- Fed officials warm up to 25-bps rate hikes, cheering equity markets

- But dollar takes a hit, stands firm only against sinking yen

- Euro powers on as ECB hawk puts foot down, flash PMIs eyed

Fed enters blackout with a nod to slower hikes

Trading got off to a quieter start on Monday, as China and other major markets in Asia are closed for the Lunar New Year celebrations, and Friday’s risk rally lost some steam, but the positive sentiment continued to prevail across asset classes following some encouraging Fed commentary.

After last week’s dreadful retail sales figures, recession fears for the US economy are probably as elevated as they’ve ever been during this cycle, but hopes of a policy reversal received a major boost from Fed speakers right before the blackout period began on Saturday. Most notably, Governor Christopher Waller – one of the more influential FOMC members – backed a further downshift in the Fed’s tightening pace to 25 basis points at the January 31-February 1 meeting.

Philadelphia Fed’s Harker also voiced support for a smaller rate rise, but Esther George of the Kansas City Fed was a bit more cautious, focusing on the risks to services inflation. Although the message that there is more tightening to come remains loud and clear and this might explain why Treasury yields actually climbed on Friday, investors are noticing subtle shifts in the language.

Waller suggested that he would be open to changing the policy course if markets are proven right on inflation, while Fed Vice Chair Brainard was more acknowledging that inflationary pressures are subsiding.

A 25-bps rate hike is now almost fully priced in for the next meeting, but more importantly, the market-implied terminal rate seems to be settling slightly below 5%. As long as investors continue to price in a terminal level that doesn’t exceed 5%, this should be supportive of risk assets.

Netflix (NASDAQ:NFLX) and Google lift Nasdaq

Stocks on Wall Street surged on Friday as the combination of a potentially more ‘flexible’ Fed and some upbeat corporate news spurred another risk rally. The S&P 500 shot up 1.9%, though it did not manage to completely recoup the week’s losses. The Nasdaq Composite (+2.7%) did, however, closing back above the 11,000 level as it outperformed the other indices.

Netflix led the gainers among the tech favourites, soaring by 8.5% after its subscriber numbers beat the estimates. Alphabet (NASDAQ:GOOGL) was the second biggest winner as the Google parent became the latest to announce massive layoffs. The Nasdaq is rallying even though the tech giants have yet to report and Netflix’ EPS was way off the mark. Microsoft (NASDAQ:MSFT) will announce its earnings tomorrow followed by Tesla (NASDAQ:TSLA) on Wednesday.

Investors are clearly starting to see some light at the end of the tunnel, but this could just be another relief rally as an earnings recession remains a real possibility this year and a Fed pause could be months away. But for now, there is some optimism in the air and European shares are edging up today.

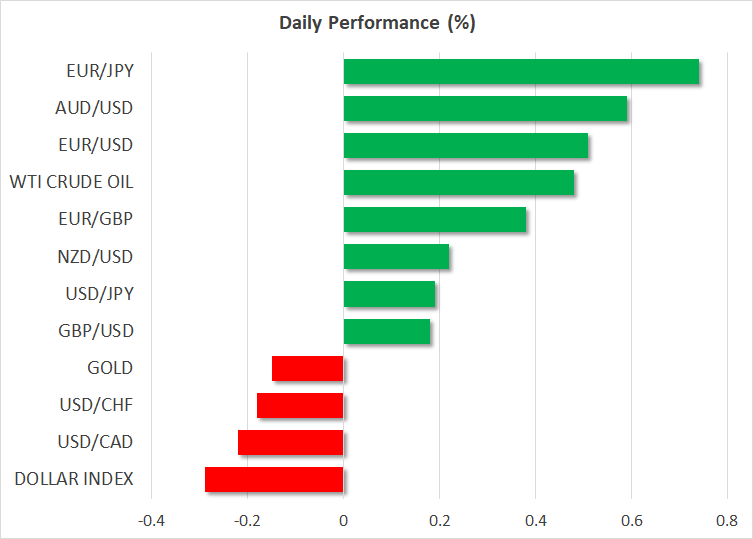

Dollar and yen slip, euro breaks key level

The positive mood added to the woes of the safe-haven US dollar and Japanese yen, both of which are already on the backfoot due to policy expectations. The yen’s ascent appears to have stalled after the Bank of Japan doubled down on its yield curve control policy last week, providing some support to the dollar index. The greenback’s gauge against a basket of currencies is close to hitting a fresh seven-month low as it’s come under renewed selling pressure, except versus the yen.

The euro has just broken above the $1.090 level for the first time since April 2022, with hawkish remarks from Dutch ECB Governing Council member Klaas Knot further bolstering the currency. The ECB has a few more 50-bps rate hikes lined up, while the Fed is probably entering the final phase of its tightening cycle. Add to that the growing signs that the Eurozone might avoid a recession, things are looking up for the euro in 2023. But the bulls will be put to the test tomorrow when flash PMI numbers for January are out.

The pound on the other hand is finding the $1.24 region a tough resistance to break as UK consumers have tightened their purse strings amid a comparatively worse cost-of-living crisis in Britain than in other advanced major economies.

The Australian dollar was the best performer on Monday, reclaiming the $0.70 handle, but the kiwi was lagging slightly as traders were somewhat cautious after Chris Hipkins was appointed as New Zealand’s next prime minister on Sunday following Jacinda Ardern’s sudden resignation. The Canadian dollar, meanwhile, was also treading water ahead of the Bank of Canada’s policy decision on Wednesday where a pause might be on the cards.