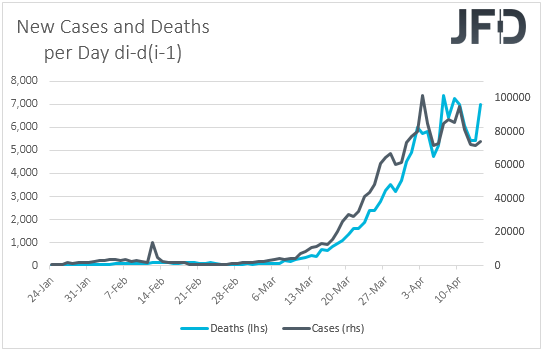

Major EU and U.S. indices continued trading in the green yesterday, but Asian bourses traded mixed today, as the reported numbers of new infected cases and deaths worldwide revealed an acceleration again. As for today, apart from headlines surrounding the virus saga, investors may also pay attention to the BoC monetary policy decision. Tonight, the most important release may be Australia’s employment report for March.

RISK APPETITE EASES AS VIRUS ACCELERATES AGAIN

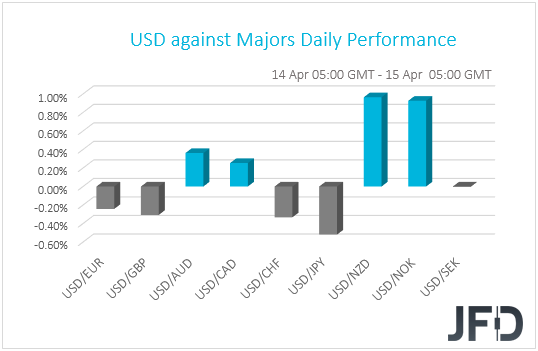

The dollar traded mixed against the other G10 currencies on Tuesday and during the Asian morning Wednesday. It gained against NZD, NOK, AUD and CAD in that order, while it underperformed versus JPY, CHF, GBP, and EUR. The greenback was found virtually unchanged against SEK.

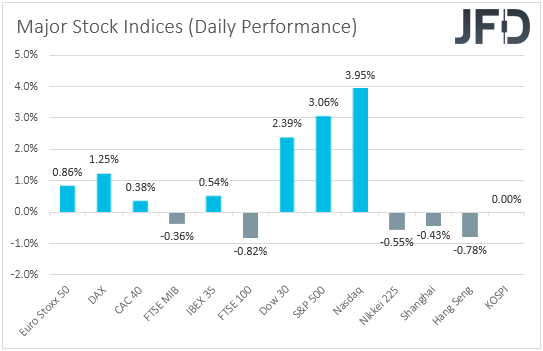

The weakening of the risk-linked Aussie and Kiwi, as well as the slide in the oil-related CAD and NOK, combined with the strengthening of the safe havens yen and franc, suggest that risk appetite eased at some point. Indeed, although major EU and US indices closed in green territory, Asian bourses were mixed, with both Japan’s Nikkei 225 and China’s Shanghai Composite sliding 0.55% and 0.43% respectively.

EU and U.S. markets may have remained supported due to prior signs that the coronavirus pandemic may be slowing down, which could result in the removal of some restrictive measures around the globe. Yesterday, White House adviser Larry Kudlow said that President Trump will proceed with a statement about reopening the U.S. economy in the next couple of days, adding to hopes that this health crisis may be ebbing.

That said, investors got a reality check during the Asia trading, as the reported numbers of new infected cases and deaths worldwide revealed an acceleration again, with the number of deaths nearing its daily record.

Remember, yesterday we noted that just a day of new records may be enough to revive fears and trigger another round of risk aversion, and the overnight reaction adds more credence to our view. We believe that it is too early for governments to reopen their economies and if they do so, we believe that it must be a slow procedure in order to avoid a new flare up. Having all that in mind, we stick to our guns that we would prefer not to trust a long-lasting recovery in the broader market sentiment. Even if equities rebound again, we prefer to take things day by day.

EURO STOXX 50 -TECHNICAL OUTLOOK

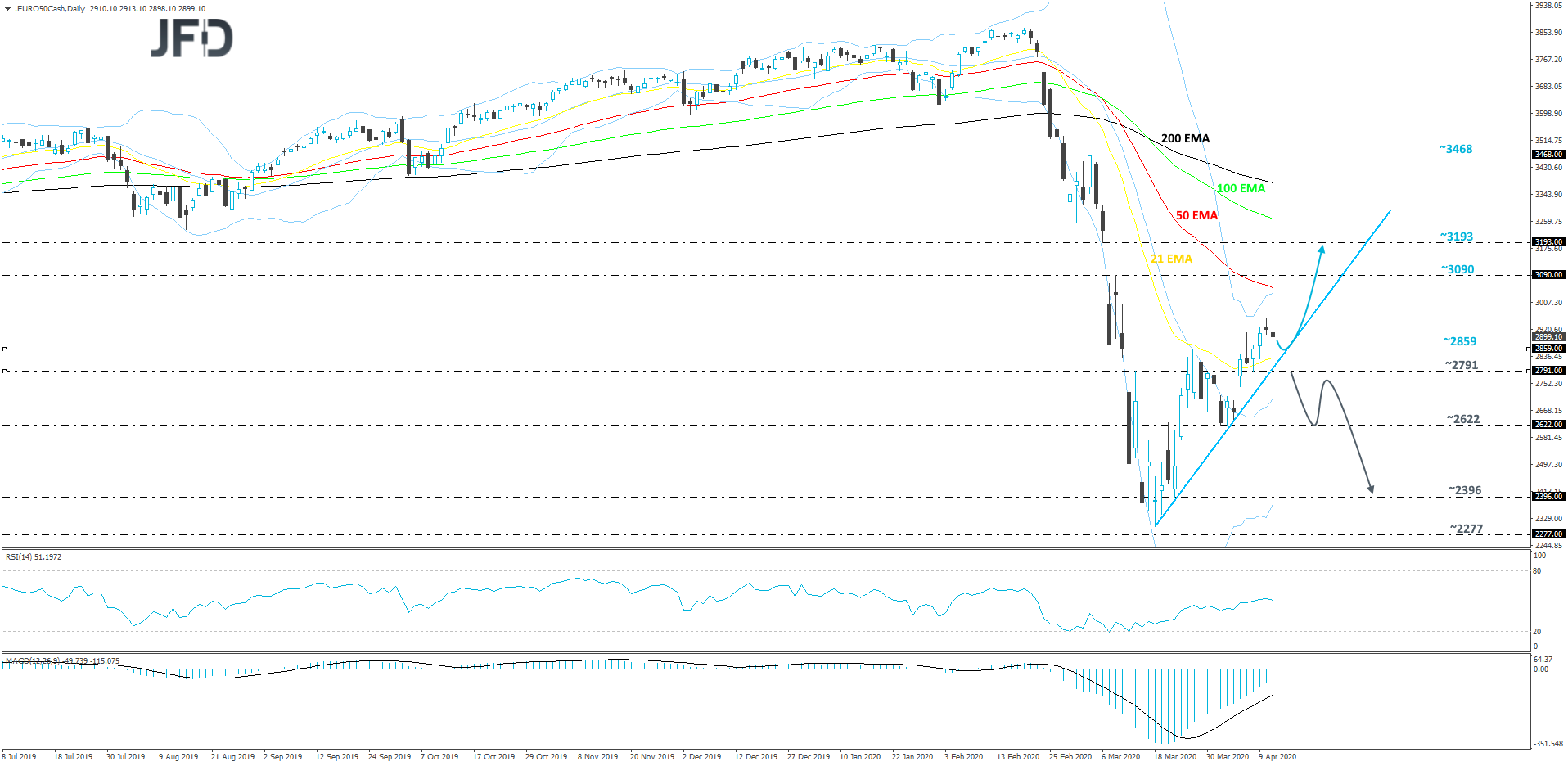

The Euro Stoxx 50 index is still slowly grinding higher and recovering some of its losses made between mid-February and mid-March. Now the price is seen balancing above a short-term tentative upside support line taken from the low of March 18th. As long as the index remains above that upside line, we will stay somewhat positive and aim for slightly higher areas.

After breaking one of its key resistance barriers, at 2859, the Euro Stoxx 50 moved a bit higher, but this morning we are seeing a small decline again. That said, if the index remains above, either the 2859 zone, or the aforementioned upside line, we will stay somewhat positive, at least for the near term. If the bulls decide to take advantage of the lower price, it may rise all the way to the 3090 barrier, marked by the high of March 10th. Slightly above it lies another possible resistance zone, at 3193, which is the low of March 6th.

On the other hand, if the previously-mentioned upside line breaks and the price slides below the 2791 hurdle, which is the low of April 8th, this may open the door for further declines. The index might then travel to the 2622 obstacle, a break of which could set the stage for a move to the 2396 level, marked by the low of March 23rd.

WILL THE BOC EXPAND ITS QE PURCHASES?

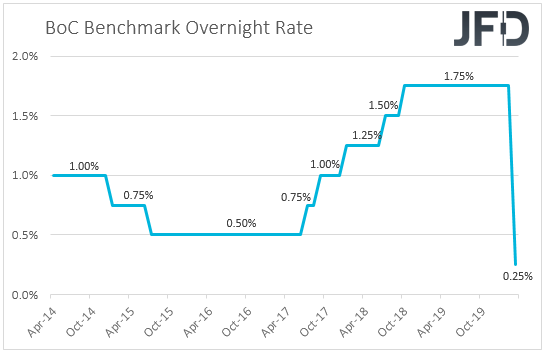

Apart from headlines surrounding the coronavirus saga, today, market participants may also pay attention to the BoC monetary policy decision. On March 27th, the Bank decided to slash interest rates to 0.25% and to launch a QE program in order to safeguard its economy from the effects of the coronavirus’s spreading. The Governing Council highlighted its readiness to take further action to support the economy and the financial system, but noted that the policy rate is now to its effective lower bound.

Last Thursday, the employment report for March disappointed largely, with the unemployment rate surging to 7.8% from 5.6% and the net change in employment revealing that more than 1mn jobs have been lost, which is the worst print in Canada’s history, at least since we can find data from. This may have increased the chances for more stimulus by the BoC, but bearing in mind that officials clearly noted that the policy rate has reached its effective lower bound, we don’t expect a rate cut at this gathering. Maybe officials will decide to expand their QE program, which could prove slightly negative for the Canadian dollar.

On the other hand, if they decide to hold off from acting due to the latest slowdown in the pandemic, the Loonie may strengthen. Such a scenario is not off the books, as officials may prefer to wait and see whether the virus spreading will slow more, and whether the already adopted measures have been having the desired effects on the Canadian economy.

USD/CAD – TECHNICAL OUTLOOK

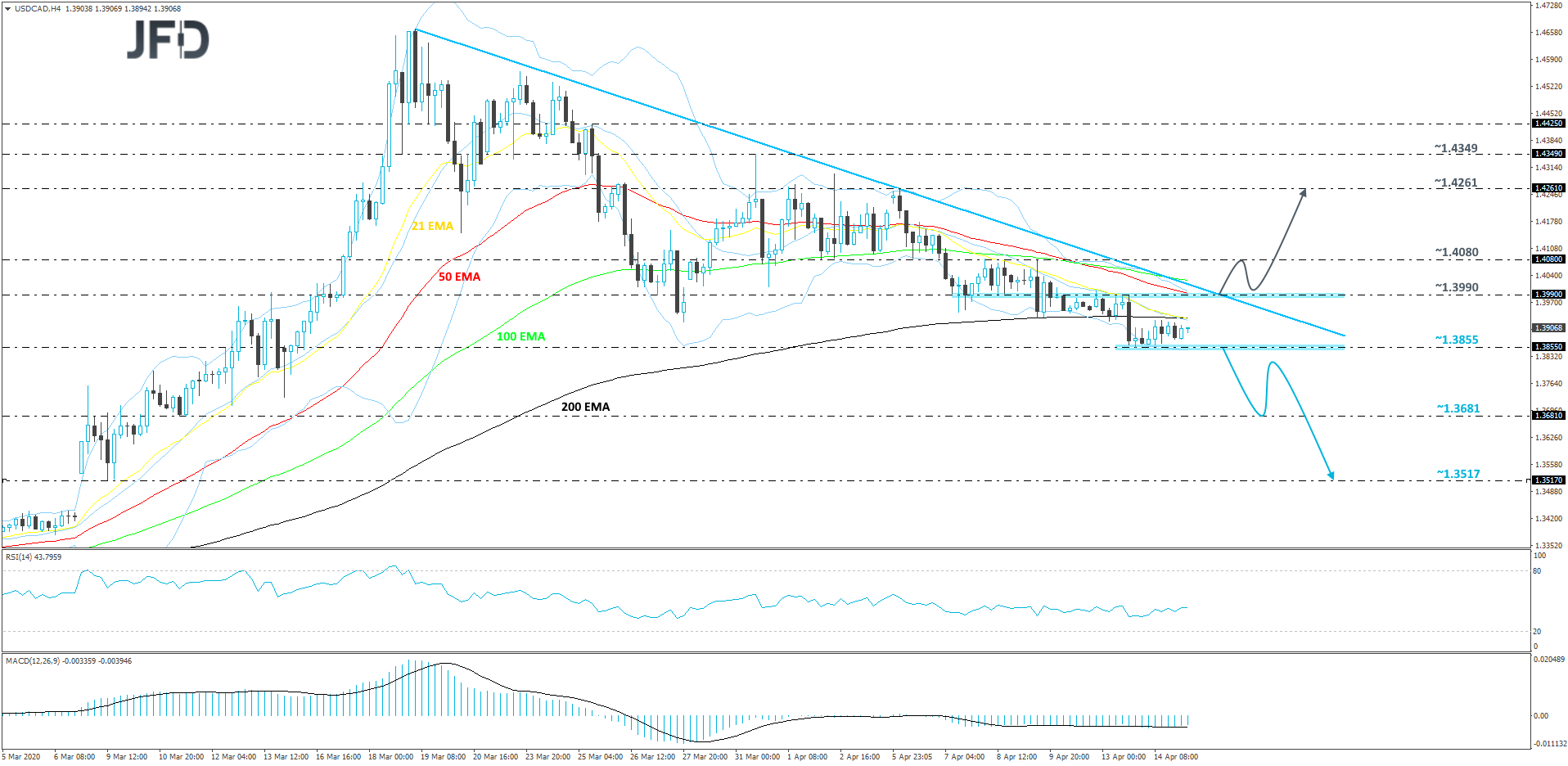

USD/CAD continues to trend lower, while trading below a short-term tentative downside resistance line taken from the high of March 19th. This week, the pair found some decent support near the 1.3855 hurdle, which continues to hold the rate from moving lower. In order to continue with the downside scenario, we need to see a break of that hurdle first, hence why we will take a cautiously-bearish approach for now.

A drop below the previously-discussed obstacle, at 1.3855, would confirm a forthcoming lower low and more sellers may join in and drive the pair in the southern direction, where the next possible support area might be seen around the 1.3681 zone. That zone marks the low of March 11th and if it holds, USD/CAD might rebound back up a bit. However, if the bulls can’t lift the rate back above the 1.3855 barrier, this may result in another round of selling, potentially sending the pair below the 1.3681 obstacle and targeting the 1.3517 level, marked by the low of March 9th.

Alternatively, if the pair makes a strong move higher and breaks the aforementioned upside line, together with the 1.3990 barrier, marked near the current high of this week, this might signal a change in the short-term trend. USD/CAD could then drift to the 1.4080 obstacle, a break of which may clear the path to the 1.4261 area, which is the high of April 6th.

AS FOR THE REST OF TODAY’S EVENTS

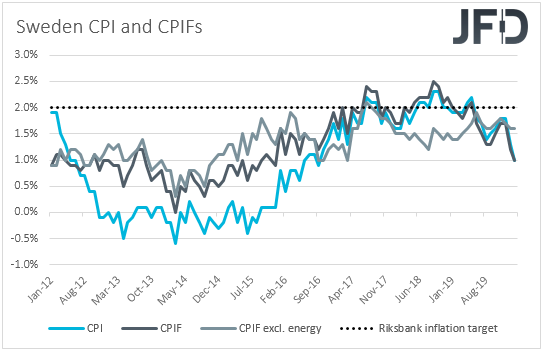

During the European morning, we get Sweden’s CPIs for March. Both the CPI and CPIF rates are forecast to have declined to +0.7% yoy from +1.0%, but as we have noted several times, we prefer to pay more attention to the core CPIF rate, which excludes the volatile items of energy. In February, that rate held steady at +1.6% yoy.

If the core CPIF rate stays close to its current levels, this would mean that the slide in the headline prints is mostly due to the tumble in oil prices and may encourage Riksbank officials to wait for a while more before deciding whether additional easing measures are needed. On the other hand, a notable slowdown in core inflation may prompt them to act again and expand further their QE purchases.

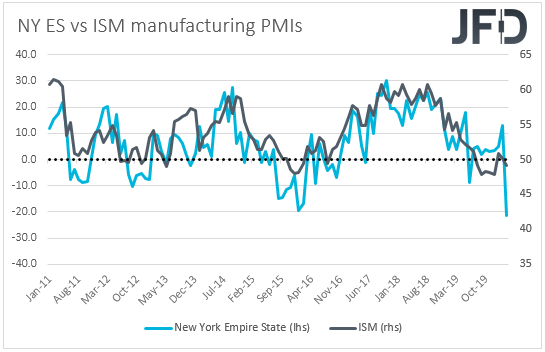

From the U.S., we get retail sales, industrial production, both for March, and the New York Empire state manufacturing index for April. Both the headline and core sales are expected to have tumbled 7.0% mom and 4.0% mom, after sliding 0.5% and 0.4% respectively. Those will be the biggest declines since we can find data from, but bearing in mind that investors already know that the US economy was hit hard due to the virus in March, big slides are unlikely to disappoint. The same applies to the industrial production, which is also expected to have slid notably.

Market participants may pay some extra attention to the New York Empire state index this time around. Although there are signs that the pandemic may be levelling off, this manufacturing index is expected to have fallen further into the negative territory, to -35.00 from -21.50, which may be an early omen that the sector’s wounds may drag for more than previously anticipated. A larger than expected tumble could raise questions as to whether the Markit and ISM manufacturing prints for the US as a whole will disappoint as well.

With regards to the energy market, we get the EIA (Energy Information Administration) report on crude oil inventories for last week. Expectations are for a 1.437mn inventory build following a 0.476mn the week before.

That said, bearing in mind that, yesterday, the API (American Petroleum Institute) revealed a 13.143mn build, we see the risks surrounding the EIA forecast as tilted to the upside. Oil prices slid yesterday, with WTI hitting once again the psychological zone of 20.00 and a surge in the EIA report could result in a break lower.

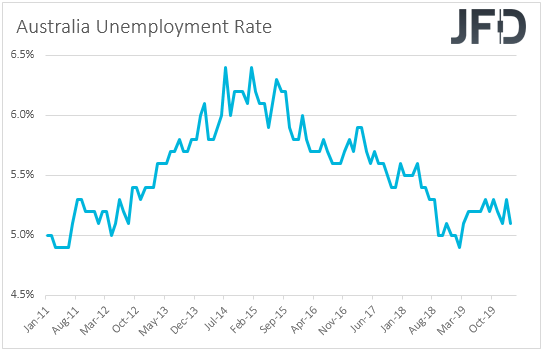

As for tonight, during the Asian morning Thursday, we get Australia’s employment report for March. The unemployment rate is forecast to have risen to 5.5% from 5.1%, while the net change in employment is expected to show a 40.0k slide in jobs, after the economy added 26.7k in February.

At their most recent gathering, last week, RBA policymakers left monetary policy unchanged and offered some details with regards to their QE program. They noted that they will do what is necessary to achieve a 3-year yield target of 0.25%, with the target expected to remain in place until progress is being made towards the goals for full employment and inflation. However, they added that if conditions continue to improve, it is likely that smaller and less frequent purchases of government bonds will be required.

After saying that interest rates have reached their effective lower bound at the prior meeting, the aforementioned points suggest that there is very little chance of expanding their QE program. On the contrary, they could soon scale it back if the spreading of the coronavirus continues to level off.

It would be interesting though to see whether a disappointing jobs report – with the unemployment rate rising further above the 4.5% threshold which the RBA expects to start generating inflationary pressures – will force them to change their minds and start considering a QE expansion.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Risk Appetite Eases, BoC Decides On Monetary Policy

Published 04/15/2020, 03:40 AM

Updated 07/09/2023, 06:31 AM

Risk Appetite Eases, BoC Decides On Monetary Policy

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.