It has been about a month since the last earnings report for Arthur J. Gallagher & Co. (NYSE:AJG) . Shares have added about 5.1% in that time frame, outperforming the market.

Will the recent positive trend continue leading up to its next earnings release, or is AJG due for a pullback? Before we dive into how investors and analysts have reacted as of late, let's take a quick look at the most recent earnings report in order to get a better handle on the important drivers.

Arthur J. Gallagher Beats on Q4 Earnings and Revenues

Arthur J. Gallagher reported fourth-quarter 2017 adjusted net earnings of 82 cents per share, which beat the Zacks Consensus Estimate by about 9.3%. Also, the bottom line improved 24.2% on a year-over-year basis.

The company’s performance was driven by solid organic growth, outstanding revenue improvement from the tuck-in mergers and acquisitions and strong margin expansion. The company also witnessed solid performance across all its segments.

Net income rose 8% year over year to 57 cents per share.

Operational Update

Total revenue was $1.6 billion, up 15.5% year over year. This upside was driven by growth in total revenue in the Brokerage, Risk Management as well as Corporate segments. The top line surpassed the Zacks Consensus Estimate by 7.8%.

Total commissions and fees earned increased nearly 10% year over year to $1.1 billion in the quarter.

Arthur J. Gallagher’s total expense rose 15.2% year over year to $1.5 billion in the quarter. Expenses escalated due to a rise in compensation costs, operating costs, interest expenses, cost of revenues from clean coal activities, plus higher depreciation and amortization expenses.

Earnings before interest, tax, depreciation and amortization and change in estimated acquisition earnout payables (EBITDAC) increased 8.1% to $213.3 million.

Full-Year Highlights

Arthur J. Gallagher’s 2017 adjusted net earnings of $3.06 per share beat the Zacks Consensus Estimate of $2.99. Also, the bottom line improved 12% over 2016.

Revenues came in at $6.2 billion, beating the Zacks Consensus Estimate of $6.1 billion. The top line improved 3% over 2016.

Segment Results

Brokerage: Adjusted revenues of $1 billion grew 12.9% year over year on higher fees, commissions, supplemental revenues and contingent revenues. Total expense shot up nearly 11% year over year to $845.5 million.

Adjusted EBITDAC rose 12.4% to $237 million.

Risk Management: Adjusted revenues were up 6.2% year over year to $197.1 million, owing to higher fees. Total expenses increased 7.9% year over year to $173.8 million.

Adjusted EBITDAC climbed 5.3% year over year to $34 million.

Corporate: Total revenues came in at $401.7 million, up 28% year over year. Total expenses increased 26.5% year over year to $497.6 million.

EBITDAC was at a loss of $57.7 million, wider than a loss of $45.8 million in the prior-year quarter.

Financial Update

As of Dec 31, 2017, total assets were $12.9 billion, up 12.2% from year-end 2016.

Cash and cash equivalents at the year-end increased 21% from the 2016 level to $2.3 billion.

Shareholders’ equity increased about 13.5% from the 2016-end level to $4.2 billion at the end of 2017.

Acquisition Update

In the fourth quarter, the company closed nine acquisitions with annualized revenues of over $29.3 million, taking the full-year tally to 36 acquisitions closed with annualized revenues of over $159 million.

How Have Estimates Been Moving Since Then?

In the past month, investors have witnessed an upward trend in fresh estimates. There have been three revisions higher for the current quarter. While looking back an additional 30 days, we can see even more upward momentum. There have been six moves up in the last two months. In the past month, the consensus estimate has shifted by 14.7% due to these changes.

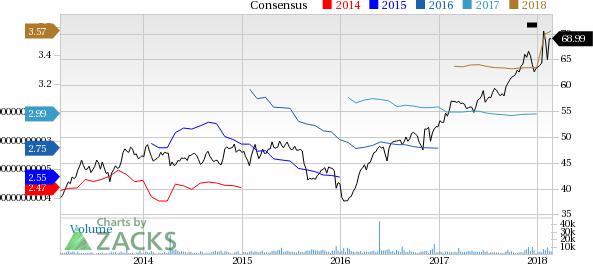

Arthur J. Gallagher & Co. Price and Consensus

Arthur J. Gallagher & Co. Price and Consensus | Arthur J. Gallagher & Co. Quote

VGM Scores

At this time, AJG has a nice Growth Score of B, though it is lagging a lot on the momentum front with D. The stock was also allocated a grade of D on the value side, putting it in the bottom 40% for this investment strategy.

Overall,the stock has an aggregate VGM Score of C. If you aren't focused on one strategy, this score is the one you should be interested in.

Zacks' style scores indicate that the company's stock is suitable solely for growth investors.

Outlook

Estimates have been trending upward for the stock and the magnitude of these revisions looks promising. It comes with little surprise AJG has a Zacks Rank #2 (Buy). We expect an above average return from the stock in the next few months.

Arthur J. Gallagher & Co. (AJG): Free Stock Analysis Report

Original post

Zacks Investment Research