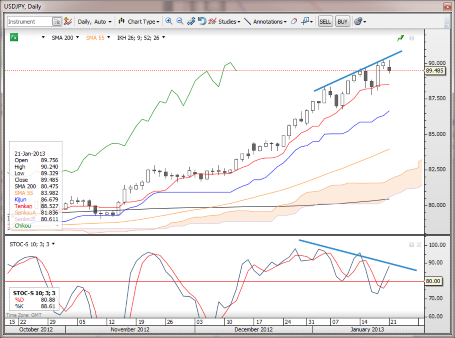

USD/JPY – 90 is obviously a major psychological barrier and we have triple divergence on the momentum indicators – could we be looking at a brutal sharp move to sub-87.00 levels? I’m not one to stand in front of a stampede, but the short-term volatility risk may be greater to the downside, even if we see a minor surge to new highs if the BoJ proves even more dovish than the market expects.

Chart: USD/JPY

USD/JPY" title="USD/JPY" width="455" height="338">

USD/JPY" title="USD/JPY" width="455" height="338">

EUR/JPY – In the event of a JPY correction stronger – this is the cross that is likely to move the most. We could be looking at 115 or even 112 in no time in the right circumstances – 400-500 pips, and still be in a bull market…120 is the psychological resistance here.

EUR/USD – 1.3250 area looks interesting and needs to fall to underline any tactical argument for a bearish follow-up move lower. A big break back below 1.3170 is needed to more firmly for the bears to get a more structural toehold. 1.3400 is the important resistance and must be taken out for bulls to get traction.

EUR/GBP – 0.8400/0.8500 is a key resistance area and the move of late has been very extreme. I would look for the pair to carve out a new range soon between 0.8250 and 0.8400/0.8500. The downside could be quick and sharp if the JPY moves stronger and the EUR/JPY is consolidating because I believe it is EUR/JPY that has been a major contributor to this move.

GBP/USD – My, how times have changed. 1.5910 is the 200-day moving average and first resistance, followed by 1.6000. The previous rally was mortally wounded by last week’s follow-up sell-off. Further forward, a break below the 1.5825 area could open up a full scale retreat back to the old sub-1.5300 range lows.

AUD/USD – 1.0485/1.0500 has not yet been taken out on the close – the bears need this as a tactical trigger as complacency in risk assets is mind-boggling. On the other hand, we remain in limbo to the upside unless the chart can take out 1.0600. Every thrust to that level since last summer has been rejected.

Stay careful out there.

Economic Data Highlights

- UK January Rightmove House Prices rose +0.2% MoM and +2.4% YoY vs. +1.4% YoY in December

- Germany December Producer Prices out at -0.3% MoM and +1.5% YoY vs. 0.0%/+1.7% expected, respectively and vs. +1.4% YoY in November

- US Markets Closed for Martin Luther King, Jr. memorial day

- Canada November Wholesale Sales (1330)

- UK BoE’s Haldane to Testify to UK parliament (1415)

- UK Former BoE member Posen to testify to UK parliament (1630)

- Bank of Japan announcement (no time given – usually early GMT hours - Tuesday)