Talks about the deescalation of US-China trade conflict sent the EUR/USD up to the bottom of figure 13.

It is interesting to watch the market that exactly knows what to do but doesn’t know when it is to take measures. The future slowdown of the US economy and the ECB monetary normalization suggest a positive outlook for the EUR/USD bulls on the long-term investment horizon. In addition, the deescalation of the US-China trade conflict and positive news about Brexit suggest that the European central bank should take active measures. After all, it is the protectionism and political risks that sets back the eurozone economy; and until it recovers the growth pace it is too early to expect increasing the interest rate.

The information about the negotiations between the US Treasury Secretary Steve Mnuchin and the Vice Premier of China Liu He triggered the US dollar sales. It is said in the market that the parties should agree on the finishing of the trade battle, followed by the discussing of details. According to BofA Merrill Lynch, if the trade conflict is settled down, the greenback will lose its safe-heaven status, being outperformed by the Japanese yen and the Swiss franc. These currencies were rather responsive to the political risks in the USA and the euro area, while the American dollar was steadily rising on the trade battles between the U.S. and China.

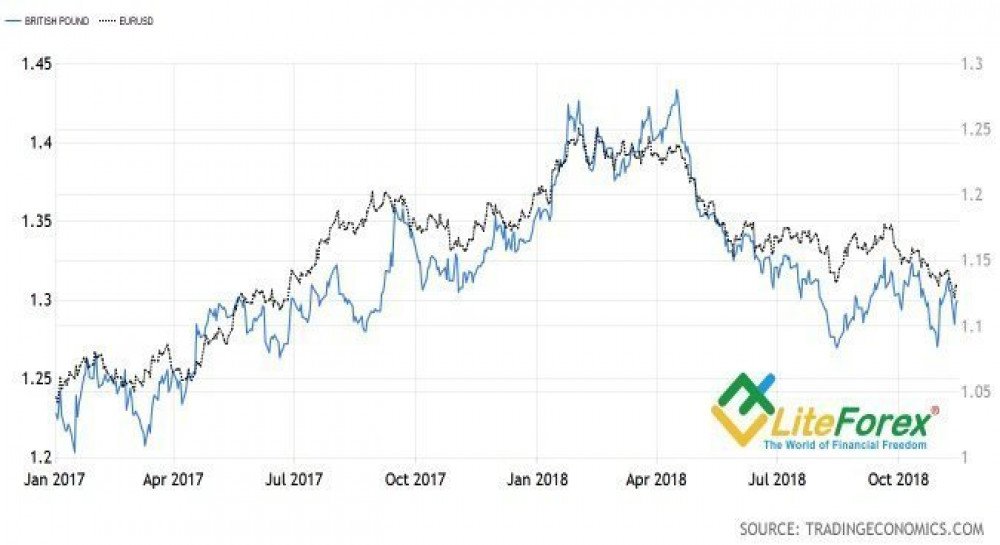

The EUR/USD bulls have been also supported by Theresa May, who announced that the government had a few unsettled issues; and by the information and that London and Brussels agreed on the Irish border. The pound has instantly surged, followed by the euro. Credit Agricole notes that the quotes of these two currencies already include too much negative and suggests its clients be extremely careful about selling the major currency pair.

Dynamics of GBP and EUR

Source: Trading Economics

The positive, suggested by the trade wars and Brexit has turned out to be stronger than the negative, raised by Italy. The Italy’s Minister of Economy and Finance Giovanni Tria announced that Rome should stick to the previously presented budget with 2.4-percent deficit. According to him, Italy hasn’t yet reached the pre-crisis level of GDP growth, and the fiscal stimulus will support it. According to the IMF, Italian economy will grow by 1% in 2018, which will result in expanded budget deficit up to 2.66%. The European Commission suggests the deficit of 2.9%. I don’t think that Brussels will agree without any arguments. The EU tools include passive watching the growth of Italian bond yields, which increases Italy’s debt-servicing costs; a fine of 0.2% of GDP; and, finally, suspension in the liquidity supply to the local banks. In cases with Greece and Cyprus it worked out, but it is now about much bigger scale.

Trade battles and political risks distracted investors’ attention from the Fed. However, they shouldn’t ignore it. AS Jerome Powell has recently stated, higher inflation rate will encourage the central bank to normalize its monetary policy at a faster pace, and vice versa. With this respect, the publication of the reports on the US consumer prices and the core inflation can become another driver for the EUR/USD. If CPI increases, the bears will be able to gain back the control and drive the pair back down to figure 12 base.