Although Wall Street indices gained nearly 5% yesterday, after the U.S. closing, stock futures and then Asian bourses slid as U.S. President Trump did not hold the conference he promised on Monday. Flying from the U.S. to the UK, the BoE unexpectedly cut its benchmark interest rate by 50bps today, while later in the day GBP traders are likely to turn their attention to the UK budget announcement.

Equity Markets Turn South Again as Trump Delays Stimulus Package

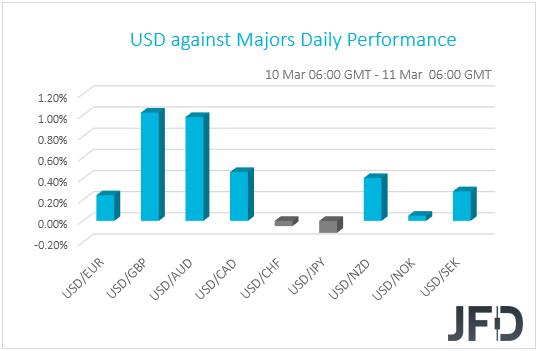

The US Dollar Index traded higher against most of the other G10 currencies on Tuesday and during the Asian morning Wednesday. It gained against GBP, AUD, CAD, NZD, SEK and EUR in that order while it lost some ground against JPY. The greenback was found virtually unchanged versus CHF and NOK.

The relative strength of the yen and the franc, combined with the weakening of the commodity-linked currencies Aussie, Kiwi and Loonie, suggests that risk appetite was subdued yesterday. However, the strengthening of the dollar points otherwise. Although it’s been used as a safe haven in the past, it had been weakening recently during risk-off periods due to elevated expectations that the Fed will continue easing aggressively.

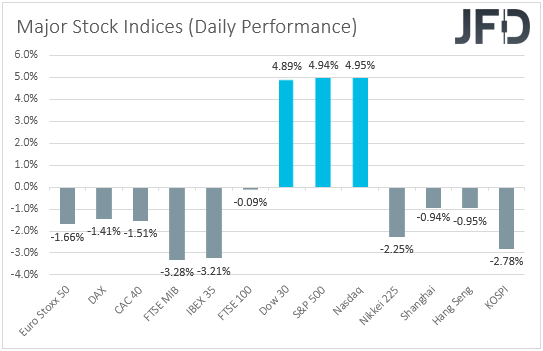

Turning our gaze to the equity world we see that indeed market sentiment had its ups and downs. EU equities closed in negative territory due to the acceleration in infected cases across the bloc. Italy is under lockdown, while the UK and Germany continue to report more and more infections. We also had a surprise surge in Sweden. With all this in mind, European investors may have little tolerance in holding risky assets for long.

That said, during the US session, the picture was totally different. All three of Wall Street’s major indices gained nearly 5%, with participants on the edge of their seats in anticipation of Trump’s conference on measures to fight the virus outbreak. Early on Tuesday, Trump held a briefing with Senate Republicans to discuss potential options, like a payroll tax relief until after the November election. This may have been the fuel behind the dollar’s strength as well. However, the conference never happened, and this came as a big disappointment. After the US closing, stock futures reversed some of their prior gains, while today, Asian bourses traded in the red. Both Japan’s Nikkei 225 and China’s Shanghai Composite slid 2.25% and 0.64% respectively.

As for our view, it still remains the same as yesterday and the day before, … and the day before. We believe that rate cuts and tax cuts are not enough to offset the damage. We need signs that the virus has entered a slowdown mode and stayed there for a decent period of time. As long as it is spreading at such a fast pace, the economic wounds could deepen and drag well into Q2. We repeat once again that with elevated uncertainty on how much more serious all this could get, it would be naïve to assume that everything is priced in. Therefore, we would treat any gains in equities as corrective moves, before the next leg south. We believe that there is still room for declines in risk assets as investors my seek once again shelter in safe havens.

S&P 500 – Technical Outlook

Despite recovering yesterday some of its losses made at the start of the week, the S&P 500 remains below its short-term tentative downside resistance line taken from the high of February 20th. Even if the price could claw back a bit more of those losses, still, if the above-discussed downside line stays intact, we will continue targeting the downside, hence why we will take a bearish approach.

Given the steep drops we saw recently, the index might try to retrace a bit more to the upside, however, as mentioned above, if the bulls struggle to push the S&P 500 above that downside line, this might cause another round of selling. The price could then fall all the way to the 2698 hurdle, which is the current low of this week on the cash index, or to the 2682 territory, marked by the lowest point of February. The S&P 500 may stall there for a bit, but if the bear pressure is still strong, a break of that area would confirm a forthcoming lower low. That’s when we will target the 2623 level, marked by the low of January 28th.

On the upside, if the previously-discussed downside line breaks and the price accelerates above the 2988 barrier, which is an intraday swing high of March 6th, this may attract even more buyers into the game. The index might then travel to the high of March 6th, at 3038, a break of which could clear the way to the 31389 level, marked by the current high of this month. Around there, the S&P 500 could also meet the 200 EMA on the 4-hour chart, which may also show a bit of resistance.

BoE Delivers a “Double Cut”, UK Budget Enters the Limelight

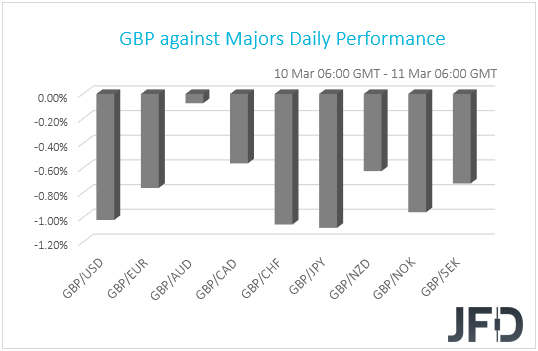

The pound was found to be the main loser among the G10 currencies. With no catalyst behind the slide, GBP-traders may have been biting their nails in anticipation of the UK Budget today and with the US government underdelivering, they may have been concerned that the UK one could also disappoint. As we are writing the report, the currency is extending it tumble as the BoE surprised the markets by delivering a rate cut of 50bps, outside a scheduled gathering, as the Fed did last week.

With regards to the Budget, this is the Autumn budget that was scheduled for November 2019, but was delayed due to the fact that general elections were called. Under normal circumstances, this time of the year, we have the Spring Statement, which is an update on the numbers. This would be the first Budget of the new Chancellor Rishi Sunak, who replaced Sajid Javid back on February 13th. Javid’s stance over spending was seen as more cautious than Sunak’s, and thus, it would be interesting to see how expansionary the new budget will be. In the midst of the domestic economic slowdown and fears over the coronavirus impact, decent fiscal support may lessen the need for additional cuts by the BoE and thereby help the pound recover some of its latest lost ground.

That said, we prefer to exploit any potential pound recovery against risk-linked currencies, like the Aussie and the Kiwi. As we already noted, we hold the view that the worst is not behind us yet with regards to the coronavirus and thus, we expect those currencies to stay under selling interest. We would avoid the traditional safe havens yen and franc, as they may continue attracting flows while uncertainty and concerns remain elevated.

The UK GDP for January, as well as industrial and manufacturing production data for the month are coming out, but they may get overshadowed by the budget announcement. Just for the record, economic growth is expected to have slowed to +0.2% mom from +0.3%, while the yoy rates of IP and MP are forecast to have slid further into the negative territory. Specifically, they are anticipated to have declined to -2.5% yoy and -3.3% yoy respectively, from -1.8% and and -2.5%. The nation’s trade balance is also coming out and expectations are for December’s surplus to have turned into deficit in January.

GBP/NZD – Technical Outlook

After a sharp spike on Monday, GBP/NZD retraced back down, closer to its short-term upside support line taken from the low of January 20th. Although there is a possibility to see another small drop lower, as long as the rate stays above that upside line, we will take a somewhat bullish approach.

Given that pair slid below yesterday’s low, at 2.0490, but remained above the aforementioned upside support line, this may still give hope for the bulls to take charge again and push the rate up. That’s when we will aim for yesterday’s high, at 2.0764. Initially, GBP/NZD might get held around there, but if that barrier eventually fails to withstand the bull pressure and breaks, such a move could open the door to some higher resistance areas. One of those areas might be the 2.0165 level, marked by an intraday swing high of March 9th.

Alternatively, if the pair breaks the above-discussed upside support line and the rate falls below the 2.0353 hurdle, which is the current low of this week, this may lead to a change in the direction of the short-term trend. GBP/NZD could then fall under the control of more sellers, who could force it to slide to the 2.0257 obstacle, or even the 2.0180 area, marked by the low of February 17th. If the selling doesn’t stop there, a further decline could put the psychological 2.0000 level back on the radar. Last time that level was tested on February 6th and 12th.

As for the Rest of Today’s Events

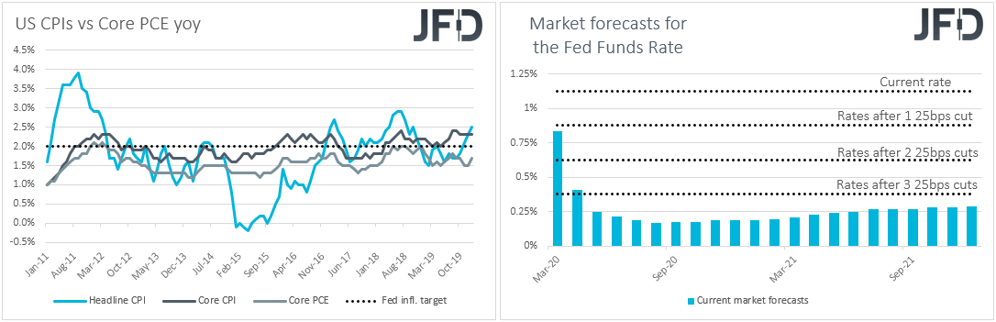

From the US, we get the CPIs for February. The headline rate is expected to have declined to +2.2% yoy from 2.5%, while the core rate is anticipated to have remained unchanged at +2.3%. Under normal circumstances, CPI rates above the Fed’s 2% inflation aim would have allowed officials to remain sidelined, despite their favorite metric being the core PCE rate which runs below 2%. Having said that though, after last week’s double cut, Fed Chair Powell highlighted that the fundamentals of the US economy remain strong, adding that they decided to cut due to the risks the coronavirus poses to activity. Thus, we don’t expect US domestic data to alter expectations around the Fed’s future course of action. According to the Fed funds futures, investors are pricing in another cut, a triple one this time, to be delivered at next week’s gathering, while there is a 60% chance for interest rates to touch zero at the April gathering.

With regards to the energy market, we get the EIA (Energy Information Administration) report on crude oil inventories and expectations are for a 2.266mn bpd increase after a 0.785mn inventory build the week before. However, bearing in mind that the API report revealed a 6.407mn rise, we would consider the risks of the EIA forecast as tilted to the upside.

- English (UK)

- English (India)

- English (Canada)

- English (Australia)

- English (South Africa)

- English (Philippines)

- English (Nigeria)

- Deutsch

- Español (España)

- Español (México)

- Français

- Italiano

- Nederlands

- Português (Portugal)

- Polski

- Português (Brasil)

- Русский

- Türkçe

- العربية

- Ελληνικά

- Svenska

- Suomi

- עברית

- 日本語

- 한국어

- 简体中文

- 繁體中文

- Bahasa Indonesia

- Bahasa Melayu

- ไทย

- Tiếng Việt

- हिंदी

Equities Fall As Trump Disappoints, BoE Cuts By 50bps Ahead Of UK Budget

Published 03/11/2020, 05:02 AM

Updated 07/09/2023, 06:31 AM

Equities Fall As Trump Disappoints, BoE Cuts By 50bps Ahead Of UK Budget

Latest comments

Loading next article…

Install Our App

Risk Disclosure: Trading in financial instruments and/or cryptocurrencies involves high risks including the risk of losing some, or all, of your investment amount, and may not be suitable for all investors. Prices of cryptocurrencies are extremely volatile and may be affected by external factors such as financial, regulatory or political events. Trading on margin increases the financial risks.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

Before deciding to trade in financial instrument or cryptocurrencies you should be fully informed of the risks and costs associated with trading the financial markets, carefully consider your investment objectives, level of experience, and risk appetite, and seek professional advice where needed.

Fusion Media would like to remind you that the data contained in this website is not necessarily real-time nor accurate. The data and prices on the website are not necessarily provided by any market or exchange, but may be provided by market makers, and so prices may not be accurate and may differ from the actual price at any given market, meaning prices are indicative and not appropriate for trading purposes. Fusion Media and any provider of the data contained in this website will not accept liability for any loss or damage as a result of your trading, or your reliance on the information contained within this website.

It is prohibited to use, store, reproduce, display, modify, transmit or distribute the data contained in this website without the explicit prior written permission of Fusion Media and/or the data provider. All intellectual property rights are reserved by the providers and/or the exchange providing the data contained in this website.

Fusion Media may be compensated by the advertisers that appear on the website, based on your interaction with the advertisements or advertisers.

© 2007-2024 - Fusion Media Limited. All Rights Reserved.