This week will be another one with no central bank decision on the agenda, but we do have the minutes from the latest RBA and FOMC meetings. With central bankers around the globe suggesting that any short-term surge in inflation is likely to prove to be temporary, CPIs from the UK and Canada may also attract special attention.

Monday appears to be a relatively light day in terms of economic releases, with the only one worth mentioning being the New York Empire state manufacturing index for May, which is forecast to have declined slightly, to 23.90 from 26.30.

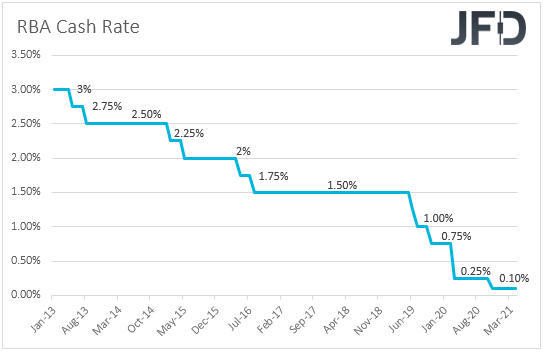

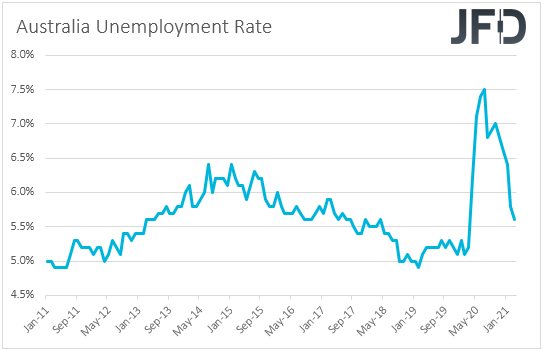

On Tuesday, Asian time, the RBA releases the minutes from its latest monetary policy gathering, at which officials kept policy unchanged, but noted that, despite the strong economic recovery in Australia, inflation pressures remain subdued in most parts of the economy and that at the July gathering, they will consider further bond purchases. With that in mind, we will scan the minutes to see how strong the likelihood for further easing is, but in our view, Wednesday’s wage price index and Thursday’s employment data may prove more determinant on that front, and thereby, bigger market movers for the Australian dollar.

Japan’s preliminary GDP for Q1 is also coming out and the forecast points to a 1.2% qoq contraction after a 2.8% expansion in the last three months of 2020. This will take the yoy rate down to -4.6% from +11.7%.

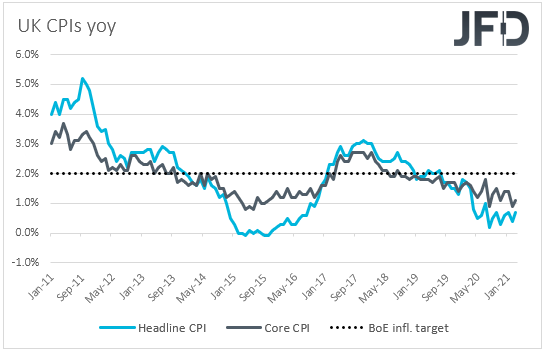

Later, during the early European morning, we have the UK employment report for March. The unemployment rate is expected to have held steady at 4.9%, while the net change in employment is anticipated to show that the UK economy has lost 150k jobs in the three months to March, after losing 73k in the three months to February. Average weekly earnings, both including and excluding bonuses, are expected to have accelerated somewhat. Although more job losses may result in a pullback in the British pound, we believe that its traders may prefer to pay more attention to the inflation data, due out on Wednesday.

From the Eurozone, we get the second GDP estimate for Q1, which is expected to confirm the initial print of -0.6% qoq, as well as the bloc’s employment change for the quarter, for which no forecast is currently available.

In the US, we have the building permits and housing starts, both for April. Building permits are expected to have increases somewhat, but housing starts are forecast to have slightly declined.

On Wednesday, during the Asian morning, Australia’s wage price index for Q1 is due to be released and expectations are for the qoq rate to have ticked down to +0.5% from +0.6%, something that is likely to keep the yoy rate unchanged at +1.4%. As we already noted, at its latest meeting, the RBA said that they could consider further bond purchases at the July meeting, and a small slowdown in wages may add to the chances for something like that taking flesh, especially if we do get a soft employment report on Thursday.

During the early European morning, the UK CPIs for April are due out. The headline rate is forecast to have doubled, to +1.4% yoy from +0.7%, while the core one is anticipated to have ticked up to +1.2% yoy from +1.1%.

At its prior meeting, the BoE decided to scale back the pace of its bond purchases, although it added that monetary policy remains accommodative. Despite officials noting that any spike in inflation is likely to prove to be temporary, combined with last week’s better than expected GDP, IP and MP data, this may add more credence to the Bank’s decision and may help the pound gain further, especially if Friday’s retail sales for April are also on the decent side.

Eurozone’s final CPIs for the month are also coming out, but as it is always the case, they are expected to confirm their preliminary estimates.

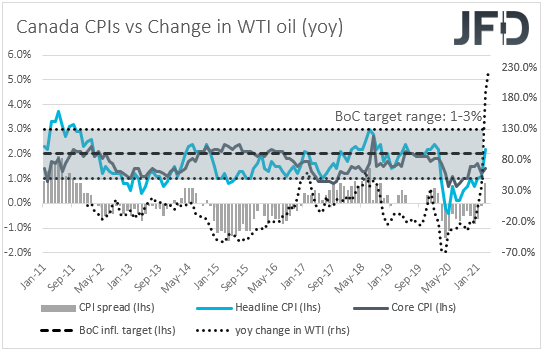

We get more inflation data for April later in the day, this time from Canada. The headline rate is expected to have surged to +3.1% yoy from +2.2%, while no forecast is available for the core rate, neither for the Trimmed mean one. The employment report for the month disappointed, while most policymakers around the globe support that any spikes in inflation this year are likely to prove to be temporary. What’s more, the BoC Governor said last week that the Loonie has strengthened beyond their expectations and that if this continues, it could impact their policy decisions.

Therefore, with all that in mind, we believe that investors may have already started questioning whether the BoC acted correctly at its last gathering, when it scaled back its QE purchases. Thus, we don’t expect a jump in the headline CPI to boost the Loonie much. For that to happen, we may have to see the core and Trimmed mean rates jumping as well, which could mean that the inflation surge is not due to transitory factors after all.

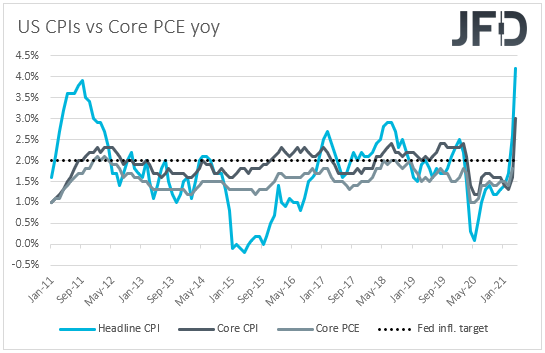

Later in the day, the minutes from the latest FOMC gathering are due to be released. At that gathering, officials kept policy untouched, maintaining their dovish stance. They reiterated the view that any short-term spikes in inflation this year are likely to prove to be temporary, while Fed Chief Powell sticking to his guns, saying that the economy is a “long way” from their goals and that it’s not time to start discussing QE tapering yet.

We will scan the minutes for more details on policymakers’ view, but bearing in mind that inflation skyrocketed more than expected last week, with the core rate surging as well, we will treat the minutes as outdated. Fed officials who spoke after the inflation data appeared slightly more skeptical, with Vice Chair Clarida saying that if inflation proves not to be transitory, they will use their tools to bring it under control.

Therefore, we believe that market participants will focus on what Fed officials have to say after last week’s CPIs. If more of them appear a bit skeptical, the stock market is likely to retrace again, while the US dollar may strengthen. On the other hand, if the consensus among them is still that the inflation spike will prove to be temporary and that it is still too early to start discussing withdrawing policy support, risk appetite is likely to prevail in the market. Equities and other risk-linked assets are likely to gain, while the US dollar and other safe-havens are likely to come under renewed selling interest.

On Thursday, the only top tier data point may be Australia’s employment report for April. The unemployment rate is expected to have held steady at 5.6%, but the employment change is forecast to have slowed to 15k from 70.7k, which, as we already noted, may increase the chances for more QE by the RBA.

Finally, on Friday, during the Asian morning, we have Japan’s National CPIs for April. No forecast is available for the headline rate, while the core one is expected to have ticked down to -0.2% yoy from -0.1%.

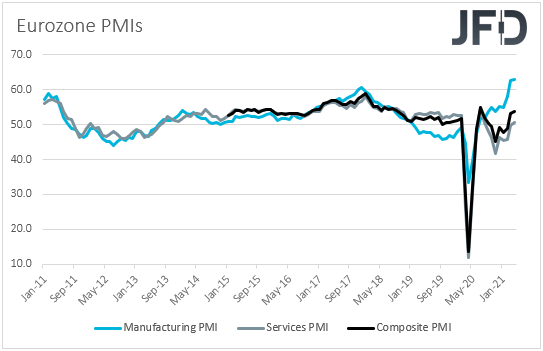

Later, we have the preliminary PMIs for May from the Eurozone, the UK and the US. Eurozone’s manufacturing PMI is anticipated to have slid somewhat, but to have stayed at elevated levels. Specifically, it is expected to have declined to 62.4 from 62.9. The services index is forecast to have increased to 52.0 from 50.5. This is likely to drive the composite index up to 54.9 from 53.8, confirming that, with the vaccinations’ rollout, the Euro-area economy is recovering from the coronavirus pandemic at a decent pace. No forecast is available for the UK prints, while in the US, the manufacturing index is expected to have ticked down to 60.4 from 60.5, and the services one to 64.6 from 64.7.

As for the rest of Friday’s releases, we have the UK retail sales for April, Canada’s retail sales for March, and the US existing home sales for April. The UK retail sales are expected to have slowed somewhat, but to have still increased at a strong rate. Canada’s sales are also expected to have slowed, while the US existing home sales are forecast to have risen.