U.S. economy adds 64,000 jobs in November, delayed BLS data shows

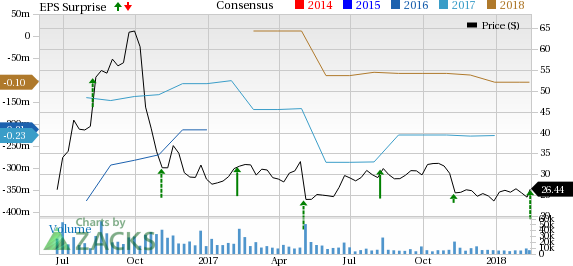

Shares of Twilio Inc. (NYSE:TWLO) jumped more than 6% during yesterday’s after-hours trade after the company reported splendid fourth-quarter results, wherein its revenues topped the Zacks Consensus Estimate as well as management’s guidance range. Also, the top line marked solid year-over-year growth.

Talking about the company’s bottom-line results, though it posted a loss per share, the figure was much lower than the consensus estimate and management’s guidance range as well. However, it has an unfavorable comparison when compared with the year-ago quarter results.

Let’s discuss the fourth-quarter results in detail.

Revenues

The company’s fourth-quarter revenues surged 40.6% year over year to $115.2 million and surpassed the Zacks Consensus Estimate of $104 million. Also, it came ahead of management’s previously guided range of $102.5-$104.5 million. Furthermore, the company’s base revenues jumped 40% year over year to $105.3 million.

The robust top-line performance was mainly driven by remarkable year-over-year growth in active customer account which was a result of the company’s continued focus on introducing products as well as its go-to-market sales strategy.

The company registered a whopping 33.8% surge in active customer accounts, adding more than 12,373 accounts over the last 12 months, bringing the total count to 48,979 as of Dec 31, 2017. During the fourth quarter alone, Twilio added more than 2,490 active customer accounts.

Operating Results

Non-GAAP gross profit climbed approximately 27.5% year over year to $61.6 million. However, gross margin contracted 550 basis points (bps) to 53.5%, as elevated cost of goods sold more than offset the benefit of higher revenues.

Non-GAAP operating expenses flared up 35.8% year over year to $65.5 million. The year-over-year surge was mainly due to increased investment in research and development, and sales to capitalize on the market opportunity. However, as a percentage of revenues, the figure decreased to 56.9% from 58.9% in the year-ago quarter.

Furthermore, the company reported non-GAAP operating loss of $3.9 million. In the year-ago quarter, Twilio had posted an operating income of $80,000. Non-GAAP net loss came in at $2.6 million or 3 cents per share. In the year-ago quarter, the company had reported net income of $0.3 million or almost breakeven earnings per share. The year-over-year widened loss was mainly due to elevated costs and operating expenses which more than offset the benefit of sturdy top-line growth.

Nevertheless, non-GAAP loss per share came way below management’s guided range of a loss of 5-6 cents. Also, the quarterly loss was narrower than the Zacks Consensus Estimate of a loss of 6.

Twilio Inc. Price, Consensus and EPS Surprise

Balance Sheet

The company exited the reported quarter with cash and cash equivalents of $290.9 million, slightly up from $283.9 million at the end of the previous quarter. In addition to this, during the year, the company used $3.3 million worth of cash for operational activities.

Outlook

Buoyed by a solid quarterly performance, Twilio provided encouraging outlook for the first quarter and full-year 2018.

For the first quarter, Twilio estimates revenues to be between $115 million and $117 million (mid-point $116 million). This is higher than the Zacks Consensus Estimate of $107.6 million. Base revenues are anticipated in the range of $108-$109 million. Non-GAAP net loss is projected to lie in the 6-7 cents per share band. The consensus estimate is currently pegged at a loss of 5 cents.

For the full year, Twilio expects revenues to lie between $5016 million and $514 million (mid-point $510 million). This is significantly higher than the Zacks Consensus Estimate of $476.4 million.

Similarly, base revenues are estimated in the range of $356.5-$357.5 million, higher than the previous forecast of $483-$487 million. Non-GAAP net loss is projected to come in the range of 10-14 cents. The Zacks Consensus Estimate is pegged at a loss of 11 cents.

Recovers from Uber Hangover

The recently-reported strong quarterly results clearly indicate that the company has been able to mitigate the loss of revenues from Uber.

It should be noted that Uber uses Twilio services for a variety of used cases such as driver and rider communication, driver marketing and several others. Till 2016, Uber used Twilio’s platforms in most of its geographical operations. However, since first-quarter 2017, Uber is “optimizing by used case and by geography” and is planning to "move communications for some use cases in-app." This means that Uber is now trying to operate its messaging services internally.

Uber’s contribution to Twilio’s revenues declined to approximately 5% in the fourth quarter from roughly 17% in the year-ago quarter.

Despite this, the company managed to report robust revenue growth in back-to-back three quarters, returning itself once again on growth trajectory mainly due to its sustained focus on rolling out products, global expansion, go-to-market sales and acquisition strategies.

Our Take

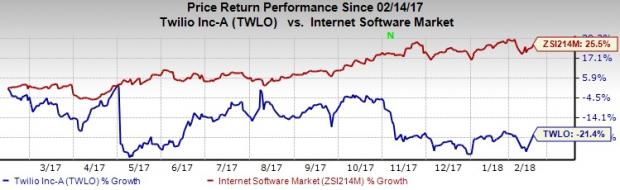

We believe back-to-back impressive quarterly results and optimistic guidance will give a fresh boost to the company’s share price which is currently trading below 24% to its 52-week high level of $34.74.

Notably, Twilio’s shares have underperformed the industry to which it belongs to over the past year. The stock has depreciated 21.4% during the said period, while the industry recorded growth of 25.5%.

Nonetheless, the company’s key initiatives, including product innovation, global expansion and acquisitions, are helping it gain customers, which bode well for long-term growth. We believe proliferation in cloud and mobile penetration across the globe will continue to fuel Twilio’s customer growth over the long run.

Twilio boasts a strong clientele that includes the likes of Netflix (NASDAQ:NFLX) , salesforce.com (NYSE:CRM) and Twitter among others. Furthermore, the long-standing relationship with Amazon (NASDAQ:AMZN) is particularly noticeable. Twilio uses Amazon Web Service (AWS) to host its platform.

Nevertheless, intensifying competition in the communications market and growing prevalence of in-app push notifications are major concerns. Moreover, customer concentration is a headwind.

Currently, Twilio carries a Zacks Rank #3 (Hold). You can see the complete list of today’s Zacks #1 Rank (Strong Buy) stocks here.

Don’t Even Think About Buying Bitcoin Until You Read This

The most popular cryptocurrency skyrocketed last year, giving some investors the chance to bank 20X returns or even more. Those gains, however, came with serious volatility and risk. Bitcoin sank 25% or more 3 times in 2017.

Zacks’ has just released a new Special Report to help readers capitalize on the explosive profit potential of Bitcoin and the other cryptocurrencies with significantly less volatility than buying them directly.

See 4 crypto-related stocks now >>

Amazon.com, Inc. (AMZN): Free Stock Analysis Report

Netflix, Inc. (NFLX): Free Stock Analysis Report

Twilio Inc. (TWLO): Free Stock Analysis Report

Salesforce.com Inc (CRM): Free Stock Analysis Report

Original post