As global shipping continues to reach for the max -- Panamax, Panamax Max, Post Panamax, Post Panamax Plus and New Panamax, to be exact, in addition to other massive container ships plying the global seas these days -- our focus shifts to the liquids that have been traveling to Japan more and more.

Namely crude oil, liquefied petroleum gas and liquefied natural gas (LNG), as the country has needed to beef up its fuel supply after the tsunami in the spring of 2011 precipitated the Fukushima disaster -- and systemic shutdowns of much of the country’s nuclear power reactors.

So what does that mean for the future of U.S. LNG exports, and for U.S. manufacturing?

New High

Turns out that Japan’s monthly trade deficit has hit a new high. Reports put the shortfall at 1.63 trillion yen (US$17.4 billion), the worst-ever monthly deficit. Although exports rose, including more shipped auto parts, imports increased 7.3% primarily due to Japan’s fuel needs.

In fact, Japan’s trade deficit for 2012 hit a new high as well -- 6.927 trillion yen ($78.24 billion). According to a Reuters report, Japan, the world’s third-largest oil consumer, brought in 2% more crude in 2012 over 2011, at a rate of 3.66 million barrels per day. Imports of thermal coal were up 6.5% year-on-year, while liquefied petroleum gas imports rose 5.8%.

However, LNG imports shot up 11.2% in 2012 over 2011, proving to be a record high. (In terms of currency value, that represents a whopping 25.4% increase.)

What's That Mean For U.S. Exports?

Japan is the number-one importer of LNG in the world -- and the U.S. is their primary supplier.

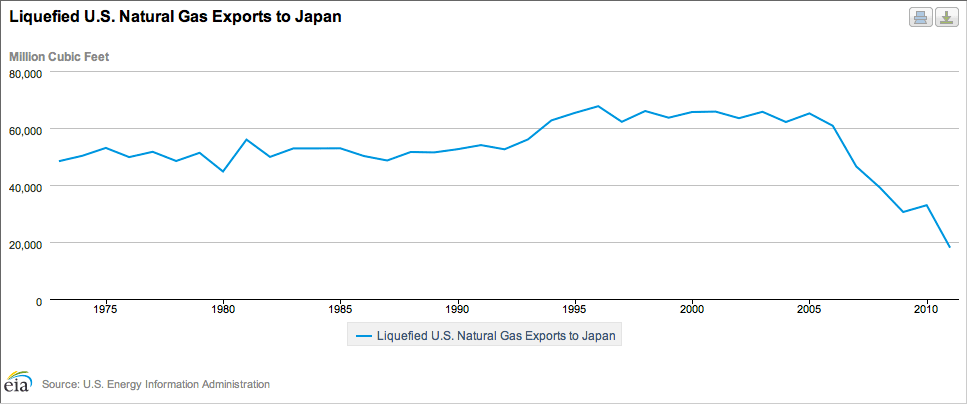

According to EIA data, Japan is by far the number-one export market for US LNG on a volume basis since the 1970s, and blows away Brazil (the only other importer of U.S. LNG aside from Mexico) between June and November 2012, for example. Total U.S. exports to Japan in that timeframe stand at 6.55 billion cubic feet.

Brazil’s imports, by comparison, total 2.64 billion cubic feet.

Historically, however, U.S. exports of LNG to Japan are at their lowest point in decades, as the EIA graph below shows.

Although Japan wants to increase its imports based on recent power capacity struggles -- Prime Minister Shinzo Abe will press President Obama for even more soon – U.S. manufacturers may want to keep global LNG exports to this trend. (Besides, who can say whether Japan’s power shortcomings will last indefinitely?)

The Hurdle

The primary reasons for this include natural gas being cheaper and burning cleaner. (Mills in the U.S., such as Nucor, are already making use of natural gas to their competitive advantage.) But the main hurdle is that hardly any U.S. liquefaction facilities exist yet.

According to this article, LNG-exporting infrastructure is a big issue: “All LNG that the U.S. currently produces comes from a terminal in Alaska. Recently, BP signed a 20-year contract to ship LNG from a terminal in Freeport, Texas, which should begin in 2017 with the completion of facility construction [in Louisiana].”

The destination of what the Louisiana plant produces? Japan.

So the question lingers: should free trade reign, or should the U.S. hang onto its cheap fuel?

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Japan's Trade Deficit: A Boon For U.S. LNG?

Published 02/21/2013, 12:37 PM

Updated 07/09/2023, 06:31 AM

Japan's Trade Deficit: A Boon For U.S. LNG?

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.