Following last week’s RBNZ monetary policy decision, this week, the central bank torch will be passed to the BoC and the ECB, with market participants eager to find out whether these banks are indeed considering scaling back their QE purchases, with the former possible to proceed with a reduction as early as at this gathering. We also get a bunch of UK data, including inflation, retail sales and PMIs, as well as New Zealand’s CPIs for Q1.

Monday is a relatively quiet day, with the only releases worth mentioning being Japan’s trade balance for March, which is already out, and Canada’s housing starts for the same month, due to be released later in the day. Both Japan’s exports and imports came in better than expected, with the nation’s trade surplus rising to JPY 663.7bn from JPY 215.9bn. Canada’s housing starts are anticipated to have risen somewhat.

On Tuesday, during the Asian morning, the RBA releases the minutes from its latest monetary policy decision, when it kept its policy unchanged, repeating that the economic recovery in Australia is well underway and that it is stronger than had been expected. Therefore, we will scan the minutes for clues as to whether this has diminished even further the chances for additional easing in the foreseeable future, and whether some members have already started thinking about normalization.

Later in the day, during the early EU session, the UK employment report for February is coming out. The unemployment rate is expected to have ticked up to 5.1% from 5.0%, while the net change in employment is forecast to show that the economy has lost 167k jobs in the three months to February, more than the prior 147k. With regards to wage growth, both the including and excluding bonuses rates are forecast to have held steady at +4.8% yoy and +4.2% yoy respectively.

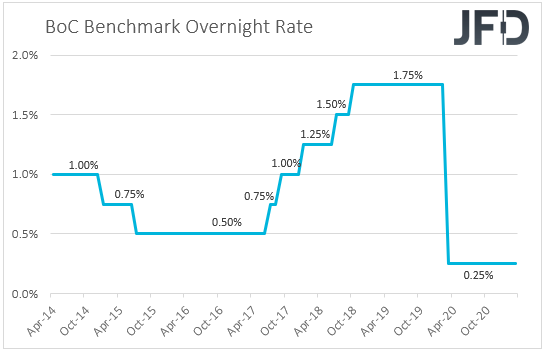

On Wednesday, the main event on the economic agenda may be the Bank of Canada interest rate decision. Last time, the Bank kept its monetary policy settings unchanged and noted that the economic recovery continues to require extraordinary monetary policy support, until economic slack is absorbed so that the 2% inflation goal is sustainably achieved.

According to the Bank’s January projections, this is not expected to happen until into 2023. The Canadian dollar slid somewhat at the time of the release, but was quick to recover those losses as officials reiterated that as they continue “to gain confidence in the strength of the recovery, the pace of net purchases of Government of Canada bonds will be adjusted as required”, something that may have kept the door for a QE tapering open.

Since then, GDP data showed that the Canadian economy expanded by more than anticipated in January, while the employment data revealed a notable drop in the unemployment rate in the last couple of months, and very strong employment gains. On top of that, ahead of the meeting, Canada’s inflation data is expected to show that the headline CPI rate jumped to +2.3% yoy from +1.1%, although this will be seen by many as temporary.

With all that in mind, it would be interesting to see whether and how policymakers will adjust their policy. Although interest rates are largely expected to stay untouched, we would like to see whether they will eventually decide to taper their QE purchases. After all, the Bank currently owns already nearly 40% of all government bonds, and Governor Macklem has clearly said that if this number surpasses 50%, market functioning could be distorted.

As for the Canadian dollar, scaling back bond purchases could prove positive. Combined with potentially further improvement in the broader market sentiment and further gains in oil prices, monetary policy is likely to be an extra boost on the Loonie’s way higher. However, in order to be on a safer side, we would like to exploit any further CAD-gains against the safe-havens, like the yen, which we expect to stay under selling interest due to an increasing risk appetite.

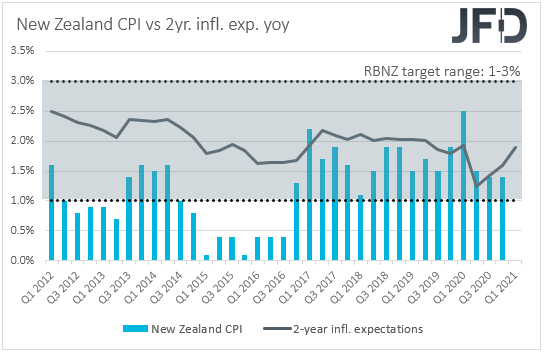

As for Wednesday’s data, during the Asian session, we get New Zealand’s CPIs for Q1. The qoq rate is forecast to have risen to +0.7% from +0.5%, but this is likely to keep the yoy one unchanged at +1.4%. At last week’s gathering, the RBNZ kept its policy settings untouched, staying prepared to lower the OCR further if required and adding that a prolonged period of time is most likely to pass before their objectives are met. An unchanged yoy inflation rate is likely to add more credence to the Bank’s view and is likely to allow officials to remain ready to cut interest rates if deemed necessary.

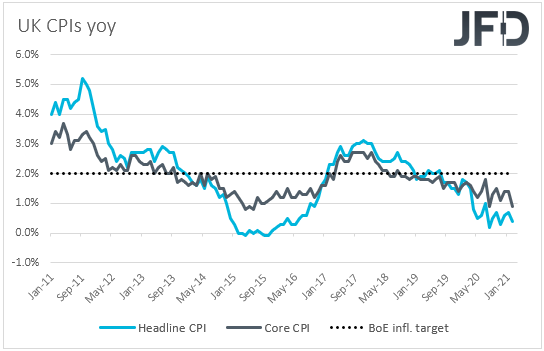

We get more CPI data later in the day, this time from the UK. The headline rate is expected to have risen to +0.7% yoy from +0.4%, while the core one is forecast to have ticked up to +1.0% yoy from +0.9%. At the prior BoE gathering, policymakers kept their policy unchanged and noted that the recent plans for easing of covid-related restrictions may be consistent with a slightly stronger outlook for consumption growth.

However, they repeated that the outlook for the economy remains unusually uncertain and that if the inflation outlook weakens, they stand ready to take the necessary action. Thus, with both the headline and core CPI rates well below the Bank’s objective of 2%, we don’t believe that officials will alter their stance any time soon.

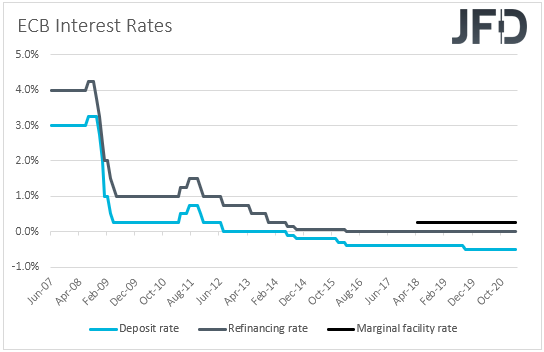

On Thursday, the central bank torch will be passed to the ECB. At its latest meeting, this Bank decided to accelerate its Pandemic Emergency Purchase Program in order to stop any unwarranted rise in bond yields. Although other major central banks share the view that the latest rise in bond yields around the globe just represents a healthy economic recovery, that’s not the case for the ECB. Rising bond yields in Europe have partly spilled over from US markets reacting to President Biden’s massive fiscal stimulus.

That said, PMIs since then suggested that the Euro-area economy is on a recovery mode, while inflation rose. Although several Eurozone nations are still in lockdowns, and despite ECB President Lagarde noting that any rise in inflation is likely to be temporary, the minutes of the last meeting revealed that officials discussed the idea of reducing the pace of PEPP purchases in the future.

Thus, it would be interesting to see whether they will signal something like that at this meeting, or whether they will stay ready to ease further if deemed necessary. With government bond yields around the globe pulling back recently, we would see the former case as the more likely one, and if indeed this is the case, the euro is likely to continue strengthening.

As for the data, the only one worth mentioning is the US existing home sales for March, which are expected to have rebounded 0.9% mom, after slumping 6.6% in February.

Finally, on Friday, during the Asian session, Japan’s National CPIs for March are coming out. No forecast is available for the headline rate, but the core one is expected to have risen to -0.1% yoy from -0.4%.

During the early EU morning, the UK retail sales for March are due to be released. Both the headline and core sales are forecast to have slowed to +1.5% mom and +1.3% mom from +2.1% and +2.4%. Following the latest safety concerns with regards to the AstraZeneca (NASDAQ:AZN) coronavirus vaccine, which may have slowed the rollout in the UK, slowing retail sales may raise questions with regards to the BoE’s view that consumption growth is likely to strengthen. This, combined with potentially subdued inflation on Wednesday, and a retreat in the April PMIs, due out later in the day, may allow traders to continue selling the British currency for a while more.

Apart from the preliminary UK PMIs, for which no forecast is available, we get the preliminary prints from the Eurozone and the US as well. Eurozone’s manufacturing and services indices are expected to have pulled back to 62.0 and 49.1, from 62.5 and 49.6 respectively, something that would take the composite PMI down to 52.8 from 53.2. In the US, both the manufacturing and services PMIs are likely to rise to 60.5 and 61.7, from 59.1 60.4, confirming that the world’s largest economy is recovering from the damages of the coronavirus pandemic at a faster pace than other nations.