Bloomberg’s Nir Kaissar is no fan of high-yield bonds. He warns that this slice of fixed income “is likely to be a drag on growth” for the risk portion of portfolios “while including them in non-risk undermines safety. Neither option is appealing.” Even worse, junk bonds don’t offer much diversification “because they’re highly correlated with stocks,” he charges.

The crowd, however, thinks differently, or so it seems, based on the recent love affair with junk. Or maybe the market is simply ignoring the caveats in pursuit of what’s considered easy money. Whatever the explanation, there’s no denying junk’s bull market of late. Indeed, high-yield securities continue to top this year’s rally among the major slices of the bond market, based on a set of exchange-traded funds through yesterday’s close (Apr. 26).

SPDR Bloomberg Barclays High Yield Bond (NYSE:JNK) is up a sizzling 9.2% so far in 2019 (as of Apr. 25) — far above the 2.8% year-to-date gain for the broadly defined investment-grade market, based on Vanguard Total Bond Market (NYSE:BND). The only slice of investment-grade bonds that comes close to JNK’s year-to-date surge at the moment: long-term investment-grade corporates via Vanguard Long-Term Corporate Bond (NASDAQ:VCLT), which is up 8.5% this year.

In other words, the next best thing to matching junk’s rally this year has required going far out on the curve for maturities in corporates. Indeed, VCLT’s average effective maturity is nearly 24 years, according to Morningstar.com – far above JNK’s roughly 6-year average.

Longer term, JNK’s return premium holds up nicely, or at least it has for the current trailing three-year window. An investment in SPDR Bloomberg Barclays (LON:BARC) High Yield Bond three years ago would have popped 23%, well ahead of VCLT’s 15% and BND’s 6%.

In the longer term, it’s true that US equities have beat junk, but there’s room for debate about the diversification benefits for high-yield bonds. For perspective, let’s switch to a pair of mutual funds that offer 15-year track records. (JNK, by comparison, was launched in 2007.) Vanguard 500 (VFINX), an S&P 500 index fund, earned an annualized 8.6% over the trailing 15-year period, moderately higher than 6.3% for Vanguard High-Yield Corporate (VWEHX), based on Morningstar data through yesterday (Apr. 25).

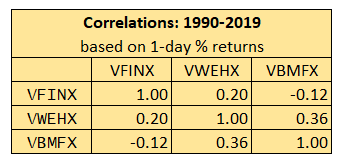

The correlation comparison, on the other hand, looks encouraging. Based on 1-day returns since 1990 through Apr. 25, 2019, the correlation for junk (VWEHX) vs. US stocks (VFINX) is a low 0.20. Note, too, that the 1-day correlation between junk and investment-grade bonds overall – via Vanguard Total Bond Market (VBMFX) – is also quite low at 0.36. (Perfect positive correlation is 1.0; no correlation is 0.0; perfect negative correlation is -1.0).

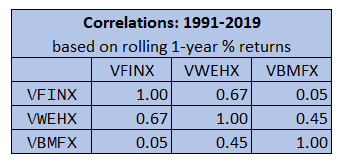

The correlations move up when we use rolling 1-year returns since 1990, but as the next table below suggests there’s still a fair amount of potential diversification meat on the junk-bond bone.

Minds may differ on the wisdom of using junk bonds in a broadly diversified portfolio, but one thing is clear: the crowd’s appetite for high-yield fixed-income securities remains red hot this year. The future is uncertain, of course, but with the Federal Reserve expected to refrain from additional interest-rate hikes for the near term, perhaps even cutting rates at some point, it’s not inconceivable that the crowd’s love affair with junk could roll on.

If there’s a risk to worry about with junk it’s probably the economy. But with U.S. recession risk low, there’s a case to be made that the high-yield market faces no obvious threat, at least based on the numbers published to date… with one key exception: valuation.

The yield spread in junk bonds has fallen sharply in recent years, courtesy of the bull market in prices for these securities. As a result, the additional yield in this market is below four percentage points, based on the ICE (NYSE:ICE) BofAML Option-Adjusted Spreads Index. That’s close to the lowest level on record (since 1997). In other words, junk is priced for perfection and so a future that delivers less-than-perfect results is a potential hazard.

For now, however, the party continues.