US begins review of Nvidia AI chip sales to China, Reuters reports; shares rise

Dropbox (DBX) is finally looking ripe for a buy as this cloud storage giant falls to an attractive valuation. DBX debuted its shares to the public in March of 2018 and has had a rocky ride since, with its share price tumbling 32% since. The firm just released its Q4 earnings and provided the markets with forward guidance that propelled this stock 20%. Analysts have risen EPS estimates and pushed this stock into a Zacks Rank #1 (Strong Buy).

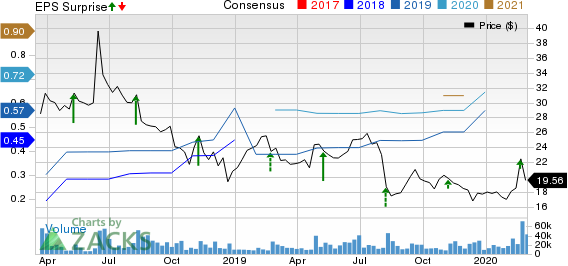

Dropbox, Inc. Price, Consensus and EPS Surprise

Dropbox, Inc. price-consensus-eps-surprise-chart | Dropbox, Inc. Quote

Dropbox beat on both top and bottom-line metrics in its earnings report, but the most notable announcement was the firm’s substantial increase in its long-term margin guidance. The company raised its 2024 operating margin guidance from 20-22% to 28-30%. This may sound like a moon shot considering its current operating margins are less than half of that. Still, the company has been very effective in telegraphing conservative guidance to the markets. Despite a falling share price, the company has been able to beat on both top and bottom-line metrics every quarterly earnings since its IPO.

Investors have traded this stock down because of concerns about the competitive nature of the cloud storage and work collaboration space. Dropbox is competing with cloud giants like Google (GOOGL) and Amazon (AMZN), but the firm has proven its market penetration and ability to grow out its userbase consistently. Dropbox has been able to accumulate over 600 million users, with 14.3 million paid subscribers, up 12.5% from last year. The business has been able to expand its average revenue per paying user to $125, representing 4.5% growth.

DBX has fallen to a valuations level that I am comfortable buying at especially considering management’s sharp upwardly guided revisions.

DBX is trading at a 4.2x forward P/S, which is at the lowest end of the firm’s range (3.7x - 11x) since its IPO 2 years ago. These shares are up over 9%, despite the 13% drop off catalyzed by the coronavirus which infected the global markets last week, causing the worst market one week break down since the financial crisis. This drop has created an excellent buying opportunity for this cloud giant.

This enterprise is right in the sweet spot for a potential buyup by a larger tech conglomerate. The stock has fallen to an attractive price and a market cap of $8 billion. This would be a reasonable price to pay for the business’s 600+ million users and its cloud infrastructure.

Take Away

Dropbox is a younger growth company that is toeing the line of profitability, the quintessential high-risk high-reward profile. I wouldn’t allocate a significant amount of my portfolio for DBX, but I would make some room for this cloud stock as its future brightens.

5 Stocks Set to Double

Each was hand-picked by a Zacks expert as the #1 favorite stock to gain +100% or more in 2020. Each comes from a different sector and has unique qualities and catalysts that could fuel exceptional growth.

a

Most of the stocks in this report are flying under Wall Street radar, which provides a great opportunity to get in on the ground floor.

Today, See These 5 Potential Home Runs >>

Alphabet Inc. (NASDAQ:GOOGL): Free Stock Analysis Report

Dropbox, Inc. (DBX): Free Stock Analysis Report

Amazon.com, Inc. (NASDAQ:AMZN): Free Stock Analysis Report

Original post

Zacks Investment Research