Market sentiment improved late in the US session yesterday, with Wall Street aided by technology stocks. Investors may have turned their gaze back to the easing of the “stay at home” measures, adopted due to the fast spreading of the coronavirus. Overnight, the RBA decided to keep interest rates unchanged. Officials announced they have scaled back the size and frequency of their bond purchases, but they added that they are prepared to scale-up these purchases again if deemed necessary.

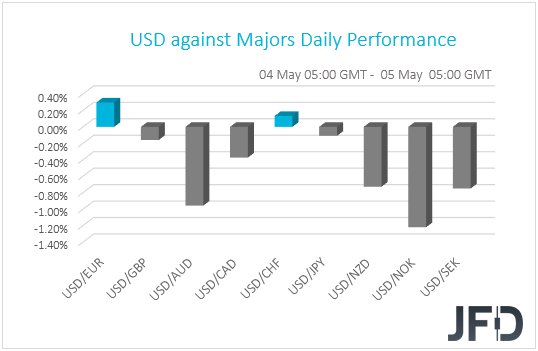

RISK ASSETS REBOUND, SAFE HAVENS SLIDEThe dollar reversed and traded lower against most of the other G10 currencies on Monday and during the Asian session Tuesday. It gained slightly only against EUR and CHF. The main gainers were NOK, AUD, SEK, and NZD in that order, while the currencies against which the greenback lost the least ground were GBP and JPY.

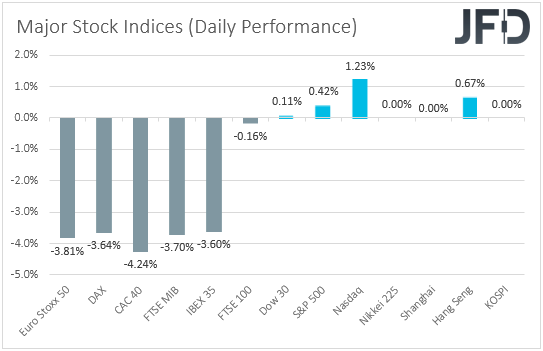

The relative weakness of the dollar and the other safe havens, franc and yen, combined with the strengthening of the risk-linked Aussie and Kiwi, suggests that market sentiment rebounded again at some point during the day. After an extended weekend, due to Friday’s holiday, most major EU indices tumbled more than 3%, perhaps due to tensions over the US-China trade saga flaring up again. Remember that on Friday, US President Trump said that China could have contained the virus, and threatened that he could use tariffs to respond to China and that if they don’t buy US goods, the US will end the trade deal.

He and his State Secretary Mike Pompeo accused the world’s second-largest economy of covering up the release of the virus from a laboratory in Wuhan. Wall Street opened lower as well and continued drifting south at the start of the session, but rebounded later, with all three of its main indices finishing their trading in the green. The recovery was mainly aided by a rebound in technology stocks, with Nasdaq gaining 1.23%. The positive sentiment rolled over into the Asian session as well, with Hong Kong’s Hang Seng gaining 0.67%. Japanese, Chinese, and South Korea’s markets were closed due to holidays.

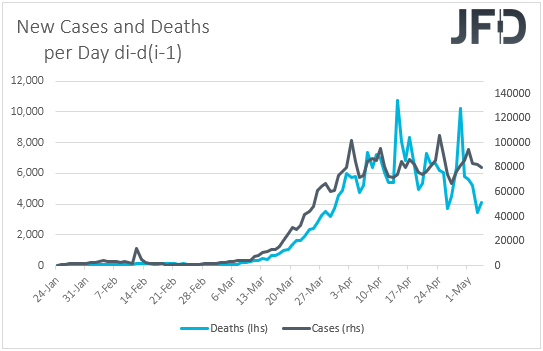

It seems that following the spark of new US-China tensions, investors may have turned their gaze back to the easing of the “stay at home” measures, adopted due to the fast spreading of the coronavirus. Yesterday, New York Governor announced a phased reopening of businesses, while his Californian colleague said that a reopening could start as early as this week. What may have also helped investors’ appetite could have been the slowdown in both infected cases and deaths. Although deaths accelerated somewhat on Monday, they have already slowed notably over the weekend. All this brightens the green light for governments around the globe to continue easing their restrictions.

As for our view, we stick to our guns that the combination of stimulative measures by governments and central banks, and the prospect of a vaccine being ready for distribution soon, makes us more trustful over another round of recovery in equities and other risk-linked assets. However, one condition for this to materialize is no new negative headlines surrounding the US-China trade saga. Apart from that, another risk may be lifting the restrictive measures too quickly, which may result in the coronavirus to start spreading at an exponential pace again. We believe that this has to be a slow process. Otherwise, it may not take long before we are back to square one.

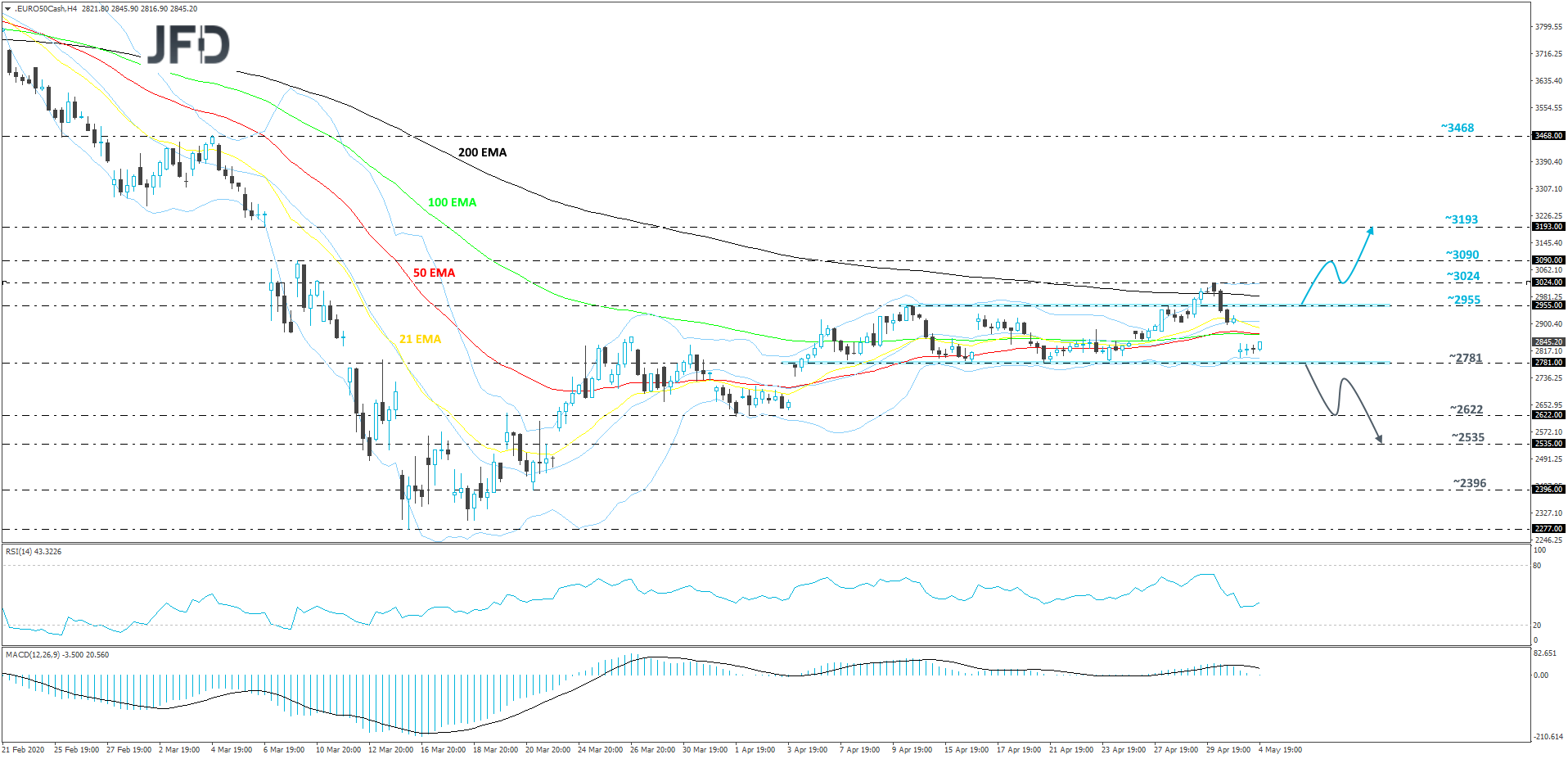

EURO STOXX 50 – TECHNICAL OUTLOOK

Looking at our Euro Stoxx 50 cash index, we can see that it got back inside the small range, roughly between the 2781 and 2955 levels, which maintained in itself the price action for the most of April. Yesterday, the index came close to testing the lower bound of that range, but failed to reach it and today the price is trying to make its way up again. That said, as long as the index stays inside that range, we will remain neutral.

If Euro Stoxx 50 climbs higher again and manages to overcome the 2955 barrier, marked by the highs of April 14th and 28th, this could also place the price above the 200 EMA on the 4-hour chart. More buyers could see this as a good opportunity to step in and drive the index higher, possibly overcoming the high of April 30th, at 3024, and reaching the 3090 hurdle, which is the high of March 10th. The price may stall there for a bit, but if the buyers are still feeling comfortable, a further push north could bring the index to the 3193 level, marked by the low of March 6th.

On the other hand, if the price falls below the 2781 hurdle, which is the lower side of the aforementioned range, this would confirm a forthcoming lower low and more sellers may join in. That’s when we will examine a possible move to the 2622 obstacle, which if fails to provide support and breaks could send Euro Stoxx 50 to the 2535 level, marked by an intraday swing high of March 23rd.

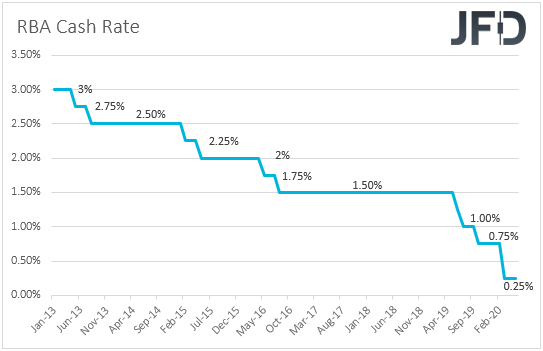

RBA KEEPS RATES STEADY, SCALES BACK ITS QE PURCHASES

Apart from news and headlines surrounding the coronavirus and US-China sequels, we also had an RBA monetary policy decision overnight. As was widely anticipated, the Bank kept its cash rate and the target of its 3-year government bond yields at 0.25%. The official said that they have scaled back the size and frequency of their bond purchases, but they added that they are prepared to scale-up these purchases again if deemed necessary.

The Aussie barely reacted at the time of the announcement, perhaps as this was the expected outcome. Overall though, the currency could stay supported if the broader market sentiment rebounds again on optimism surrounding the easing of the coronavirus. The commodity-linked currency may well outperform the safe havens dollar, yen and franc, but it could also win the battle against its neighboring Kiwi.

Although a commodity-linked currency as well, the New Zealand dollar may underperform the Aussie due to monetary policy divergence. While the RBA has started scaling back its QE purchases, the RBNZ is expected to double its QE pace this month, at least according to Westpac, and also to cut interest rates to -0.5% in November, a move that could be telegraphed as early as in August. Remember that the RBA noted that, at +0.25%, interest rates have hit their effective lower bound.

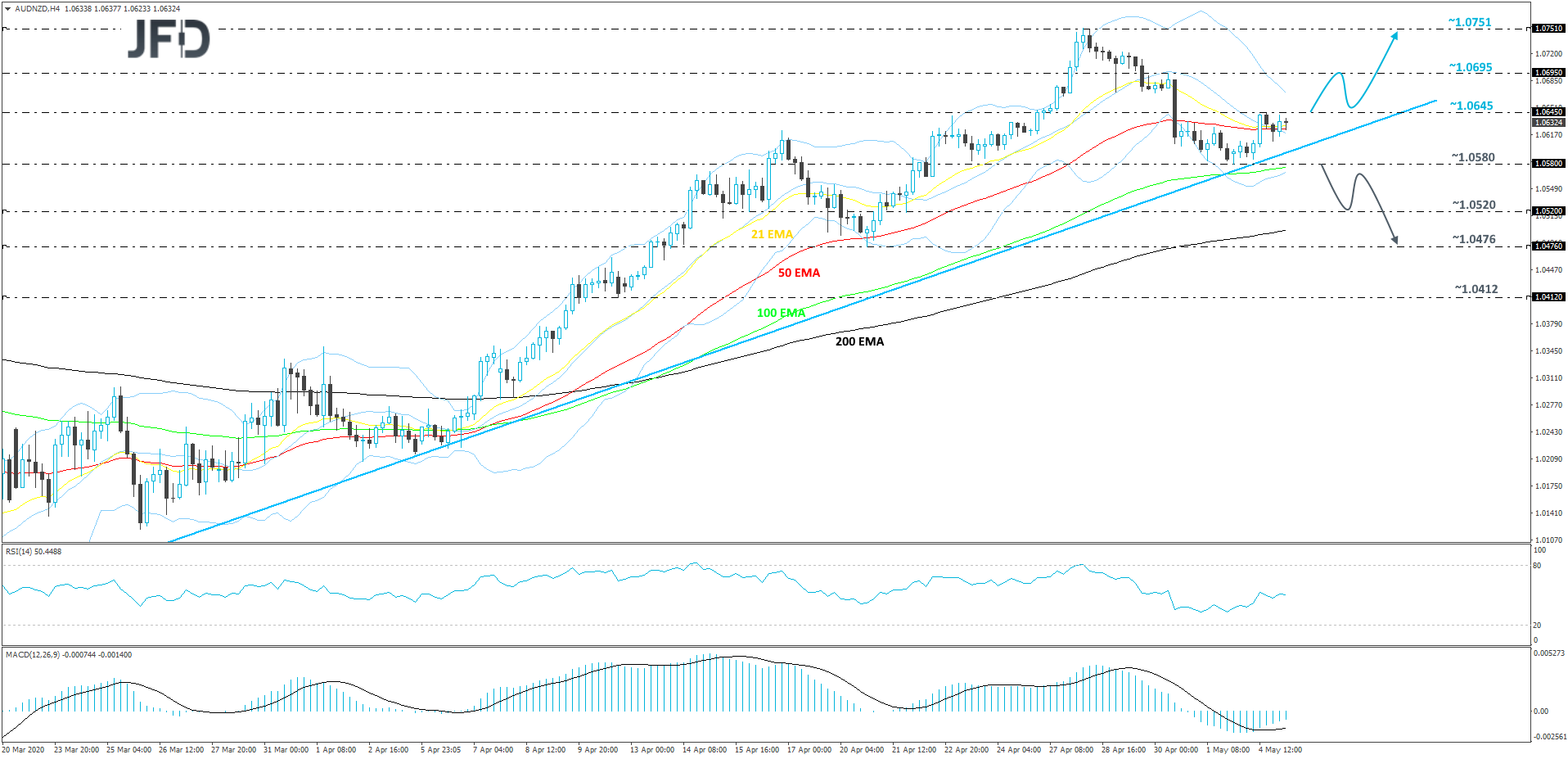

AUD/NZD – TECHNICAL OUTLOOK

At the end of last week, AUD/NZD once again came close to its short-term upside support line taken from the low of March 18th, from which the pair rebounded yesterday and is now trying to make its way back up. For now, we will stay bullish, especially if the rate climbs above yesterday’s high.

A push above the 1.0645 barrier, marked by yesterday’s high, could increase the pair’s chances of moving further north. AUD/NZD could travel to the high of April 30th, at 1.0695, which if provides decent resistance, might force the rate to retrace slightly. However, if the pair continues to balance above the aforementioned upside line, the bulls may take charge again. If

AUD/NZD can overcome the 1.0695 hurdle this time, then the next potential resistance area could be around the 1.0751 level, marked by the highest point of April.

Alternatively, if the aforementioned upside line breaks and the pair falls below last week’s low, at 1.0580, this would confirm a forthcoming lower low and more sellers could join in. We will then target the 1.0520 territory, a break of which may clear the way for a drift to the 1.0476 zone, marked by the low of April 20th.

AS FOR THE REST OF TODAY’S EVENTS

During the European morning, Sweden’s GDP for Q1 is due to be released, but no forecast is currently available. At last week’s gathering, Riksbank policymakers decided to leave the repo rate unchanged at 0% and to continue their purchases of government and mortgage bonds up to the end of September 2020. They noted that they cannot rule out the possibility of interest rates being cut at a later date, but they added that it was not deemed justified at this point to increase demand by a cut.

Given the fast spreading of the coronavirus outside China during the last month of the quarter, we wouldn’t be surprised if we get a negative print. So, the question may be how deep the wounds have been. Following just a downtick in the core CPIF rate for the month of March, a not-that-bad number may allow Riksbank policymakers to stay sidelined for a while more. On the other hand, a deep contraction may raise speculation that policymakers could take interest rates back into the negative territory.

From the UK, we get the construction PMI for April, which is expected to have rebounded to 44.0 from 39.3, as well as the final services and composite PMIs, which are expected to confirm their preliminary estimates of 12.3 and 12.9 respectively.

Later in the day, we get more final PMIs for April, this time from the US. The services and composite indices are due to be released, but similarly to the UK ones, they are anticipated to confirm their initial forecasts. Market participants may pay more attention to the ISM non-manufacturing PMI for the month, which is expected to have declined to 44.0 from 52.5. The US and

Canadian trade data are also coming out.

With regards to the energy market, the API (American Petroleum Institute) weekly report on crude oil inventories is coming out, but as it is always the case, no forecast is available.

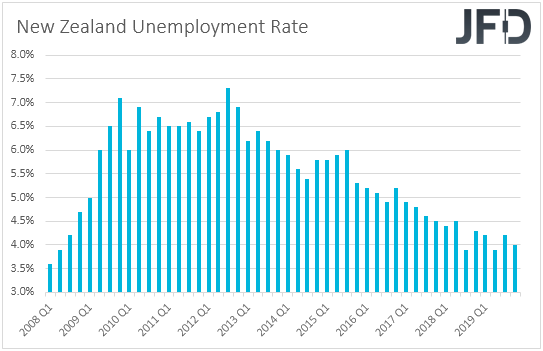

As for tonight, during the Asian morning Wednesday, it’s another holiday in Japan and thus, Japanese markets will stay closed. In New Zealand, the employment report for Q1 is coming out. The unemployment rate is expected to have increased to 4.3% from 4.0%, while the net change in employment is forecast to show that the economy lost 0.3% jobs, after a stagnation in the last three months of 2019. The labor costs index is anticipated to have ticked up to +2.5% yoy from +2.4%. A soft employment report may add more credence to the view of further easing by the RBNZ and perhaps hurt the Kiwi.

Australia’s retail sales for Q1 and China’s Caixin services PMI for April are also due out. Australian retail sales are expected to have accelerated to +1.7% qoq from +0.5%, while no forecast is available for China’s Caixin index. That said, bearing in mind that the official non-manufacturing PMI rose to 53.2 from 52.3, we see the case for the Caixin index to have moved in a similar fashion.