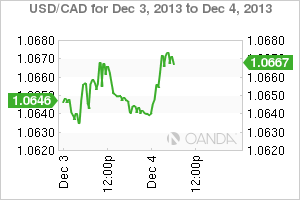

The grass is not always greener on the other side, even with Ireland being thrown into the mix. Persistently soft European data certainly opens the door for the ECB to be proactive once again, and perhaps even as early as at tomorrows ECB meeting. A plethora of Central Bank monetary decisions announcements will be dominating this week, at least until Friday's US non-farm payrolls. Late Monday, the RBA down-under did not deviate from their last meetings script, holding rates steady at +2.5%. Governor Stevens even took time out to continue to whine about their overvalued AUD. Today, the Bank of Canada gets to hog the limelight, albeit briefly, before investors have to once again square off with the "Old Lady" and the ECB tomorrow. USD/CAD" border="0" height="200" width="300">

USD/CAD" border="0" height="200" width="300">

Governor Poloz at the Bank of Canada is expected to hold the line, and keep benchmark lending rates on hold at +1.00%, with no significant change in guidance. Since the previous decision, data have been mostly in line with consensus, and global inflation pressures have been contained. Last time out, the committee was notably more "neutral" than in their previous decision. Has recent data any cause for Canadian policy makers to waiver again? No, not at all - current data does not warrant another change in Canadian policy stance for the time being. The market remains relatively bearish on the loonie. Obviously any further dovish hints and the CAD will be expected to come under further attack. As NFP draws closer, dealers will expect the principal US dollar to dominate price action. The market believes that the reporting of a strong job environment stateside is proof enough for a December taper.  EUR/USD" border="0" height="200" width="300">

EUR/USD" border="0" height="200" width="300">

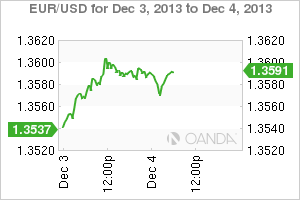

The trend remains – the Euro-zone continues to rely on Germany to support whatever economic growth the region is producing. This morning's mid-week Purchasing Managing surveys suggest that the relationship is perhaps even more symbiotic than the market had perceived. The Euro PMI fell to 51.7 last month from 51.9 in October. The report is a strong indicator that the private sector activity once again slowed during that month. Nationally, Germany continues to independently play the dominant role in pushing forward the whole regions economic development. It's own composite PMI rose again to 55.4 on the month, backed by a rise in the service sector. Analysts note that activity in the country's private sector grew at the fastest pace in two-and-a-half years. A stark reminder of how perilous growth is in the region, both France and Italy's private sectors contracted at the fastest pace in nearly six-month.  EUR/JPY" border="0" height="200" width="300">

EUR/JPY" border="0" height="200" width="300">

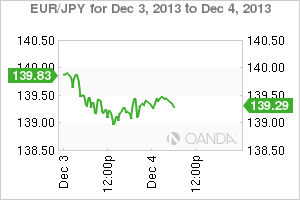

It's no surprise that the data should suggest that growth in Germany is expected to develop in Q4 by as much as +0.5%. However, the Euro-zones number two and three economies outlook do not look so rosy. France and Italy are expected to continue to battle their own growth concerns. The dismal composite data for either country this week would again suggest further contraction in either economy in Q4. Germany's superior services sector boomed last month, jumping to 55.7 from 52.9 – a new 10-month high. By contrast, the French and Italian service sector contracted for the first time in three months.

The Euro-zones service sector basically has put in a repeat performance to Monday's manufacturing PMI's. France and Italy have both come in weaker than expected, while Germany and a few of the peripheries, continue to surprise to the upside. With divergence appearing within the core (Germany and France) and the periphery (Spain and Italy) there is certainly room for Draghi and company at the ECB to follow up its rate cut last month with further easing tomorrow. Fixed income traders believer there remains a case for the ECB to deal with the decline in excess liquidity, which is starting to "increase volatility in money markets." There remain a number of innovative options open for ECB policy makers, ranging from cutting the reserve requirement to leaving the SMP program "partially or fully unsterilized." But, will Draghi and company have the gall to proceed as early as tomorrow? USD/JPY" border="0" height="200" width="300">

USD/JPY" border="0" height="200" width="300">

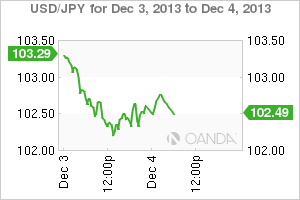

But before Draghi can ever give the "nod" investors will have to deal with US ADP and ISM data points for further Fed clues towards a December taper. ADP of late has had little bearing on the monthly NFP numbers for awhile, however, expect many market participants to make a strong argument particularly if the outcome strongly surprises. Be aware, that a particularly strong indication for Friday carries the risk of the market assigning a higher probability to a December taper, which should support a stronger USD and higher US 10-year yields.

Original post

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Will The Dollar Get The Green Light From BOC And ECB?

Published 12/04/2013, 06:57 AM

Updated 07/09/2023, 06:31 AM

Will The Dollar Get The Green Light From BOC And ECB?

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.