The main spotlight will fall this week on ECB’s Financial Stability Review, which will be released on Wednesday and on the FOMC meeting minutes, also delivered on the same day. We will also get the PCE index figures from the US, which will be carefully monitored by the Fed. Sweden and Norway will also deliver key data sets, which will attract attention.

Monday will be a relatively quiet day in terms of economic data releases. Japan will be closed because of the Workers Day celebration. The eurozone will release their manufacturing and services PMIs for the month of November. If the manufacturing figure is believed to have declined from 54.8 to 53.1, the services reading is forecasted to show up on a slightly better side, rising fractionally from 46.9 to 47. If the readings come out as expected, this might not be good for the euro, as manufacturing PMI would show a decline and the services PMI would stay in contraction territory.

UK will deliver its preliminary composite PMI reading. There is currently no forecast available, however the previous figure was at 52.1 and it has been declining since September. US will also present its final manufacturing and services PMIs for the month of November. The manufacturing one is expected to have stayed the same, at 53.4, but the services number is believed to have dropped from 56.9 to 54.6. We don’t expect the US dollar to get affected too much, unless the actual readings come out far from the forecasts.

Tuesday will start off with Germany releasing its QoQ and YoY final GDP figures for Q3. If we take a look at the flash reading of Germany’s QoQ GDP figure released in the end of October, that number not only has beaten the previous -9.8%, but also the initial optimistic forecast of +7.3%. For now it is believed that the final figure will show up at -10.1%, which may be disappoint some investors and especially euro-bulls, as it may hurt the common currency. The final YoY GDP number is also believed to come out in the negative territory, at -11.7%, whereas the forecast sits at only -4.1%.

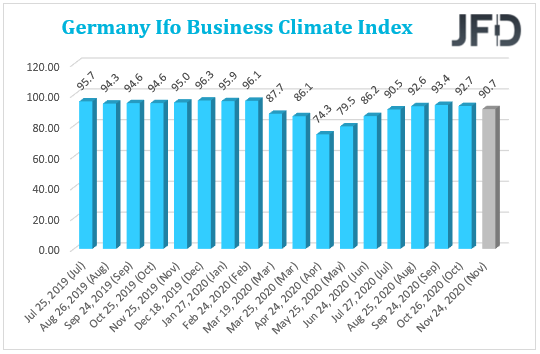

Germany will also deliver its Ifo business climate index number. So far, the forecast sits at 93.0, which is slightly above the previous reading of 92.7.

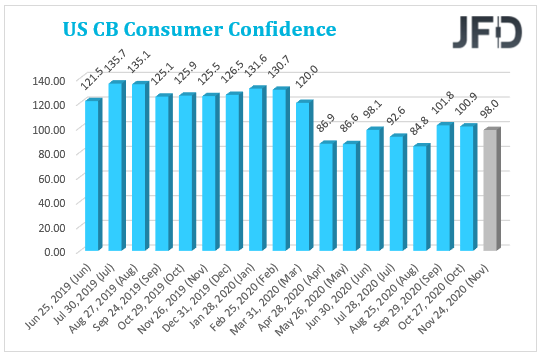

The US will post their CB consumer confidence number for the month of November, however that one is expected to be on the lower side, going from the previous 100.9 to 98.0. Certainly, this is not something that investors would like to see going further into the holiday season.

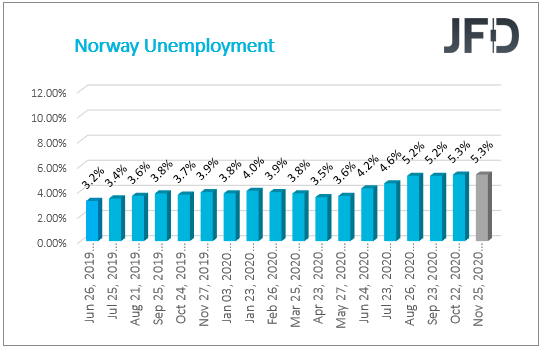

Wednesday will be quite a busy day in relation to economic data releases. The day will start off with the Norwegian unemployment number, which is expected to have remained the same, at 5.3%. If so, we may expect the Norwegian krone to stay unchanged against its major counterparts, such as the euro and the US dollar, however NOK could remain a bit more vulnerable to the developments in the oil market instead.

Later on, the ECB will deliver its Financial Stability Review, in order show what it and other eurozone central banks think about the current state of the financial system. The report is aimed to promote awareness of the European financial industry and show the issues that surround it at the moment. In the previous review, which was delivered in May, the ECB stated that: “The spread of the coronavirus (COVID-19) triggered abrupt shifts in asset prices and led to an increase in financial system stress”. It also said that: “The coronavirus pandemic has affected virtually all aspects of economic activity, at times interacting with pre-existing financial vulnerabilities. Even if temporary, there will be a significant contraction in euro area economic activity this year”. We do not expect the euro to react much to the report.

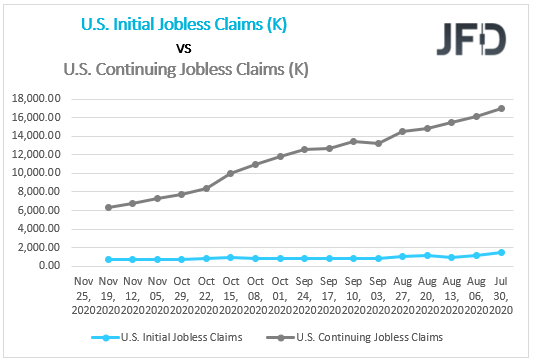

Before the start of the US session, we will receive some economic data from the US. Initial and continuing jobless claims for the past week will be released. There is currently no forecast for the continuing jobless claims number, but initial one is believed to have improved slightly, going from 742k to 730k. Also, the US will release its preliminary Q3 QoQ GDP figure, which is expected to have stayed the same as previous, at +33.1%. If so, the US dollar could stay focused on the other US datasets, which will fall under the spotlight, and that’s the core and headline PCE rates for the month of October. There are no forecasts for the headline MoM and YoY PCE figures, however the core ones are believed to have ticked down by a tenth of a percent. The MoM number is expected to slide from +0.2% to +0.1% and the YoY one is believed to have fallen from +1.5% to +1.4%. Certainly, if the actual figures move even below the initial forecasts, this is not something that the Federal Reserve would like to see. The Fed uses the PCE index, when making their monetary policy decisions. And given that the FOMC has set a target to bring inflation slightly above 2%, in order to have longer term inflation near the average of 2%. If the actual PCE figures come out below forecast, that might have a negative effect on USD.

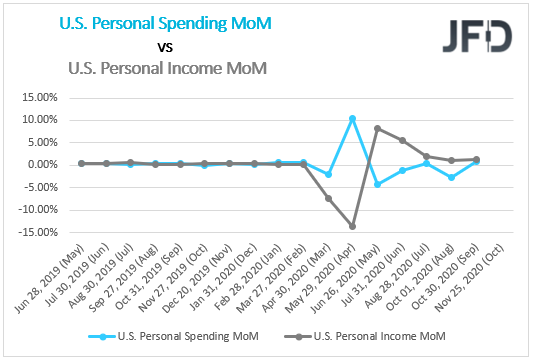

US will also deliver the consumer personal income and spending numbers for the month of October on a MoM basis. So far, the forecasts sit on the lower side. Personal income is believed to have gone down from +0.9% to +0.1% and personal spending is expected to drop from +1.4% to +0.3%. If that’s the case. This may create a risk-off environment in the market.

Later on, we will get the minutes from the last FOMC meeting. Investors will try to seek clarity on how policymakers are willing to proceed further. During the previous meeting, the Fed decided to take a wait-and-see approach, because of the uncertainty surrounding the US elections. The Committee had state last time that they are ready to use all available tools to support the US economy.

On Thursday, the US will be closed due to Thanksgiving celebration.

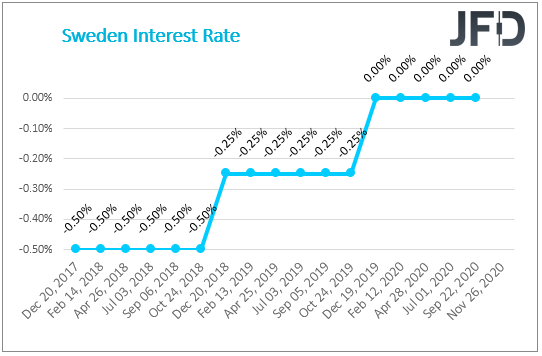

During the early hours of the European morning on Thursday, the Swedish central bank will take center stage, as it will deliver its interest rate decision. In the latest monetary policy report delivered by the Riksbank, it states that the Swedish economy has managed to recover somewhat after the sharp decline experienced in spring of this year. The Bank will continue providing support to the economy and it is believed that the repo rate will stay the same, at 0.0%.

Later on, the ECB will publish its account of monetary policy meeting minutes from its October meeting, which might show further monetary easing, in order to continue supporting the eurozone.

On Friday, the US will be open, but will close earlier, due to the continued celebration of Thanksgiving.

During the early hours of the Asian morning on Friday, Japan will deliver the Tokyo core and headline CPI figures on a YoY basis for the month of November. There is currently no available forecast for the headline number, but is expected that the core will come out on the lower side from the -0.5%, at -0.7%. We don’t expect much movement in the Japanese yen, as the currency might stay vulnerable to the broader market sentiment.

Sweden is set to release its QoQ and YoY GDP figures for Q3. The current forecast of the actual numbers is for an improvement. The YoY figure is expected to move from -7.7% to -3.7%, whereas the QoQ reading is believed to get back into positive territory, going from -8.3% to +4.4%.

Sweden’ neighbour, Norway, will release its non-seasonally adjusted unemployment figure for the month of November. The forecast is currently sitting at 4.0%. If that’s the case and the actual figure shows up as expected, this could be a disappointment for the Norwegian economy, which is considered one of the stronger ones in the world, because the previous reading was at 3.5%. The NOK may take a slight beating against its major counterparts, if the actual number comes out as forecasted, or even higher.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Weekly Outlook: ECB Stability Review, FOMC Minutes, PCE Index

Published 11/23/2020, 05:06 AM

Updated 07/09/2023, 06:31 AM

Weekly Outlook: ECB Stability Review, FOMC Minutes, PCE Index

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.