The US dollar has been in a rally mode since Friday, while oil prices and gold tumbled and even opened with negative gaps on Monday.

The big driver behind the rally in the US dollar, and partly behind the slump in commodity prices, may have been the better-than-expected US employment report for July, which may have increased speculation for an early tapering by the Fed, perhaps as early as in September.

US Jobs Report Fuels Fed Normalization Bets

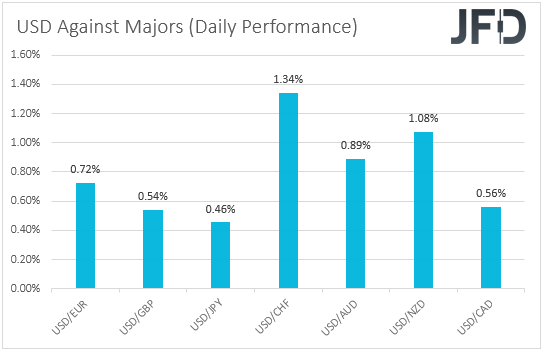

The US dollar outperformed all the other major currencies on Friday, Monday, and in the Asian session on Tuesday. It gained the most versus CHF, NZD, and AUD in that order, while it eked out the least gains against JPY.

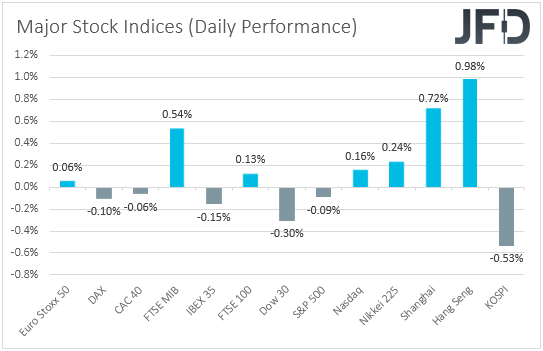

The strengthening of the dollar, combined with the weakening of the risk-linked Aussie and Kiwi and the fact that the yen lost the least ground, suggests that markets traded in a risk-off fashion. However, shifting attention to the equity world, we see a rather mixed picture, although we saw some improvement late in the Asian session today.

Appetite appeared much more subdued in the commodity market, with oil and gold prices falling on Friday, and opening with negative gaps on Monday. Although they recovered somewhat afterwards, they remain well below their Friday openings.

As mentioned above, the big catalyst behind the USD rally, and in part, the drop in commodity prices, may have been the surprise US Nonfarm Payrolls, which rose more than expected, while the unemployment rate slid below its own consensus.

Earnings exceeded their forecasts as well. With Fed Chair Powell noting at the press conference following the latest FOMC meeting that the labor market has still a long way to go, the jobs report came to undermine his remarks, and combined with hawkish comments by several other policymakers, including Vice Chair Clarida, added to speculation that the Fed may need to start tapering its QE purchases sooner than previously anticipated.

This could mean sooner rate hikes as well. Indeed, according to the Fed funds futures, the timing of when market participants expect the Fed to proceed with the first 25bps increase has come slightly forth, to March 2023 from April 2023 ahead of the report.

Oil and gold prices may have also felt the heat of concerns around the spreading of the coronavirus Delta variant, which resulted new restrictions in Asia. However, there appears to be a disconnect with the equity world, where, although investors appeared careful, they kept major indices near their records. Perhaps they want to take advantage of extra-low interest rates before it is too late.

As for our view, with what we have in hand now, we would expect this pattern to continue. Namely, the dollar to continue gaining, and commodities, alongside commodity-linked currencies, to continue underperforming. As for the equities, although we could see some retreat due to more cautiousness, we cannot rule out fresh highs in the days to come.

That said, a lot may also depend on the US CPI data for July, due out on Wednesday. Another set of extremely high numbers, well above the Fed’s objective of 2%, could add to the view that the surge in inflation may not be transitory, and thereby, increase further the chances for an earlier normalization by the Fed.

If, indeed, the CPIs solidify the case for the Fed to start withdrawing stimulus soon, perhaps in September, market participants may then start examining hints and clues on the pace of the normalization process.

Currently, the Fed is buying USD 120bn worth of assets per month. So, a USD 20bn taper means that the program will end in six months, and thereby allow even earlier rate hikes, while withdrawing only half of that amount would take a full year. We may get more information on that front at the Jackson Hole Economic Symposium, scheduled later this month.

EUR/USD - Technical Outlook

EUR/USD has been in a sliding mode since Friday, and yesterday, it managed to break below the key support zone of 1.1750, marked by the low of July 21. Overall, the pair continues to trade below the downside resistance line drawn from the high of June 1, which combined with the fact that the fall below 1.1750 confirmed a forthcoming lower low on the daily chart, keeps the near-term outlook negative.

We would now expect the bears to initially target the 1.1705 level, marked by the low of Mar. 31, the break of which could see scope for larger extensions, perhaps towards the 1.1620 territory, marked by the low of Nov. 2, slightly above the low of Nov. 4.

On the upside, we would start examining the case of a short-term reversal upon a break above the 1.1895 zone, which acted as a ceiling between July 29 and Aug. 4. We could then see the bulls targeting the 1.1950 area, the break of which could trigger extensions towards the 1.1990 hurdle. Another break, above 1.1990, could pave the way towards the low of May 13, at around 1.2050.

WTI – Technical Outlook

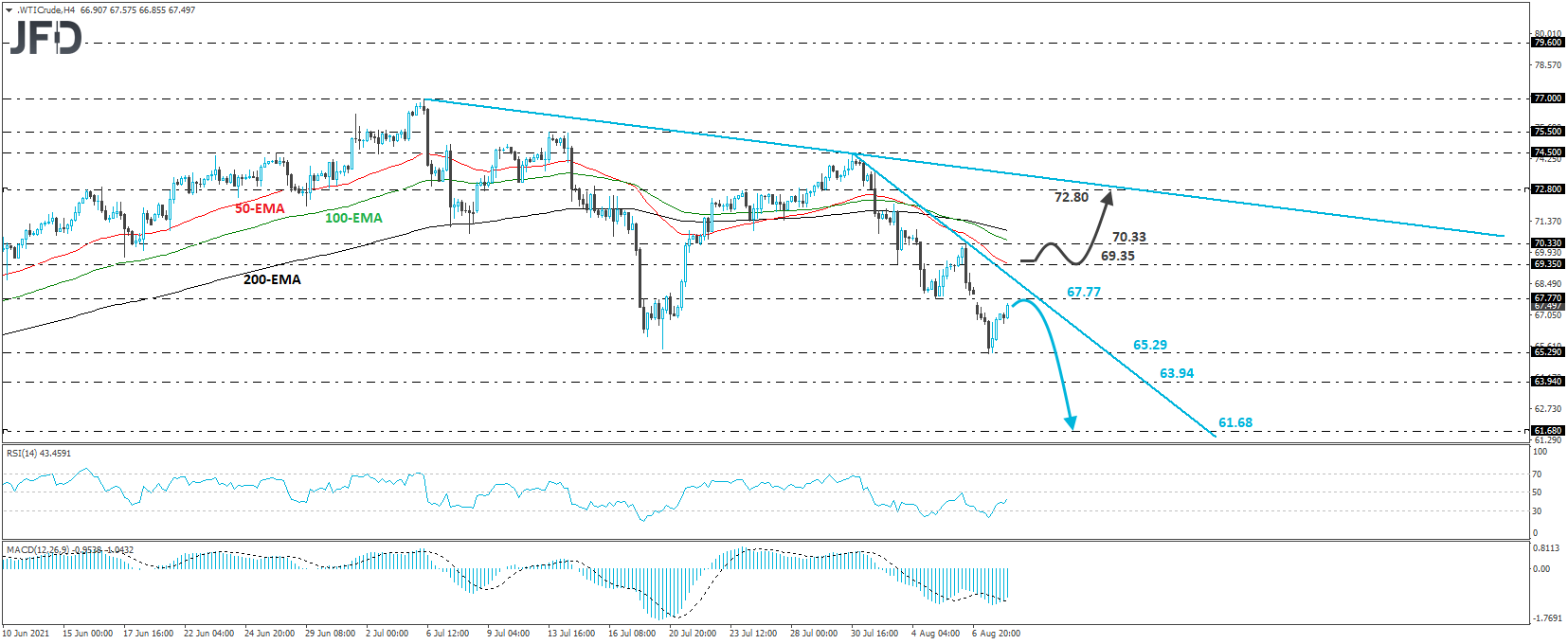

WTI fell sharply on Friday and continued to slide on Monday. However, it hit support at 65.29, and then it started to recover. At the time of writing, it was trading fractionally below the 67.77 resistance level, marked by the inside swing low of Aug. 5. Despite the recovery, taking into account that WTI is still trading below the downside resistance line drawn from the high of July 30, we will consider the short-term picture to be negative.

The bears may take charge from near the 67.77 zone, or the aforementioned downside line and push the action down for another test near 65.29. A break lower would confirm a forthcoming lower low and may allow a test near the 63.94 level, marked by the inside swing high of May 20, where another break could set the stage for declines towards the 61.68 area, defined as a support by the lows of that day and the next.

Now, in case we see a recovery back above 69.35, which is the low of Aug. 3, we will start examining the case for a larger correction to the upside. The bulls may initially target the high of Aug. 6, at 70.33, the break of which could open the path towards the crossroads of the 72.80 area, and the downside resistance line taken from the high of July 6.

As For Today's Events

The calendar appears relatively light today, with no major market movers on the agenda. During the EU session, we had the German ZEW survey for August. The current conditions index was expected to have risen to 30.0 from 21.9, while the economic sentiment one was forecast to slide to 57.0 from 63.3.

Although the current conditions index was suggesting that the economic recovery in Eurozone’s growth engine continues despite fears over the Delta variant of the coronavirus, the economic sentiment reveals cautiousness for the future. Therefore, we don’t expect the euro to receive any support if this is the case.

With the ECB signaling through its new guidance that it is now willing to keep interest rates low for much longer than the previous guidance suggested, and with expectations around of an earlier Fed action growing recently, we believe that the path of least resistance for EUR/USD remains to the downside

With regards to the energy market, we get the API (American Petroleum Institute) report on crude oil inventories for last week, but as it is always the case, no forecast is available.

As for the speakers, we have one on today’s agenda and this is Chicago Fed President Charles Evans. Following the relatively dovish remarks by Fed Chair Powell at the press conference after the latest policy gathering, several officials, including Vice Chair Clarida, sounded more hawkish. Thus, it would be interesting to see whether Evans is among those agreeing with Powell, or whether he will also join the hawkish camp, advocating for earlier tapering, and/or earlier rate hikes.