We have a very busy week ahead of us, with not one, not two, but five central bank decisions on the agenda.

The Fed is expected to drop the “transitory” wording from its policy statement and perhaps signal a faster tapering process, while the ECB could announce that the PEPP will end in March, but perhaps compensate via other schemes.

The BoE will probably refrain from hiking rates, and the SNB could strengthen its threats with regards to FX intervention. As for the BoJ, we expect it to pass once again unnoticed.

Monday appears to be a relatively light day with no major events or indicators on the agenda.

On Tuesday, the only releases worth mentioning are the UK employment report for October and the US PPIs for November. The unemployment rate in the UK is expected to have ticked down to 4.2% from 4.3%, but the employment change is forecast to show that the economy has gained less jobs in the three months to October, than it did in the three months to September.

Average weekly earnings, both including and excluding bonuses, are forecast to have slowed, which could mean that UK inflation could top as well in the months to come. In any case, we don’t expect pound traders to pay much attention to this release, as they may prefer to avoid committing to large positions ahead of Thursday’s BoE decision. As for the US data, similarly to the CPIs, both the headline and core PPI rates are expected to have drift further north.

On Wednesday, the calendar gets heavier, with the main event on the agenda being the FOMC interest rate decision. A couple of weeks ago, Fed Chair Jerome Powell appeared hawkish before the US Congress, surprising those expecting him to adopt a more cautious stance due to the new coronavirus variant and the restrictive measures adopted around the globe.

In contrast, the Fed Chief said that the “transitory” wording with regards to inflation may have to be dropped out of the Fed’s monetary policy statement, and that QE tapering should end sooner than previously estimated.

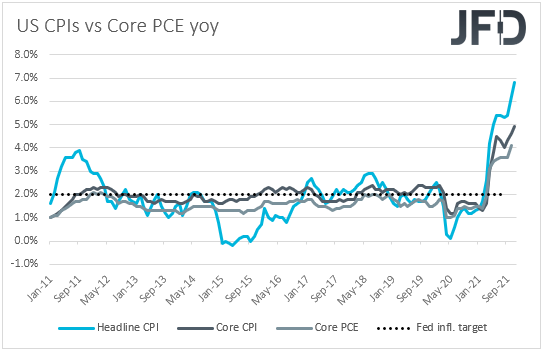

Despite nonfarm payrolls for November missing expectations, the unemployment rate declined even more, to 4.2% from 4.6%, which combined with further acceleration in the CPIs on Friday, suggests that indeed the Fed could appear more hawkish this time around.

That said, removing the “transitory” wording and announcing a faster tapering pace is what the financial community may have been already anticipating. Therefore, such decisions by themselves are unlikely to result in high market volatility. Thus, we expect investors to pay extra attention to the updated economic projections and the new “dot plot”.

If officials are also in favor of faster rate hikes as well, then the US dollar could keep drifting north, but how equities will react is not straight forward. With market participants turning somewhat skeptical again with regards to the future performance of the global economy, stocks could be sold on speculation that higher borrowing costs sooner could hurt companies’ profitability. However, because they may have digested the idea to some extent, we don’t expect a large and extended fall.

As for Wednesday’s data releases, during the Asian morning, we have China’s fixed asset investment, industrial production, and retail sales, all for November, while during the early EU session, the UK CPIs are forecast to have accelerated further.

That said, we don’t believe that they will prove a game changer with regards to Thursday’s BoE decision, as the main focus recently has been the increasing COVID cases and the new restrictive measures.

Later in the day, but still ahead of the FOMC decision, we get the US retail sales for November and the Canadian CPIs for the month. Both headline and core sales are forecast to have slowed, while Canada’s headline CPI rate is forecast to have held steady at +4.7% yoy. No forecast is available for the core rate.

On Thursday, the central bank torch will be passed to the SNB, the BoE and the ECB.

Getting the ball rolling with the SNB, meetings of this Bank have been passing unnoticed for several months now. However, things may be different this time around, as concerns how the new COVID-related restrictions can affect European growth have pushed EUR/CHF lower, near the 1.0400 zone.

With SNB officials maintaining the view that the franc remains highly valued, even when EUR/CHF was at higher levels, we see decent chances for them to strengthen their wording about intervening in the FX market to prevent the pair for moving lower.

Now, passing the ball to the BoE, we believe that all the attention will fall on interest rates. Following the outbreak of a new COVID variant, and the new restrictions in the UK, market participants have pushed drastically back their expectations with regards to a rate hike at this gathering.

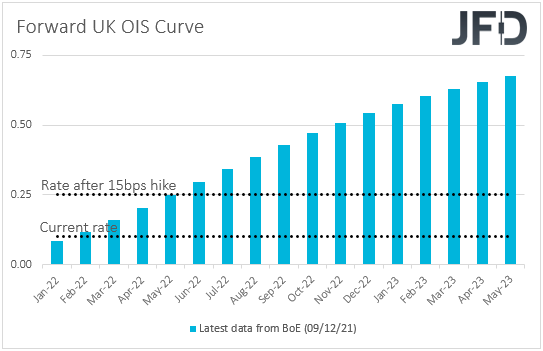

The latest available data of the UK OIS (Overnight Index Swaps) suggest that a hike to 0.25% is fully priced in for May 2022. We don’t believe that policymakers will surprise the financial community by hiking this week, and therefore, it will be interesting to see what they have to say for their future course of action.

Hints that they could lift rates sooner than when the market pricing suggests could result in a rebound in the British pound. The opposite could be true in case they sound more hesitant.

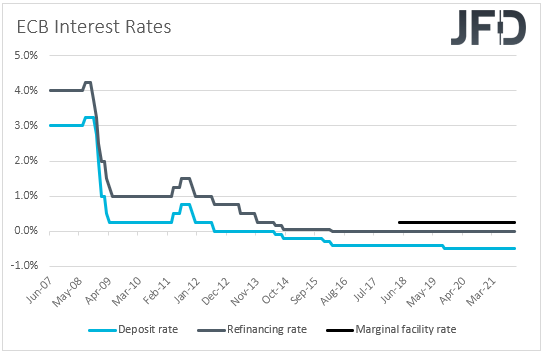

A few minutes after the BoE, we have the ECB. No monetary policy action is expected by this Bank, but it would be interesting to see what they are planning to do moving forward in the midst of fresh lockdowns, but also accelerating inflation in the euro area.

Officials are expected to announce that PEPP (Pandemic Emergency Purchase Program) will end in March, so, it will be interesting to see whether they are willing to compensate through other schemes, like the APP (Asset Purchase Program). Something like that, combined with more warnings that interest rates are unlikely to start rising anytime soon, could result in another round of selling in the euro.

Besides those three central banks, we also have several top-tier data releases on the agenda, like the New Zealand GDP for Q3 and Australia’s employment report for November during the Asian session. Later in the day, we get the preliminary manufacturing and services PMIs from the Eurozone (manufacturing, services) the UK (manufacturing, services) and the US (manufacturing, services). The US industrial production for November is also due out.

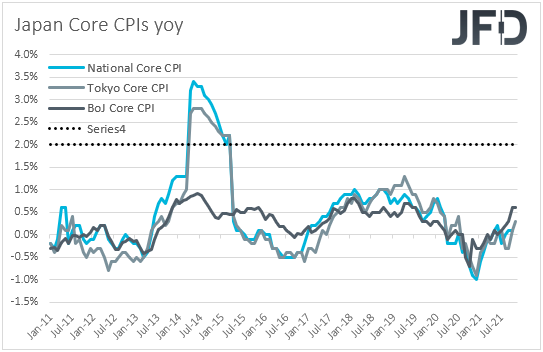

Finally, on Friday, the central bank torch will be passed to the BoJ. With Japanese inflation near zero, well below the Bank’s target of 2%, we don’t expect any material changes, neither to the actual policy measures nor to the language in the accompanying statement. Once again, the yen may not react to the outcome and stay driven by developments surrounding the broader market sentiment.