Major EU and US indices closed their Monday sessions in the red, perhaps as investors remained relatively cautious ahead of the earnings season, but also ahead of today’s US CPIs for March.

Later today, during the Wednesday morning Asian session, the RBNZ decides on monetary policy and it would be interesting to see whether officials will sound more dovish this time around.

Investors Stay Cautious Ahead Of The US CPIs

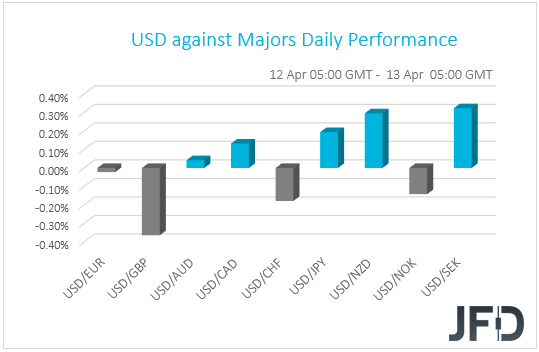

The US dollar traded mixed against the other G10 currencies on Monday and during the Asian session today. It gained versus SEK, NZD, JPY, and CAD in that order, while it underperformed against GBP, CHF, and NOK. The greenback was found virtually unchanged versus AUD and EUR.

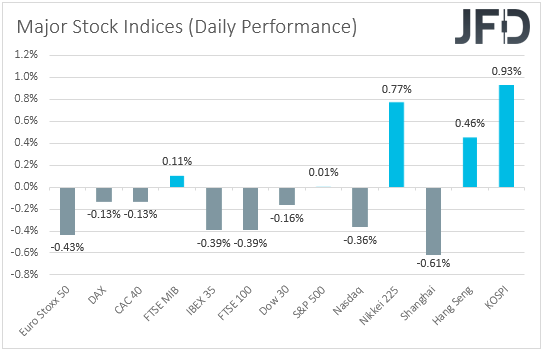

The weakening of the kiwi, combined with the strengthening of the Swiss franc, suggests that markets may have traded in a risk-off fashion yesterday and today in Asia. Indeed, major EU and US indices finished their trading in the red, with the only exceptions being Italy’s FTSE MIB and the S&P 500. The former gained 0.11%, while the latter closed virtually unchanged.

Investors’ appetites improved during the Asian session today. Although China’s Shanghai Composite slid 0.61%, Japan’s Nikkei 225 and Hong Kong’s Hang Seng gained 0.77% and 0.46% respectively.

EU and US shares may have slid somewhat as investors remained relatively cautious ahead of the quarterly corporate earnings season, with major banks like Goldman Sachs (NYSE:GS), JPMorgan (NYSE:JPM), and Wells Fargo (NYSE:WFC) reporting their results on Wednesday. Market participants may have also stayed careful ahead of the US inflation data, due out to be released today.

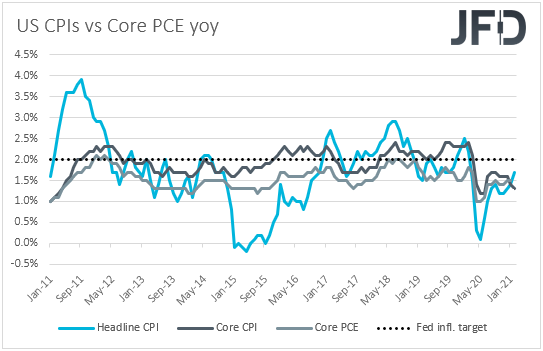

The headline CPI rate is expected to jump to +2.5% yoy from +1.7%, while the core one is anticipated to rise to +1.6% yoy from +1.3%. This is likely to prove positive for the US dollar, but we don’t expect any recovery to last for long. After all, the Fed has clearly noted that any surge in inflation this year is likely to prove to be temporary and that inflation will rise and stay above 2% for some time—the goal for beginning to normalize policy—in the years after 2023.

Let’s not forget that Fed Chief Jerome Powell himself has been repeatedly stating that it is too early to start discussing policy normalization. With all that in mind, we would expect the US dollar to pull back again soon, and equities to continue trending north.

USD/CHF Technical Outlook

From the beginning of April, USD/CHF continues to drift lower, while trading below a short-term tentative downside resistance line, taken from the high of Apr. 1. Recently, the pair fell below the 200 EMA on our 4-hour chart, which could add more negativity into the near-term outlook. That said, in order to get comfortable with larger extensions to the downside, we would prefer to wait for a break below the 0.9212 hurdle first. Hence our cautiously-bearish approach for now.

If, eventually, we do see the rate falling below the 0.9212 zone, marked by the lows of Mar. 17 and Apr. 12, that will confirm a forthcoming lower low, possibly setting the stage for further declines, as more sellers might join in. USD/CHF could travel to the 0.9189 obstacle, or to the 0.9167 territory, marked by an intraday swing low of Mar. 3, which may temporarily provide a hold-up.

That said, if the bears continue to apply pressure on the pair, this might result in another decline, potentially opening the door for a move to the 0.9136 level, marked by the low of March 2nd.

In order to shift our attention to some higher areas, a break of the aforementioned downside line would be required. Also, a push above the 0.9353 barrier, marked by the low of Apr. 5, could strengthen the upside scenario, attracting more buyers into the game. The pair may then rise to the 0.9396 obstacle, a break of which could set the stage for a push to the 0.9438 level, marked by the high of Apr. 5.

NASDAQ 100 Technical Outlook

Yesterday, the NASDAQ 100 cash index struggled to overcome the 13850 barrier, which is the high of last week. Today, the cash index was correcting lower, but overall, the price continued to trade above a short-term tentative upside support line, drawn from the low of Mar. 25.

Even if we see a decline in the near term, if NASDAQ 100 stays somewhere above the 21 EMA, or the 13742 hurdle, marked by yesterday’s low, this move lower could be classed as a temporary correction before another possible move higher.

As mentioned above, a small move lower could test the 21 EMA, or the 13742 hurdle. If that area does provide good support, we might see a rebound, where NASDAQ 100 may end up testing the 13850 barrier again, which is the current highest point of April. If that barrier is finally broken, this will confirm a forthcoming higher high and set the stage for a push towards the 13905 level.

That level is the current all-time high, however, if the bulls are feeling comfortable, they might overcome that obstacle and place the index into uncharted territory.

Alternatively, if the price slides below the 13742 hurdle, or even falls below the 13657 zone, marked by the high of Apr. 6 and the low of Apr. 9, that could open the door for a larger correction lower.

NASDAQ 100 may then slide to the 13522 obstacle, a break of which might clear the path towards the previously discussed upside line, which could provide a hold-up for the index. Around there, the price might also test the 13401 level, which marks the high of Apr. 2.

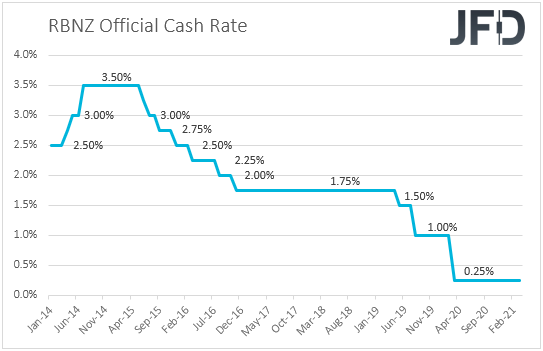

Will The RBNZ Sound More Dovish This Time?

During the Asian session Wednesday, the RBNZ decides on monetary policy. At its previous meeting, in February, this Bank decided to keep its official cash rate and its Large-Scale Asset Purchase program unchanged, noting that they agreed to stay prepared to provide additional support if necessary, with the options including a lower OCR.

The kiwi slid initially, perhaps as the statement may have revived speculation over negative interest rates by this Bank, but it was quick to rebound, recover the losses, and trade even higher, perhaps as investors started scanning the quarterly Monetary Policy Report, in which the economic forecasts showed the OCR turning higher from December.

However, since then, data showed that New Zealand’s economy contracted in the last quarter of 2020, while the government decided to take measures in order to cool its hot housing market, including higher taxes.

Those developments suggest that the RBNZ may push back the timing of when it expects to start raising rates. Policymakers are expected to keep their monetary policy settings unchanged once again, and thus, all the attention may be on whether they will sound more dovish this time around. In other words, it would be interesting to see whether they will keep the door for a rate cut open, and whether they will hint that interest rates are likely to stay low for longer than previously assumed.

If so, the New Zealand dollar is likely to come under selling interest. That said, we don’t expect this to result in a major downtrend, as the risk-linked currency may be helped by a potential further improvement in the broader market sentiment.

As For The Rest Of Today's Events

During the early European morning, we already got the UK GDP for February, as well as the nation’s industrial and manufacturing production rates for the month. GDP rebounded 0.4% mom following an upwardly revised tumble of 2.2% in January, while both the industrial and manufacturing production rates rose by more than anticipated.

The pound rose on Monday due to the easing of some COVID-related restrictions in the UK, and it may continue recovering following the aforementioned data. However, fears that safety concerns with regards to the AstraZeneca (NASDAQ:AZN) drug may slow down the vaccine rollout in the UK, could keep a lid on any short-term sterling gains as other countries catch up.

Germany’s ZEW survey for April is due to be released. The current conditions index is expected to have risen to -52.0 from -61.0, while the economic sentiment one is forecast to have inched up to 79.5 form 76.6.

We also have four Fed speakers on today’s agenda and those are: San Francisco President Mary Daly, Kansas City President Esther George, Philadelphia President Patrick Harker, and Atlanta President Raphael Bostic.