Fed policymakers decided to keep their policy steady yesterday, with Fed Chief Powell maintaining the stance that it is too early to start discussing policy normalization. Later in the day, US President Biden, speaking before Congress, proposed a new spending package. As for today, attention is likely to fall on the preliminary US GDP for Q1, with expectations pointing to accelerating economic growth.

Fed Still Not Ready To Discuss Tapering, Biden Proposes 1.8 Trillion Spending Plan

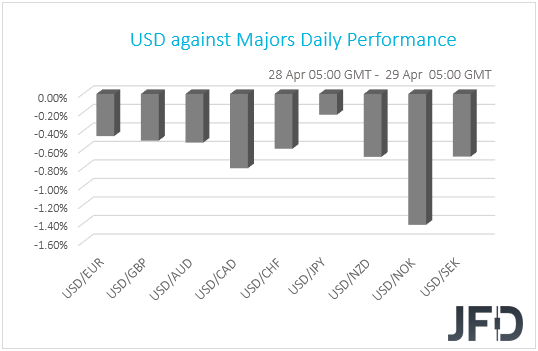

The US dollar traded lower against all the other G10 currencies on Wednesday and during the Asian session Thursday. It lost the most ground versus NOK, CAD, SEK, and NZD in that order, while it underperformed the least against JPY.

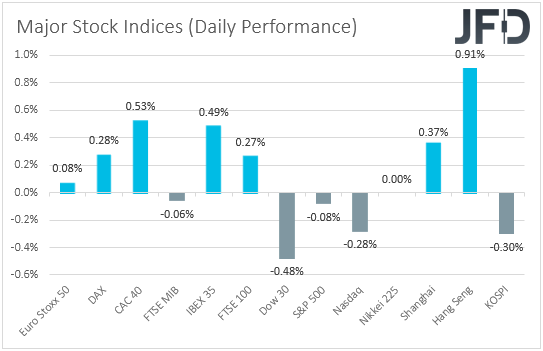

The strengthening of the commodity-linked Loonie, Kiwi and Krone, combined with the weakness in the dollar and the yen, suggests that markets traded in a risk-on fashion yesterday and today in Asia. Turning our gaze to the equity world, we see that most major EU indices closed in the green, and although all three of Wall Street’s main indices finished lower, this was after the S&P 500 hit a fresh record high. Investors’ appetite improved again during the Asian session today.

Yesterday, the main items on the agenda were the FOMC decision and the speech of US President Joe Biden before Congress. Getting the ball rolling with the Fed, policymakers decided to keep their monetary policy settings unchanged, and repeated that they will keep it that way “until labor market conditions have reached levels consistent with the Committee's assessments of maximum employment and inflation has risen to 2 percent and is on track to moderately exceed 2 percent for some time." Yes, they acknowledged the improvement in economic activity, but at the press conference following the decision, Fed Chair Powell stuck to his guns, saying that the economy is a “long way” from their goals and that it’s not the time to start discussing about tapering QE.

This is inline with what we’ve been expecting and thus, we will maintain the view that with the Fed staying dovish, equities are likely to continue trending north. Other risk-linked assets, like the Aussie and the Kiwi may also benefit from investors’ decision to increase their risk exposure. On the other hand, the US dollar and other safe havens, like the yen, may stay under selling interest.

Now, passing the ball to Biden, in a speech before Congress, the US President proposed a sweeping new USD 1.8trln spending package. Although Democrats applauded Biden, Republicans stayed largely silent, which raises question as to whether they will eventually support the plan. In any case, Democrats hold majorities in both chambers of the Congress, which means that his proposal could pass without Republican support. After all, this was the case with his USD 1.9trln pandemic stimulus plan. Maybe that’s why equities marched even higher during and after his speech.

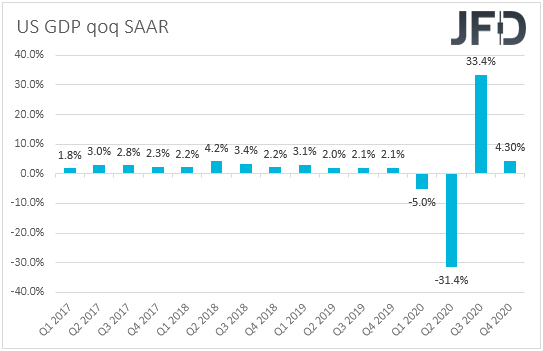

As for today, the spotlight may turn to the preliminary US DP for Q1. The forecast suggests that economic activity in the US accelerated to +6.1% qoq SAAR from +4.3%, but the Atlanta Fed GDP Now model points to a 7.9% expansion, which tilts the risks surrounding the actual forecast to the upside. A solid number will confirm that the world’s largest economy is recovering from the coronavirus-related damages at a fast pace and may eventually tempt some participants to start thinking as to whether the Fed should consider normalizing its policy earlier. This could take the US dollar slightly higher and equities lower, but we don’t expect it to prove a game changer. We would consider such a counter reaction as a corrective move. We stick to our guns that with the Fed prepared to keep its policy extra loose for long and President Biden willing to pass more supportive bills, the broader market sentiment is very likely to stay supported.

NZD/USDTechnical Outlook

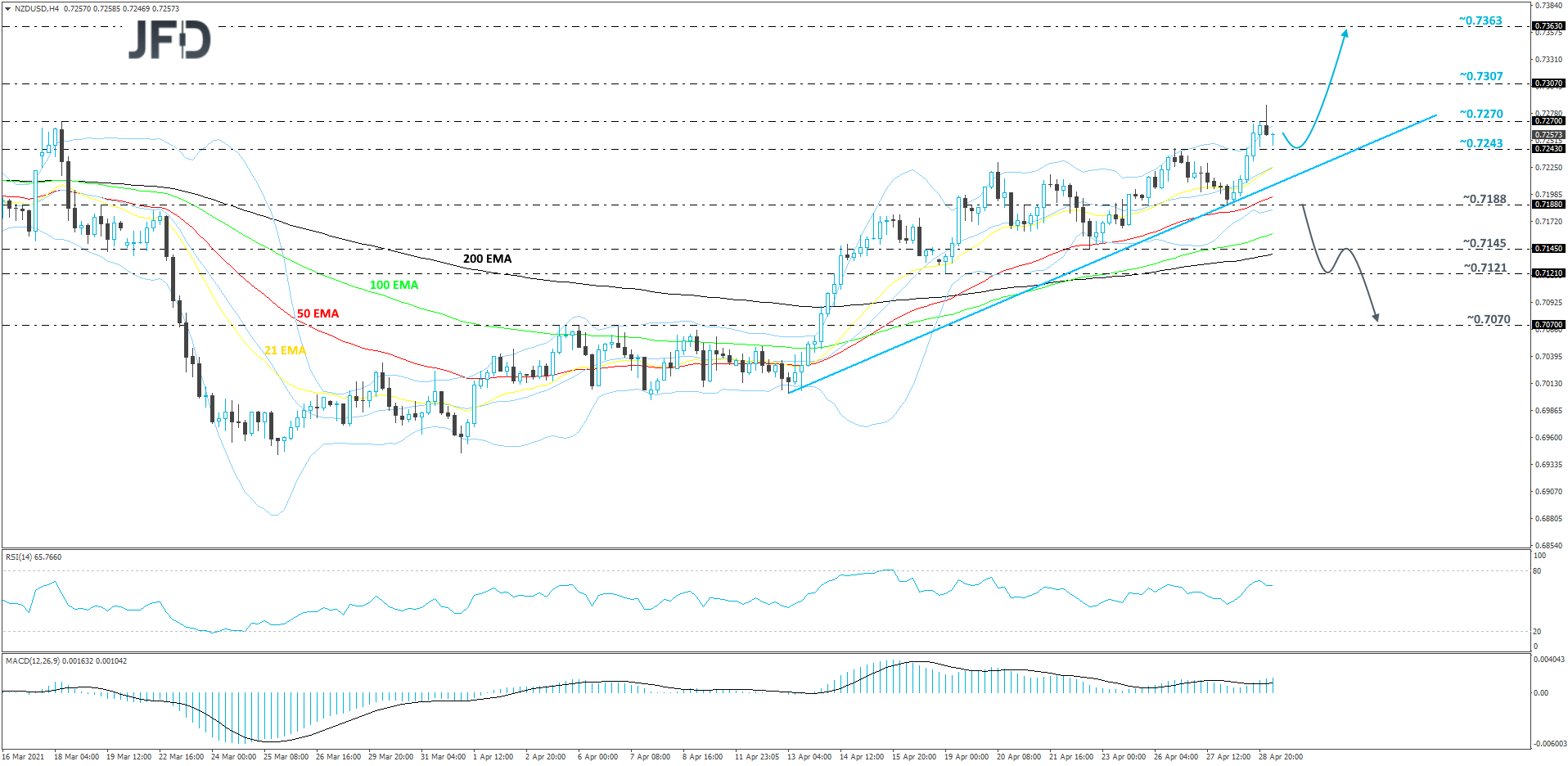

This morning, NZD/USD went for a new weekly high, this way showing that the bulls continue to dictate the rules. Also, the pair is balancing above a short-term tentative upside support line taken from the low of Apr. 13. As long as that line stays intact, we will continue aiming higher.

This morning we are seeing a slight correction lower, however if the rate remains somewhere above the 0.7243 hurdle, marked by the high of Apr. 26, that may keep the bulls interested for a while longer. If so, the pair might get pushed higher again, beyond the 0.7270 obstacle, potentially targeting the 0.7307 zone, marked by the highest point of March. If the buying doesn’t stop there, the next aim for NZD/USD could be the 0.7363 level, which is an intraday swing low of Feb. 24 and an intraday swing high of Feb. 26.

Alternatively, if the pair breaks the aforementioned upside line and falls below the 0.7188 area, marked by the low of Apr. 28, that could spook the bulls from the field temporarily. More bears may run in and drive NZD/USD to the 0.7145 obstacle, or the 0.7121 hurdle, marked by the low of Apr. 19. If the selling continues, the next possible target could be the 0.7070 level, which is marked near the highs of Apr. 5, 6 and 7.

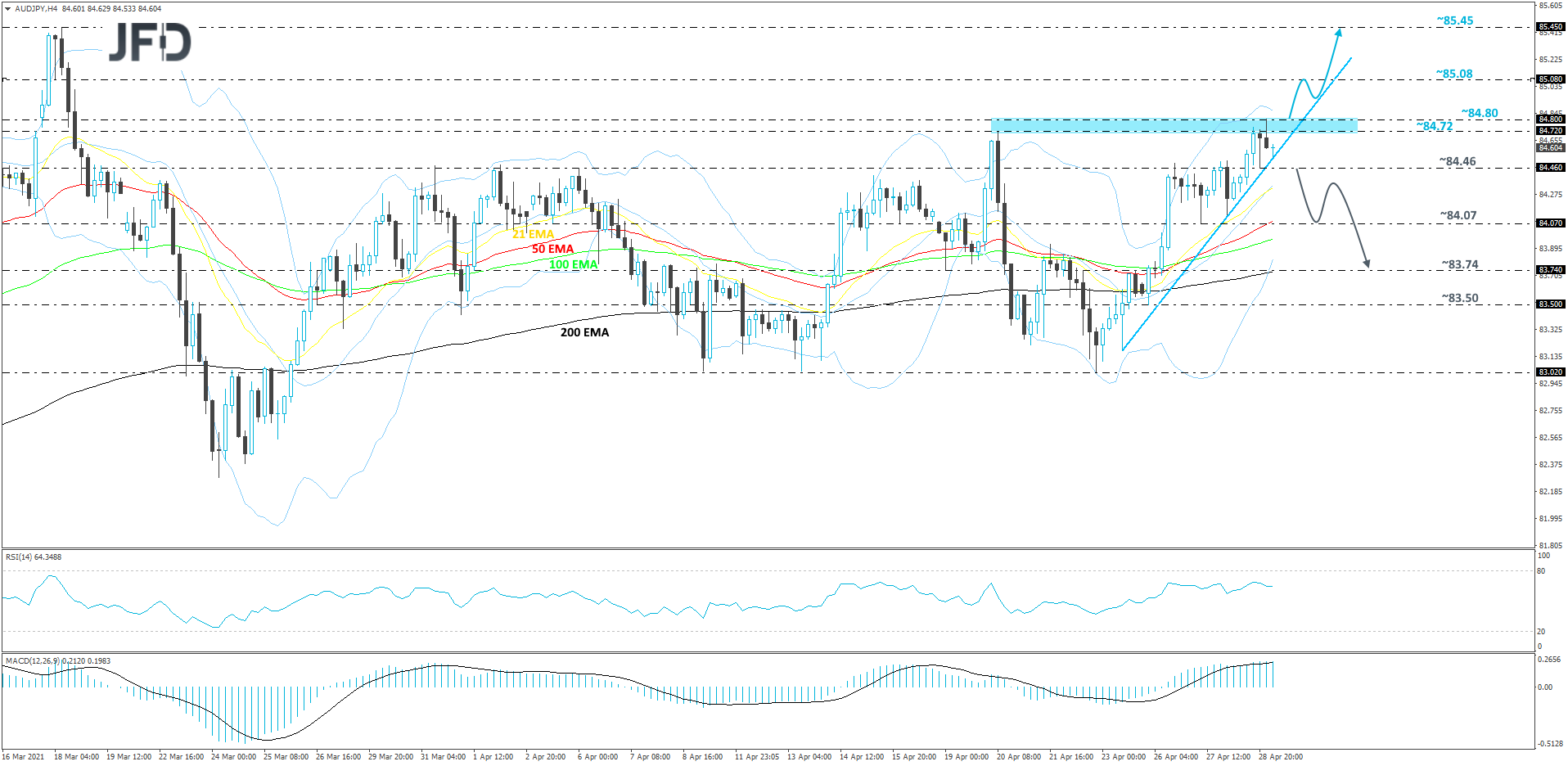

AUD/JPY Technical Outlook

AUD/JPY continues to move higher on a steep incline, after reversing higher on Apr. 23. At the same time, the pair continues to balance above a short-term upside support line taken from the low of the reversal day. So far, the near-term outlook looks positive. More buyers could join in if the rate rises above the 84.80 barrier, marked by the current high of today. We will remain positive, for now.

If, eventually, the pair climbs above that 84.80 zone, this will confirm a forthcoming higher high, potentially inviting more buyers into the game. AUD/JPY might then travel to the 85.08 obstacle, a break of which may set the stage for a push to the 85.45 level. That level is marked by the highest point of March.

On the other hand, if the aforementioned upside line breaks and the rate falls below the 84.46 zone, marked by an intraday swing low of yesterday, that could change the direction of the current short-term trend. AUD/JPY could now fall to the 84.07 obstacle, which if fails to provide support and breaks, might clear the path towards the 83.74 level, marked by an inside swing high of Apr. 23.

As For The Rest Of Today's Events

During the European session, Germany’s preliminary inflation data for April is due to be released. The CPI rate is expected to have ticked up to +1.8% yoy from +1.7%, while the HICP one is anticipated to have held steady at +2.0% yoy. This is likely to raise speculation that Eurozone’s headline CPI, due out on Friday, may also rise somewhat.

Later in the day, from the US, apart from the GDP, we also get the initial jobless claims for last week, where expectations are for a small increase, to 549k from 547k, and pending home sales for March, which are forecast to have rebounded 5.0% mom after tumbling 10.6% in February.

During the Asian session Friday, we get the usual end-of-month data dump from Japan. The unemployment rate and the jobs-to-applications ratio for March are both expected to have held steady at 2.9% and 1.09 respectively, while the preliminary industrial production for the month is anticipated to have tumbled another 2.0% mom after sliding 1.3% in February. The core Tokyo CPI rate is anticipated to have ticked down to -0.2% yoy in April from -0.1%, but no forecast is available for the headline rate.

We also have two speakers on the agenda and those are Fed Board Governor Randal Quarles and New York Fed President John 0Williams.