- ECB and BoE stick to hawkish stance as Fed becomes dovish outlier

- Euro and pound skyrocket before paring gains on weak PMIs

- Upbeat US data fail to deter dollar bears as yields continue to slide, stocks party

No rate cut talk at the ECB and BoE

Central banks in Britain and the euro area diverged from their US counterpart on Thursday, sidestepping any talk about rate cuts while reiterating the need to maintain higher rates for longer. The European Central Bank kept its main lending rates unchanged as expected, but President Christine Lagarde took markets by surprise with the hawkishness of her tone.

Although the ECB lowered its forecasts for inflation for this year and next, Lagarde displayed heightened wariness about elevated wage pressures, warning that policymakers shouldn’t lower their guard. She also disappointed those anticipating some signal of a rate cut, telling reporters “We did not discuss rate cuts at all” in her press briefing.

In a further hawkish twist, the ECB accelerated its quantitative tightening schedule by announcing an early end to its PEPP reinvestments.

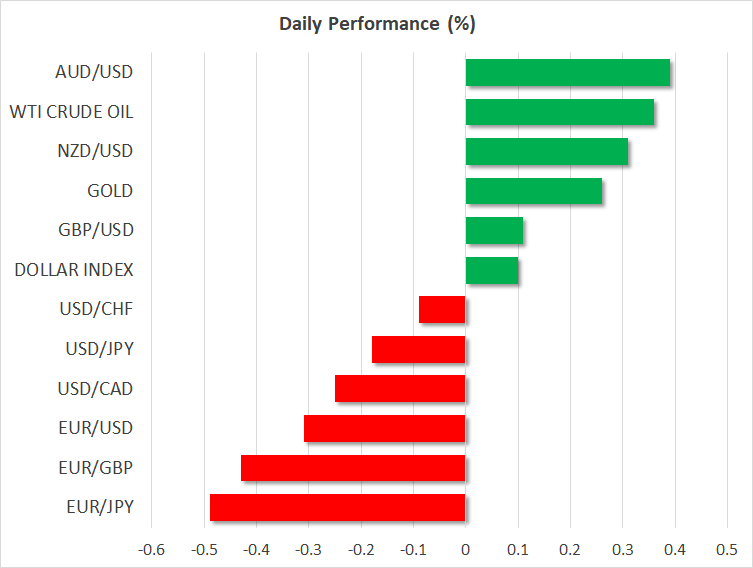

The Bank of England also delivered a hawkish pause, pointing to several upside risks to inflation. Higher services inflation and strong wage growth in particular are a bigger problem in the UK than elsewhere, so the BoE’s stance is probably the least surprising. Nevertheless, it’s far too evident how much more work the BoE still has in reining in inflation completely and that explains why the pound was the best performer yesterday, followed closely by the euro and the yen.

Dollar selloff aids euro, pound and yen

The pound came just shy of reclaiming the $1.28 level, while the euro briefly brushed the $1.10 mark. The yen has also been on a roll lately amid the US dollar’s broad selloff and speculation that the Bank of Japan is inching closer to exiting negative interest rates. The dollar hit a four-and-a-half-month low of 140.94 yen on Wednesday.

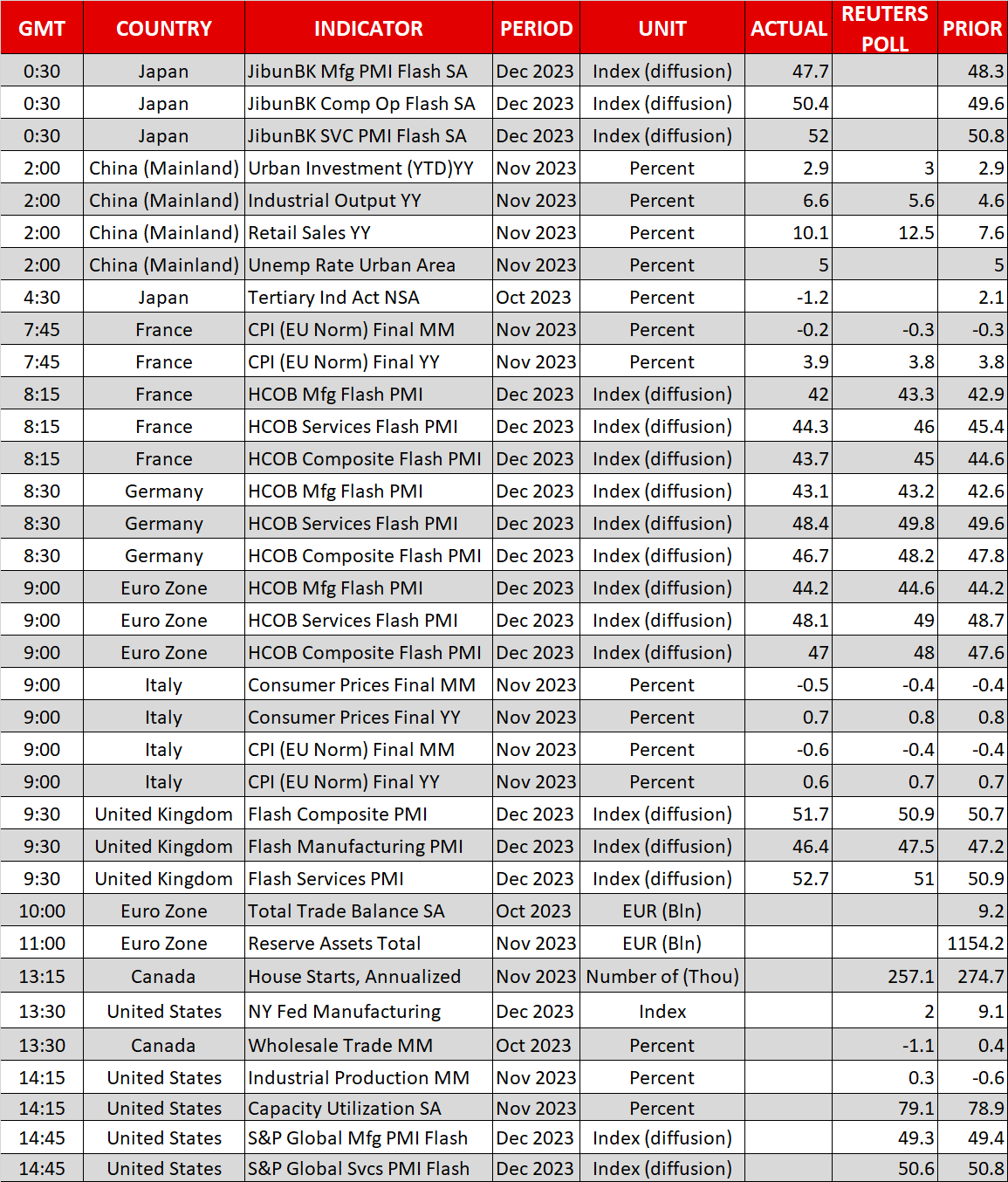

However, there’s a bit of a pullback today for the euro following a very poor batch of flash PMI readings out of the Eurozone. The French and German PMIs have fallen deeper into contraction territory, dragging the Eurozone composite PMI down to 47.0 in December from 47.6 previously. Expectations were for a slight improvement to 48.0.

The UK economy on the other hand seems to be faring notably better. Although the manufacturing PMI disappointed, the services sector appears to be bouncing back, pushing the composite PMI to a 6-month high of 51.7.

Monetary policy divergence in the spotlight after latest data

The latest data highlights how central banks have become at odds about the way forward on rates and is perhaps one of the reasons why investors are not listening to policymakers. Only yesterday, US retail sales beat expectations in November and weekly jobless claims declined. Yet, the Fed seems to be sending a clear signal that rate cuts are on the way, while the ECB wants to keep rates on hold for an extended duration despite the Eurozone economy being the weakest among the G10.

Investors have not altered their view that the ECB will begin slashing rates in April, with the cumulative cuts for 2024 being ratcheted up after the PMI releases. As for the Fed, there is greater certainty that the first cut will come in March rather than May.

Investors have also upped their bets for Bank of England rate cuts, but in the short term at least, the pound’s bullish streak is likely to continue. The yen is another currency that could extend its gains in the coming days should the Bank of Japan offer clues about the possible timing of liftoff when it meets on Tuesday.

Stocks remain buoyant

For equity traders, though, the sharp slide in yields has turbo-charged the end-of-year rally, with even Hong Kong’s Hang Seng index joining in today. China’s central bank injected a record amount of liquidity into the economy after another batch of underwhelming economic data were released on Friday. The cash injection, along with the relaxation of property restrictions in Beijing and Shanghai boosted sentiment in Asia.

On Wall Street, the Dow Jones closed at another record high on Thursday, while the S&P 500 and Nasdaq set new 2023 highs as tech behemoth, Apple (NASDAQ:AAPL), saw its share price hit an all-time high.