This week appears relatively light compared to the previous ones. We have no central bank decision on the agenda, while the most important events may be the US CPIs for April and the UK GDP for Q1.

Inflation in the US is expected to have surged further, raising questions as to whether the Fed should start considering tapering QE. The UK GDP is expected to have contracted in the first quarter of the year, but to have performed very well during March.

Monday appears a relatively light day with no major indicators or releases on the agenda.

On Tuesday, during the Asian morning, we get China’s CPI and PPI for April. Both rates are expected to have risen to +1.0% yoy and +6.6% yoy from +0.4% and +4.4% respectively.

During the European session, we have Germany’s ZEW survey for May. The current conditions index is expected to have increased to -42.6 from -48.8, while the economic sentiment one is forecast to have risen fractionally to 71.0 from 70.7.

Following the improvement in the PMIs around the Eurozone in the last months, this will confirm that the bloc’s growth engine continues to recover from the damages of the coronavirus pandemic.

At the latest ECB gathering, officials kept their policy unchanged and did not discuss plans for their bond purchases, but given that at the next meeting we will also get new staff macroeconomic projections, we may also get hints with regards to the Bank’s future plans. With the recovery underway, officials may provide clues as to whether and when they intend to reduce the pace of their QE program.

Later in the day, the US JOLTs job openings for March are coming out and the forecast points to a small acceleration, to 7.500mn from 7.367mn in February.

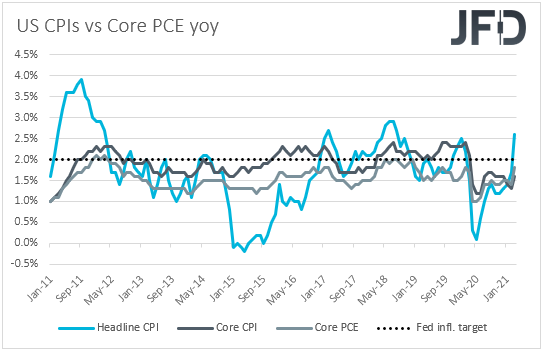

On Wednesday, the main item on the agenda may be the US CPIs for April. The headline rate is expected to have rallied to +3.6% yoy from +2.6%, further above the Fed’s inflation goal of 2.0%, while the core rate is anticipated to have increased to +2.3% yoy from +1.6%.

The fact that the core rate will also climb decently higher may raise questions as to whether the surge in headline inflation will prove to be temporary and thus, whether the Fed should start considering scaling back its monetary policy earlier.

That said, with the US employment report disappointing on Friday, it seems that Fed officials may not be in a rush to alter their policy any time soon. We will get to hear from several of them this week, who may attempt clear the picture around the Fed’s future plans even further. Those speaking after the inflation data may be even more interesting to listen as they will provide an even more updated view.

If they indeed stick to their guns that it is still too early to start discussing about policy normalization, equites are likely to edge higher, while the US dollar and other safe havens, like the Japanese yen, are likely to stay under selling interest.

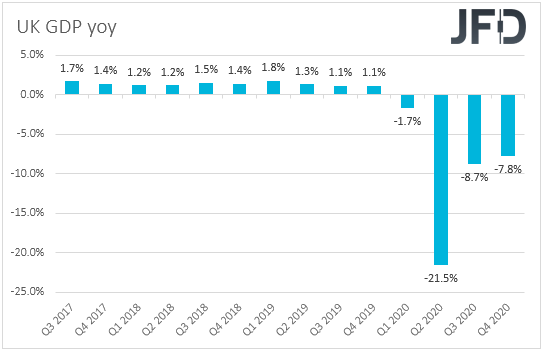

Ahead of the US CPIs, during the early European morning, the UK preliminary GDP for Q1 is due to be released and expectations are for a 1.7% qoq contraction after a +1.3% qoq expansion in the last three months of 2020. That said, the monthly figures for March may show a sharp increase, mainly due to the fast vaccination rollout pace.

The case for a better economic performance during the month of March is also suggested by the forecasts of the industrial and manufacturing productions. Both the yoy rates are expected to have rebounded back into the positive territory. Specifically, they are expected to have surged to +2.8% yoy and 3.8% yoy, from -3.5% and -4.2%.

This is likely to add more credence to the BoE’s decision to scale back the pace of its bond purchases at its latest gathering and may come in line with the Bank’s view that the economy may return to its pre-pandemic size in the last quarter of this year, a quarter earlier than previously thought. With that in mind, GBP-traders may get encouraged to add to their long positions, especially against the US dollar and the Japanese yen, which, as we already noted, we expect to continue underperforming.

As for the rest of Wednesday’s releases, Germany’s final CPIs for April and Eurozone’s industrial production for March are coming out. Germany’s final CPIs are expected to confirm their preliminary estimates, while Eurozone’s IP is anticipated to have rebounded 0.6% mom after deteriorating 1.0% in March.

On Thursday, the only release worth mentioning is Australia’s wage price index for April, which is expected to slow to +1.1% yoy from +1.4%. At last week’s gathering, the RBA said that despite the strong economic recovery in Australia, inflation pressures remain subdued in most parts of the economy and that at the July meeting, they will consider further bond purchases following the completion of the second AUD 100bn purchases in September.

Thus, with wages slowing even further, the chances for more QE by the RBA may increase. This is likely to prove negative for the Aussie, which although is a risk-linked currency, we prefer to avoid for now, even if market sentiment improves further as we expect.

Finally, on Friday, we have the US retail sales for April, the US industrial production for the same month, as well as the preliminary UoM consumer sentiment index for May. Retail sales are expected to have slowed in both headline and core terms, after surging in March, while industrial production is anticipated to have slowed somewhat, to +1.1% mom from +1.4%. The preliminary UoM consumer sentiment index is forecast to have increased to 90.3 from 88.3.