We don’t have any central bank deciding on monetary policy this week, but that is far from suggesting a quiet week. But, it looks equally important. Both ECB President Christine Lagarde and Fed Chair Powell will deliver testimonies while the RBA releases the minutes of its latest gathering.

We also get inflation data from the UK, Canada, and Japan, which could prove determinant of monetary policy decisions by the BoE, the BoC, and the BoJ. The preliminary PMIs will also come out, giving us a first taste of how the global economy has been faring during June.

On Monday, there are no top-tier data on the economic agenda. Still, there is an event that could attract a decent amount of attention, and that’s the testimony of ECB President Christine Lagarde before the European Parliament in Brussels.

At its latest gathering, the ECB kept all three of its main interest rates untouched but signaled it would hike rates next month, followed by a perhaps bigger increase in September. This added credence to those seeing a 75 bps increase by September, as it could mean a quarter-point hike in July and doubling that in September.

However, Lagarde and her colleagues failed to provide details on how they plan to address the problem of “fragmentation,” which refers to the divergence in the economic state and especially borrowing costs between different Eurozone countries, which raised concerns among the financial community.

The bank held an ad-hoc meeting last week, saying that it would direct cash to more indebted nations from debt maturing and that they would work on a new instrument to prevent an excessive divergence in borrowing costs. ECB President Lagarde said that the ECB’s job is taming inflation and not helping budgets.

So, having all that in mind, we expect Lagarde to confirm market expectations regarding the path of interest rates for the summer. Still, we are very eager to hear any remarks related to “fragmentation.” Will she show more sympathy this time about the periphery, or will she stick to her guns that inflation is the bank’s top priority and not helping budgets? In our view, the first scenario may allow the euro to continue the recovery started today morning, while the second could invite the bears back into action.

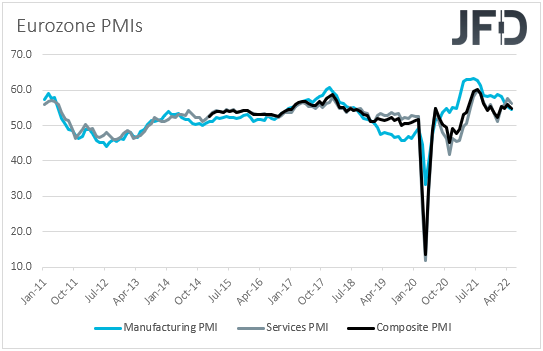

The preliminary PMIs, due out on Thursday, could also affect the euro’s future course of action, as they will provide an early sign of how the economy has been faring during June. Although the market can handle a slight slowdown due to the uncertainty surrounding the war in Ukraine, this may be largely priced in. A larger-than-expected decline could come as a disappointment. Market participants may scale back their hike bets, resulting in a weaker euro.

On Tuesday, investors’ attention is likely to travel to Australia. The RBA meeting minutes and a speech by RBA Governor Lowe are due. At its latest meeting, this bank decided to lift interest rates by 50bps, to 0.85%, against the consensus of 25bps, also noting that inflation is expected to increase further and that they will take further steps in normalizing monetary conditions.

Since then, market participants have lifted their bets regarding the RBA’s future course of action, with the ASX 30-day interbank cash rate futures yield curve suggesting another 12, yes 12, quarter-point increases by the end of the year. In our view, the minutes will reflect the hawkish vibe we got from the meeting statement, so investors and traders may focus more on Lowe’s (NYSE:LOW) more up-to-date remarks.

If he signals that they are willing to take bolder steps in curbing surging inflation, the Aussie is likely to gain. However, we don’t expect this currency to see a long-lasting recovery. Due to its risk-linked status, expectations over further aggressive tightening around the globe, and increasing fears over recessions, could bring it back under selling interest.

Later in the day, we get Canada’s retail sales for April, with expectations pointing to a decent slowdown in both headline and core terms. However, following a hawkish BoC at its last gathering, we don’t believe retail sales could prove a game-changer in monetary policy. Investors may prefer to pay more attention to Canada’s CPI data, due on Wednesday.

On Wednesday, ahead of Canada’s CPIs, we get the UK CPIs for May. The headline rate is expected to have ticked up to +9.1% YoY from 9.0%, but the core one is expected to have slid to +6.0% YoY from +6.2%.

Last week, the BoE hiked interest rates by 25bps as was widely anticipated, enhancing the notion that it will follow a slower rate-hike path than most other major central banks. However, officials said they are ready to act “forcefully” if necessary, with market participants lifting their pricing. They now see interest rates near 3% by year-end, expecting at least 50bps at each September and October meeting.

Accelerating inflation could add credence to that view and may support the pound. However, we are reluctant to call for a trend reversal. The bank warned that the economy may have contracted in the second quarter. Thus, more data revealing an ugly economic picture could prompt market participants to scale back their hike bets, resulting in another round of selling in the British currency.

The PMIs on Thursday may be of those releases. Thus, ahead of the PMIs, we will treat a potential rebound in the pound due to the CPIs as a corrective bounce.

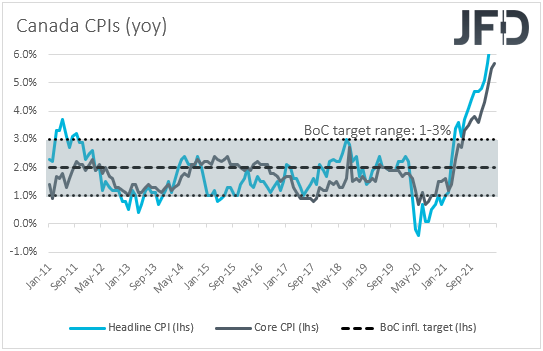

During the European afternoon, as we already noted, we have the Canadian CPIs for May. Headline inflation is expected to have accelerated to +7.5% YoY from +6.8%, but the core rate is anticipated to have declined to 5.4% from 5.7%.

At its latest gathering, the BoC hiked by 50bps, its second double hike in a row, taking its benchmark rate to 1.5%. That said, this was largely anticipated and fully priced in. So, in our view, the most important takeaway from that gathering was that the bank reiterated its willingness to “act more forcefully if needed.”

Thus, accelerating inflation could add credence to that view and help the Loonie gain at the time of the release, even if the core rate declines somewhat. After all, that rate remains well above the 2% midpoint of the bank’s target range of 1-3%.

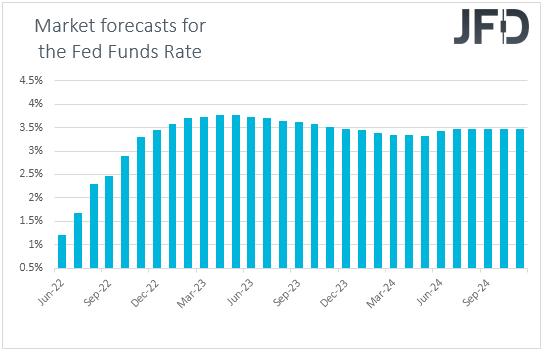

Later in the day, Fed Chair Powell will deliver his semi-annual testimony before Congress. He will deliver the same testimony on Thursday as well. Last week, in line with the market pricing, the Fed raised interest rates by 75bps.

The new dot plot was also very close to the path priced in by the financial community. The median dot for 2022 was at 3.4%, up from 1.9%, which implies another 175bps by the end of the year. In other words, the market has been pricing in another triple hike in July and two more doubles after that.

However, at the press conference following the decision, Chair Powell said that they might hike either by 50 or 75 bps at the next meeting, depending on incoming data. In our view, this meant that a 75bps liftoff is not a done deal as the market pricing has been suggesting.

Thus, with that in mind, we will monitor his testimony for hints and clues as to how likely a 75bps hike is at the next meeting. The dollar could strengthen if he appears more confident about another triple hike, while the opposite may be true if he keeps highlighting the probability that 50bps could also be the case.

On Thursday, the spotlight will likely turn to the preliminary PMIs for June from the Eurozone, the UK, and the US. In the Eurozone, the manufacturing and services PMIs are expected to have declined somewhat, taking the composite index down to 54.0 from 54.8.

As we already noted, we don’t expect this to hurt the euro much, as it may already be largely priced. However, a deeper slide could prompt EUR traders to adjust their bets about the ECB’s future course of action.

In the UK, there are no forecasts available for now. Still, similarly to the Eurozone, decent declines could increase concerns over a recession and thereby prompt participants to price out some BoE hikes. The result could be a depreciating pound.

Later in the day, in the US, the manufacturing PMI is forecast to have slid fractionally, but the services index is expected to have increased. We don’t believe that the US indices will attract the same attention as those of the Eurozone and the UK, as USD-trader may have their gaze locked on Fed Chair Powell’s testimony.

On Friday, we get more CPIs for May, this time from Japan. There is no forecast for the National headline rate, but the core rate is forecast to have held steady at +2.1% YoY. Although this is above the BoJ’s objective of 2%, it is still the lowest among the major economies. Thus, we don’t believe it will tempt BoJ policymakers to alter their ultra-loose policy very soon.

After all, they kept all their tools untouched at the last gathering, when the core rate was already at 2.1%. A few hours later, we have the UK retail sales for May, with both the headline and core monthly rates expected to dive into the negative territory, adding to concerns over the UK economy falling into recession.