- Dollar slides as durable goods orders slip more than expected

- Pound outperforms on new Northern Ireland deal

- Equities gain, but outlook stays dim

Dollar slips, but hike bets stay elevated

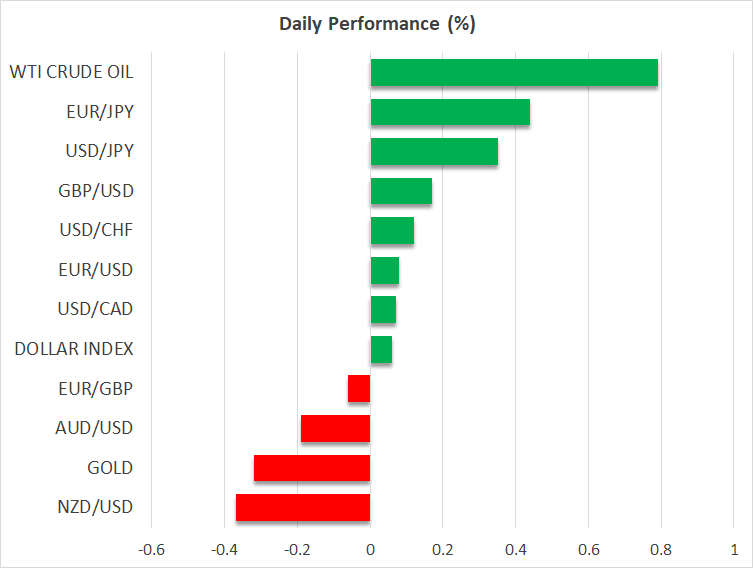

The dollar traded lower against all the other major currencies on Monday, although it rebounded somewhat today.

What prompted traders to liquidate their long dollar positions may have been the larger than expected slide in durable goods orders for January. The headline m/m rate tumbled to -4.5% from 5.1%, with the excluding defense rate falling to -5.1%. Nonetheless, durable goods orders excluding both defense and aircrafts rebounded 0.8% from -0.3%, which means that the slide in the headline print was mainly due to plunging aircraft orders.

That’s maybe why investors barely touched their bets with regards to the Fed’s future course of action. Following a streak of positive data and hotter-than-expected inflation for January, they are currently expecting US interest rates to peak at around 5.4% in July, while they expect them to end the year at 5.3%, higher than the Fed’s own median projection of 5.1% for the year.

With all that in mind, it is hard to envision larger declines in the dollar for now. However, it is also premature to call for a long-lasting recovery, as ahead of the March FOMC gathering, market participants will have to digest several more data releases, and most importantly, the employment and CPI numbers for February. What’s more, the Fed is not the only major central bank expected to proceed more aggressively henceforth. Investors have been also adding to their ECB hike bets, assigning a nearly 40% probability for a 75bps hike in March, and a total of 150bps worth of rate increments until the end of the year.

This week, dollar traders will have the opportunity to get a first glimpse as to how the US economy performed during the second month of 2023 as the ISM manufacturing and non-manufacturing PMIs are due to be released on Wednesday and Friday, respectively. The forecasts point to a mixed picture, with the manufacturing PMI expected to have risen to 48 from 47.4, and the non-manufacturing PMI expected to have declined to 54.5 from 55.2. Nonetheless, given that the service sector accounts for nearly 80% of US GDP, another print decently above 50 is unlikely to elicit a reduction in Fed hike bets.

Pound traders cheer Northern Ireland accord

The British pound was the main gainer after UK Prime Minister Rishi Sunak reached common ground with the EU on post Brexit trade rules for Northern Ireland, saying that the two sides struck a deal that removes “any sense of a boarder” between Britain and its province. The accord takes off the table a scary tail risk for the pound and other UK assets, that of an EU-UK trade dispute, and that’s maybe why the pound enjoyed gains against every other major currency.

The good news comes on top of last week’s upside surprise in the UK PMIs, which added to hopes that the UK may be on course to bypass a long recession. Nevertheless, it is still too early to argue for long-lasting gains in the pound. Although investors added to their BoE hike bets as well lately, they are expecting as many basis points worth of additional rate increments as they do with regards to the US, where interest rates are already at a higher level. What’s more, Cable has been stuck within a sideways range since the end of November, between 1.1900 and 1.2440, painting a neutral picture for now.

Wall Street recovers somewhat as dollar slides

The slide in the dollar helped Wall Street recover somewhat yesterday, with the Nasdaq gaining the most ground. Perhaps the slide in durable goods orders made some investors believe that the Fed will not proceed that aggressively after all. It could also be that the risk appetite triggered by the EU-UK accord during European trading rolled over into the US session as well.

Still, with the consensus pointing to US interest rates peaking at 5.4% this year, and with all the previously anticipated cuts for the year being priced out, seeing equities drifting further north and heading towards their record highs seems a rather unreasonable scenario. Anything adding to speculation about a more aggressive Fed could bring equities under renewed selling interest as higher interest rates mean higher borrowing costs and lower valuations for firms. Today, the Conference Board consumer confidence index for February is expected to have rebounded, which could revive fears of further acceleration in inflation and thereby weigh on Wall Street.

Today’s agenda also includes the Canadian GDP data for Q4. The annualized q/q rate is estimated to have declined to 1.5% from 2.9%, which could cement expectations that the BoC will refrain from pushing the hike button when it meets next.