Will the Fed’s meeting drive the EUR/USD as sharply as the mid-term elections did?

Excessive sensitivity of the market to the US mid-term elections turned out to be a blank shot in fact. The factor, historically, was never a serious driver to change the US dollar rate. Besides, the results of the Democrats’ victory in the House of Representatives are not as clear as they used to seem. They have been supporting Donald Trump’s measures, related to trade wars, which has been pressing down the greenback during most of the year due to high demand for safe-heaven assets. In addition, Goldman Sachs (NYSE:GS) reminds that, since the 1970s, the US stock indexes were growing by 12% on average, since the mid-term elections until the first quarter of the next year. And it the leading performance of S&P 500 over the rivals provided capital inflow to the U.S. and laid a strong base for the USD rally.

I personally think the situation is similar to that of 2017, when after Donald Trump had become the president, the market’s view on the greenback outlook divided. Some people were confident that the mass fiscal stimulus will speed up the US inflation growth and make the Fed hike the interest rate aggressively’ others insisted that the US twin deficit will crash the greenback dramatically. The USD rate dropped down finally, but the reasons were different. It was due to the US administration’s failure to pass the legislative initiatives through the Congress and due to the greenback’s rivals, being quite strong. Currently, Morgan Stanley (NYSE:MS), Credit Agricole (PA:CAGR) and BofA Merrill Lynch suggest that the dollar is going to be getting weaker because of the US administration’s inability to implement the plan of the further tax reduction. Citigroup (NYSE:C), on the contrary, sees the USD drop as an opportunity to buy it, referring to the historically weak influence of the US mid-term influence on the greenback value.

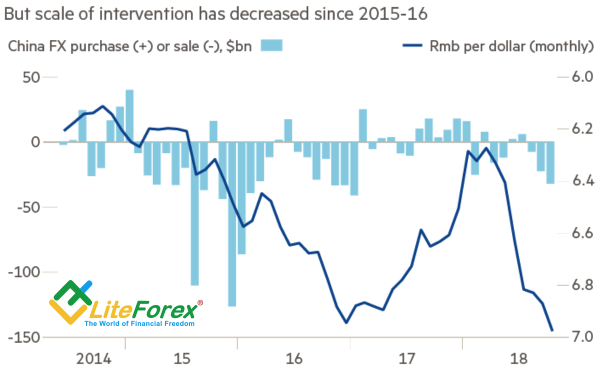

According to JP Morgan, as the US president can’t expect any support from either the Fed or the Congress, he should strike a deal with China quickly to provide the economic expansion at the current pace in future. This argument is a bullish factor for the EUR/USD. China is willing to negotiate and, based on the decline in FX reserves in October, is doing whatever is necessary to keep the yuan afloat. According to Financial Times, the scale of its intervention into foreign exchange market is about $32. Quite a substantial amount, though it is not as big as the average volume of $70 billion per month during six months, like it was in late 2015.

Dynamics of FX interventions and the yuan rate

Source: FinancialTimes.

Having surged up to the previously marked short-term consolidation range of 1.13 – 1.15, the EUR/USD pair is back at the initial levels, focusing on really important things. On the FOMC meeting. I don’t think that, following strong employment data in October, the Fed will much change its rhetoric, compared to the previous meeting. At that time, the announced willingness to conduct moderately tight monetary policy for some time pushed the dollar up. At present, investors face a really hard question, if they are to sell the dollar or not. Based on the close end of the US economic cycle, Jerome Powell will have to solve a dilemma in 2019: set back the economic expansion or continue hiking the rate? But it is still too early to discuss this, isn’t it?

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

EUR/USD Update

3rd party Ad. Not an offer or recommendation by Investing.com. See disclosure here or

remove ads

.

Latest comments

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.