- US business activity picks up in April, but Fed still seen pausing after May

- Mixed start for dollar and stocks before barrage of tech earnings and US data

- Yen steady ahead of BoJ decision; euro firmer after PMIs and hawkish ECB, GDP next

Fed bets little changed after stronger PMIs

Despite a slew of rate hikes and a mini banking crisis, the US economy has not edged any closer to a recession, defying yet again predictions of sharp slowdown. Instead, business activity seems to be on the rise in April, with both the services and manufacturing sectors displaying unexpected strength according to Friday’s flash PMI estimates by S&P Global.

The composite PMI measuring overall economic activity accelerated to its highest in 11 months, suggesting little lasting impact from the banking turmoil on the real economy. The survey also pointed to higher input prices and employment – something that should worry the Fed and the markets.

Yet, Fed tightening expectations barely budged after the data, which merely reinforced the recent shift in view that rate cuts are less likely but that the Fed will still probably pause after the May meeting. Investors had pared back their rate cut expectations after some hawkish remarks from Governor Waller and only one 25-bps reduction remains priced in for 2023.

But last week’s remarks, including those of Mester and Cook were somewhat more balanced, keeping alive hopes that the expected rate hike at next week’s meeting will be the last. What could potentially determine whether or not the Fed will signal a pause in May is any evidence that lending standards tightened in recent weeks. The Fed conducts its own quarterly survey on credit expansion to businesses and consumers and so policymakers will be watching the results of the latest report very closely amid some signs of credit tightening.

Dollar bulls struggle to keep up with hawkish ECB

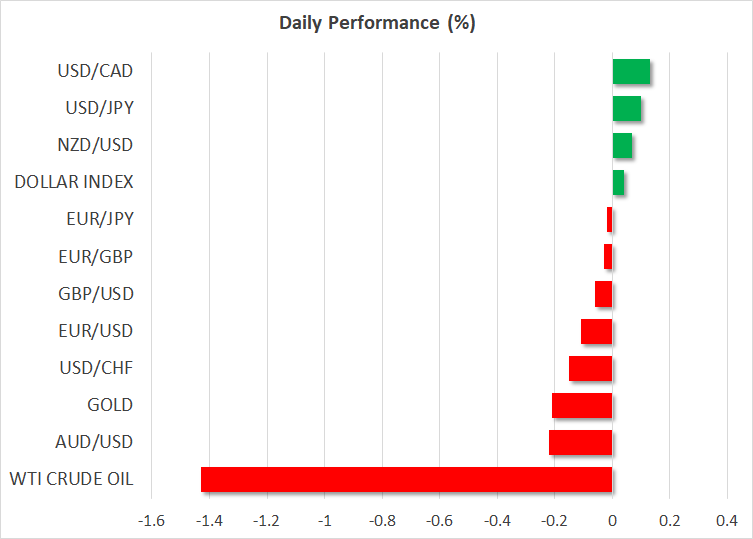

With Fed bets largely unchanged after the PMIs, the US dollar has been drifting slightly lower since Friday. Although the Fed’s message that the odds of a rate cut this year are remote is slowly sinking in, other central banks have also been keeping up with their hawkish rhetoric – most notably the ECB – and this is hindering any bullish bets for the dollar.

ECB President Christine Lagarde reiterated on Friday that more rate hikes are needed, while Governing Council member Klaas Knot signalled that the tightening cycle could extend well into the summer.

Eurozone PMI numbers were also broadly better than expected in April, though the slump in manufacturing deepened. It was a similar picture in the UK, but the euro appears to have picked up a bit more momentum than the pound from the flash PMIs, most likely due to the ECB’s very hawkish language.

The euro is flirting with the $1.10 level today and sterling is marginally higher too, trading around $1.2450.

BoJ meeting eyed ahead of Fed and ECB decisions

There are more important data releases on the horizon this week, including preliminary GDP estimates out of the United States (Thursday) and Eurozone (Friday), and the PCE inflation readings on Friday. Both the Fed and ECB meet next week so the incoming numbers might prove to be crucial.

Also on the agenda on Friday is the Bank of Japan’s policy decision, which will be the first under new Governor Kazuo Ueda. However, all the indications are that any shocks will be saved for later in the year and no surprises are anticipated this week, with Ueda strongly hinting that policy easing must continue for the time being.

The yen has been on a downward path during April, as expectations of a policy tweak have been scaled back, and remained under slight pressure against the greenback on Monday.

Tech earnings under the limelight

In equities, European markets are mostly in the red today as US futures slipped after a subdued session on Wall Street on Friday. However, things should liven up this week as Microsoft (NASDAQ:MSFT) and Alphabet (NASDAQ:GOOGL) report their earnings tomorrow, with Amazon’s results coming up on Thursday.

It’s possible that all three tech behemoths will have benefited from the solid performances of their cloud units but investors will also be wanting to hear more about their AI plans.